European monetary policy faces another crisis: Is the ECB effectively leading the way?

In a little over a decade the European Central Bank found itself fighting three considerable crises: the Great Recession in 2008, the sovereign-debt crisis in 2011-2012 to today’s pandemic-induced recessions. The Euro is a project without precedent and under Mario Draghi the ECB was a leading actor in world monetary policy. In 2019, Christine Lagarde became the new president of the ECB. How does she compare?

Origins of the Current Situation

The European Central Bank (ECB) is a unique monetary institution which has a variety of functions; however, the complicated intergovernmental agreements that underlie it preclude the ECB from the same scope of action the Federal Reserve Bank (Fed) and other central banks enjoy. Mainly, the ECB operates according to its multi-year strategy, which was last updated in 2003. Since that year, many things have changed in economics as a whole — and monetary policy has not stood still. The way that academics and policymakers face monetary-policy issues has transformed for many reasons. New policies were needed to respond to shifts in the underlying economic structure. But also previous strategies were unable to deliver on what they promised in a world impacted by the Great Recession and this has been the more potent factor.

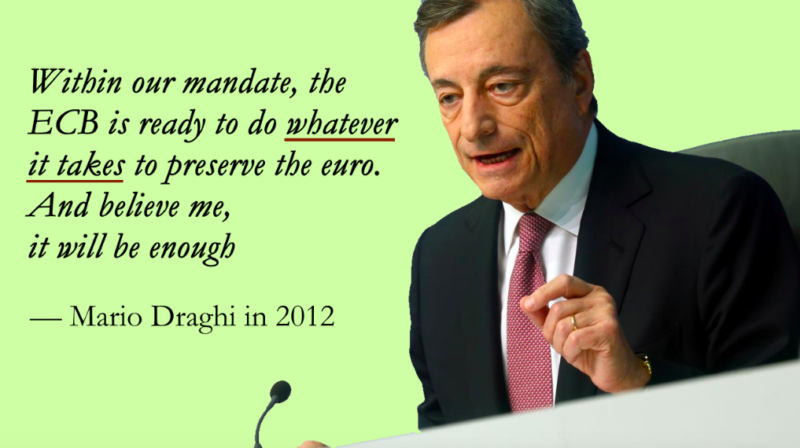

Under Mario Draghi’s presidency, the ECB opted for “unconventional” measures only “later than the USA [… as it tended] to respond following more conventional manners.” Still, many see the Italian banker as the man who “saved the Eurozone”. The ECB switched to unconventional tools in 2012, when interest rates on sovereign debt rose unchecked in several EU countries. The so-called ‘PIIGS’: Portugal, Ireland, Italy, Greece and Spain suffered greatly. Athens was on the verge of bankruptcy while a “EU’s coup d’état” replaced Berlusconi’s government in Rome. Then Draghi unleashed the “policy bazooka”: a series of extremely low-cost loans (TLTROs) and the quantitative easing (QE) programs. In 2019 Draghi left his post to Christine Lagarde. The former head of the IMF is now managing an ever -so-divided ECB.

Enter Lagarde

The new president already has a variety of challenges to overcome. Draghi left her an intact Eurozone, but also policies she simply “can’t quit”. As effective as they were, his choices did not solve all of the Euro’s weaknesses. Crucially, the “too-big-to-fail problem still exists in European banking,” which can spur instability.

In this ever-shifting environment, Lagarde has launched a new strategy revision. This is probably the only method she has to reverse some of Draghi’s policies. But it is also a much-needed move. Not only has the international monetary-policy environment changed substantially since 2003. But via the ECB Listens program citizens, academics and civil society at large will be able to communicate with monetary authorities more easily. This can be a powerful channel to foster a more dynamic decision-making process.

Despite this initiative, it looks like the ECB is following in the Fed’s footsteps without much innovation of its own. In May 2018, the Fed announced it would “let inflation run above the 2 percent goal for ‘temporary period’,” in an attempt to boost the economy. Then, in September 2020, Lagarde declared that targeting inflation “below, but close to, 2% was appropriate at a time when […] too-high inflation was [the ECB’s] main worry.” But now priorities have changed radically. Interest rates are too close to what Keynes termed “zero lower bound.” This means that they are at – or under – a level for which inflation is too low and any further monetary intervention to boost the economy is virtually ineffective. Hence, Lagarde’s ECB aims at a moderately high interest rate granting a so-called “policy-buffer” capable of restoring conventional monetary policies’ operability.

… and the pandemic

If all of that was not enough, the CoViD-19 pandemic struck more violently in Europe than elsewhere. Italy and Spain were the hardest-hit countries, with the UK and France following suit according to the European Centre for Disease Prevention and Control.

Up until now, the monetary-policy debate had been quite focused. The main issue at stake has been the combination of effects that affected the economic system in the post-Cold-War era. Namely, the attention has been on what happened to inflation, the indicator central banks act upon, albeit indirectly in various ways (setting interest and exchange rates, lending banks more or less money, buying and selling securities on the market). On the one hand, globalisation enlarged the global supply of labour and heightened competition in many sectors. On the other, technological advancements spurred a cost reduction and led to more competition as customers can compare prices on the internet. Not least in importance is that the late stage of demographic transition in Western economies weakens demand. These factors made up for the persistent disinflationary trend that the ECB had to face under Draghi.

However, Lagarde’s tenure may be transformative thanks to the pandemic. The sort of fears it triggered may very well lead to a rise in protectionism. A partial de-globalisation would shorten supply chains, which could also reduce the possibilities for supplier diversification. Furthermore, the post-pandemic political economy is witnessing a return of countercyclical fiscal policies. In fact, monetary policy can accommodate fiscal policy more effectively when interest rates hit the zero lower bound. At the same time, massive investments in the green economy should not be overlooked because they may have similar incentivising effects. In any case, Lagarde’s ECB will need to adopt new policies in order to accommodate these new necessities.

Forecast: Errors not to repeat

As hinted above, Draghi’s policies were effective in preserving the Eurozone, but they may not be apt in the new, post-CoViD context. The ECB did little more than prorogue and expand existing policies to answer the challenges brought by the pandemic. In effect, the Pandemic Emergency Purchase Programme (PEPP) is little more than a TLTRO on steroids. Together, they have stabilised the banking system while encouraging lending. However, there are not many reasons to be optimistic.

The TLTROs – and, therefore, the PEPP – are incredibly effective only because of the current negative-rate policy. Recent studies have shown that “both bank profitability and bank activity deteriorate over the course of negative rate episodes.” Thus, the current tactic of ECB cannot last for long. Thus, unless Lagarde steers the strategy-review process decisively, the ECB will repeat once again some of the mistakes it made during the early years of the Great Recession. In 2008, the Fed was faster and, therefore, more effective than the ECB in responding to the financial crisis. The ECB needs to get ahead of the curve on shaping a new monetary policy consensus, otherwise it may need to forge a new bazooka.