What bubbles, eventually bursts: are 2020’s tech IPOs the path to the first post-pandemic crisis?

“It doesn’t have to be that for somebody to win someone else has to lose. […] We can work hard to design better systems for everyone, there is no question about that” — Brian Chesky, Airbnb’s CEO

2020 was a “bust-and-boom pandemic year” for financial markets, especially in the United States. In fact, December was the hottest month when it came to what big investors are really putting money into: tech IPOs. After all, with their expansionary measures, central banks and governments are trying to prop up crisis-stricken sectors. In a way, these measures are sustaining market instability, making it difficult to predict the return on investments relative to their actual risk. Thus, buyers are pouring their money into “ever-riskier bets, driving valuations of unprofitable start-ups to levels that seem divorced from reality.” Against this background, the “current IPO craze is starting to look a lot like the 1999 tech bubble.” Will it burst?

What is all this about?

An IPO (Initial Public Offering) is the most typical procedure through which a company can “go public”. This means that “the general public has the ability to buy shares” that had previously been held “privately”. An IPO usually involves some bureaucratic procedures, followed by the issuance of a stock of shares. Then, companies have to set a price at which they will be offered to institutional investors. The operation’s profitability for the company depends on how much more valuable its stocks are by the end of the day. However, investors should be careful. It is not uncommon for markets to overshoot IPO shares’ price. This holds especially true in the case of tech firms.

Figure 1 An IPO (Initial Public Offering) is the most typical procedure through which a company can “go public”. © RupeeIQ

It is reasonable to assume that the tranche of shares sold during an IPO would be attentively priced. Thus, the company’s starting quotation on the day it goes public is a fairly accurate measure of its real value. Nevertheless, a certain variation will always be registered. In fact, “underwriters and market participants incorporate additional information into the valuation” of the company’s offering, one of these factors obviously being the perceived risk. This difference’s ratio to the initial price could be termed the first-day jump.

The scramble for yields

This notwithstanding, quotations should not fluctuate too much by the end of the first day of public trading. At least, assuming that share prices reflect a company’s activity real value and its realistic chances of growth. After all, it is illogical to suppose that a firm’s fundamentals could change massively in a matter of a few hours.

Therefore, the difference between IPO shares’ value and their quotation by end-day is an important indicator. First, the first-day jump reveals underwriters’ potential profit on the first day of trading. In other words, it unveils the extent of the “wealth transfer from the shareholders of the issuing firm to these [early] investors.” Second, it can be seen as a tool ‘quantifying’ – or better, approximating – the gap between financial markets and the real world.

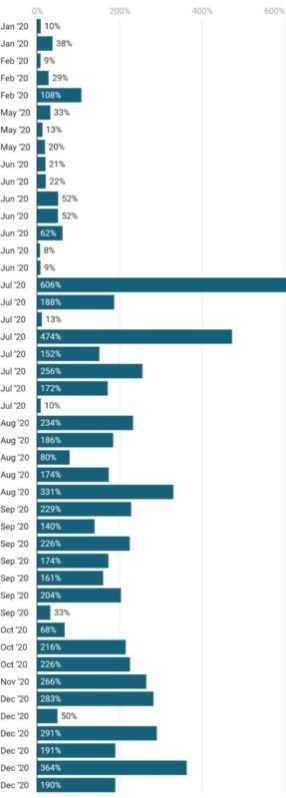

IPOs’ first-day jumps in pre-pandemic times were quite predictable. In the period between the beginning of the end of the dot-com bubble in 2002 and December 2019, tech IPOs’ first-day jumps averaged 50.7%, meaning that share prices at market closure were $2.70 higher on average. This predictability vanished into thin air in 2020.

Chart 1 In 2020 the average IPO has had a 88.4% first-day jump in price. There are worrying signs that IPOs may lead to a new market bubble once the pandemic ends. Chart: F. A. Telarico. Source: Jay R. Ritter.

During the last year, the average first-day jump was almost 88.4%. Thus, in the last 12 months, the average tech IPO realised a $20.48 first-day jump (see Chart 1). These figures are still not comparable to the 200% registered in 1999–2000. At that time, every IPO share was $80 more valuable after the first day of trading. However, “the e-commerce start-up Wish, the game maker Roblox and the home-buying company OpenDoor also plan to go public this month.” Thus, there could be some surprises.

Investors are pouring money into loss-making firms

It is worth noting that at the beginning of 2020 the landscape was much different. Pricing in the effects of the pandemic, many start-ups were “cutting back in anticipation of a slowdown”. After all, Uber and WeWork’s failed IPOs in late 2019 had ushered in a wave of layoffs. Yet it was too early to claim that the “start-up boom” was “deflating”. As central banks lavished the markets with money, investors have moved to anything that promises a positive yield.

Figure 2 Airbnb’s IPO is in many ways paradigmatic of the looming bubble. © Airbnb

Such miscomprehension of risks is paving the way for a return of the divergence between finance and the real economy. The same thing happened before the dot-com bubble burst — and “[o]nce again we’re seeing this detachment.” Airbnb’s case is paradigmatic in many ways. It shows that “[p]eople are interested in the name, not the financials.” The truth is, this buoyancy has been mostly circumscribed to the IPO market. Yet, there are reasons not to rest assured.

First, the bubble is growing and going global. Airbnb followed two other over-performing IPOs in US markets. Earlier in the same week, Kinnate Biopharma made a first-day jump of $19/share (or 282% of the IPO price). More notoriously, loss-making DoorDash jumped $87/share (or 290%). One day after Airbnb, “shares in Chinese toymaker Pop Mart International Ltd. jumped as much as 112 per cent in their debut”. Second, other established companies have benefited from the distortions that the pandemic induced in actors’ behaviour too. Amongst them is undoubtedly Tesla, which hints at an all-market compulsive buying.

Forecast

In conclusion, as some analysts have noted, 2021 will not be 2001 all over again. The bubble now involves “companies that are 10 years old with very significant revenues” as opposed to firms “that were two years old with no revenues getting a $20 billion market cap.” Perhaps it is really the case that “you can’t afford to miss out” on the opportunity to profit on some of these titles. Yet exercising caution should be the mantra. It really is “silly season” out there. Paying attention to what the characteristics of a stable profit-making company are can be a life-saver. As of now, the prospects published by the likes of Airbnb do not allow one to say that “they’re all bad companies”, but “a good company doesn’t mean it’s a good stock.”

{kind=link}