As US exports of liquefied natural gas have increased, policymakers on both sides of the Atlantic have viewed them as a way to decrease Europe’s dependence on Russian natural gas. However, while US exporters have some advantages in comparison to Russian gas company Gazprom, their ultimate success or failure will be determined by market dynamics. At the moment, these dynamics generally favor Gazprom’s continued dominance.

On 25 July, on the margins of a meeting with European Commission President Jean-Claude Juncker, President Trump announced that the European Union (EU) will soon be a “massive buyer” of US liquefied natural gas (LNG), in what was perceived as an attempt to ease trade tensions with transatlantic allies. This declaration boosted stocks of US LNG exporters, and which was welcomed by several high-ranking EU officials, with German Economy Minister Peter Altmaier hailing it as a “breakthrough.”

As Europe still largely relies on Russia to meet its gas needs — which have significantly increased over the past three years — many see US LNG as a way to counter Moscow’s energy leverage over Europe. Long-standing tensions between the Kremlin and Europe — most notably over the 2014 Russian invasion of Crimea — have put energy security at the center of the EU’s agenda, and there seems to be strong political will within the continent to restrain Russian gas supply.

However, Washington and Brussels’ joint willingness to boost US LNG exports to Europe might collide with the realities of the global LNG market, where Europe is in competition with the Asia-Pacific region, and which is the primary destination for US LNG exports. Moreover, if faced with the threat of losing its dominant position in Europe, state-owned Russian company Gazprom could try to preserve its market share using a number of different strategies. Despite Trump’s pledge, on the long-term, Europe is likely to remain a “last resort” market for LNG suppliers.

Are US LNG export contracts flexible enough to unseat Gazprom?

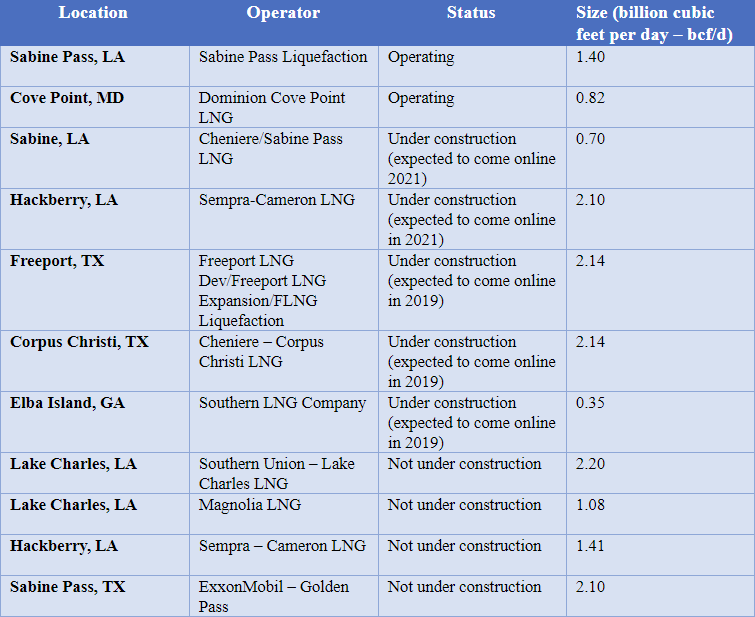

Just a decade ago, forecasters expected the United States to become a net importer of LNG to meet its enormous energy needs. The extraction of vast unconventional natural gas deposits and the development of shale-gas drilling techniques have completely reversed that view. According to the BP’s Statistical Review of World Energy 2017, at the end of 2016, the US’ proven natural gas reserves stood at 8.7trn cubic meters (cbm), equivalent to 4.7% of the world’s proven reserves. In 2017 the US became a net exporter of natural gas for the first time, and could become the third largest exporter in the world (after Australia and Qatar) by 2020, when volumes are forecast to more than quadruple, from around 14.4 million metric ton (mt) in 2017 to 62 million mt, as the Elba Liquefaction Project, Freeport LNG, Cameron LNG and Corpus Christi LNG will come online.

US LNG export terminal projects approved by the Federal Energy Regulatory Commission (FERC)

Source: S&P Global Platts, US Energy Information Administration, FERC

The surge in US natural gas coincided with a series of geopolitical events and natural disasters — including the Arab Spring, the Russia-Ukraine crisis and the Fukushima nuclear accident — which led European leaders to engage in a dialogue tackling the continent’s energy security. Since the late 1960s, Gazprom has enjoyed a near export monopoly on the European gas market, and the Brussels’ political establishment saw US LNG as weapon to increase Europe’s bargaining power in the light of Russia’s continued efforts to destabilize Ukraine.

In this vein, in February 2016, the European Commission unveiled several proposals to make Europe a more attractive market for LNG exporters. The Commission emphasized three key actions for the EU’s LNG strategy: building infrastructure around the Baltics and central and southern Europe to increase access to the global LNG market, creating an internal gas market to boost competition over LNG and lower prices, and closely cooperating with international partners to ensure a free and transparent LNG market.

One distinctive feature of US LNG exports is that they are priced differently from Russian exports. While US prices are indexed to the US Henry Hub gas spot price, Gazprom’s prices are indexed to the price of oil. This suggests that as more US LNG projects come online in the coming years, a rise in crude oil prices could hurt the competitiveness of Russian gas compared to US LNG due to higher prices.

US LNG contracts also stand out for their flexibility. They include tolling agreements, which guarantee the reservation of liquefaction capacity for a fixed rate for periods of 15-20 year on a use-or-pay basis. This means that if a European buyer opts not to use the LNG, it will only have to pay the fixed reservation fee, instead of covering the entire price of the LNG, as it would have to in a contract including take-or-pay clauses. This is particularly important, since the take-or-pay obligations included in long-term gas contracts require buyers to pay for more expensive oil-indexed gas than they actually need, even though cheaper spot gas is available in the global LNG market.

Despite political will, Europe remains a “last resort” market for LNG

Thus, US LNG can arguably serve European buyers looking to diverse their portfolio, and could also constitute an effective ceiling on European natural gas prices while remaining unaffected by to oil prices. Given that most LNG projects from the US will come online by 2020-2022, there has been some speculation that US gas will conquer the European market and considerably weaken the competitivity of Russian pipelined gas. Proponents of this argument point to Europe’s 28 large-scale LNG import terminals, which can process up to 227 billion cbm, along with the 8 small-scale facilities located in EU countries, and the 9 more terminals that could come online through 2021. In addition, the recent announcement by the European Commission that it would support 14 LNG infrastructure projects — and which will increase capacity by another 15 billion cbm by 2021 — reflects Europe’s willingness to promote itself as an attractive market for LNG exporters.

However, a key feature of US LNG contracts is that they do not include destination clauses. Given the global LNG market’s liquid nature, cargoes’ endpoints often differ from their original destinations, meaning that what really matters are commercial contracts, as opposed to physical shipments.

Despite the increased availability of US LNG for Europe, Europe has so far constituted a “last resort” market for exporters, where they can sell their surplus of LNG, whereas Asia represents the core market of US LNG exports. According to the US Department of Energy, between February 2016 and May 2018, Europe only received 11% of US LNG shipments, while Asian markets, where cargoes sell at higher prices, received 47% of all US LNG exports. Europe’s take of US LNG has decreased so far this year to less than 3% of total US LNG volume. In addition, Europe is also in competition with South America, whose share of the US LNG market currently stands at 32%, up from 31% in 2017, according to data from S&P Global Platts.

Higher gas demand in Asia has largely been driven by China’s pivot away from coal-fired power plants. The Chinese government has launched a wide range of initiatives aiming at replacing coal with natural gas in factories and for residential heating, which are the main sources of air pollution. In its National Energy Strategy unveiled in 2016, China announced that it will increase the share of natural gas in its energy mix to 15% by 2030, making it one of the most attractive market for US LNG exports.

Alongside China, countries such as Indonesia (which is expected to become an LNG net importer by 2019-2020), Thailand and the Philippines have also placed the use of LNG at the center of their economic development.

In South Asia, Bangladesh is set to join India and Pakistan as a major LNG importer, while Myanmar also has a huge potential to become an LNG importer. Therefore, in the coming years, LNG demand fluctuations in Asia will have a decisive impact on the share of US LNG in the EU energy mix. If demand in China and other Asian emerging economies was to experience a major drop, large amounts of US LNG would be avaliable to compete with Russian pipeline gas in Europe. On the other hand, if demand in Asia remains steady as some forecasts suggest — especially in the giant markets of China and India — the prospect of a surge of US LNG in Europe will be significantly diminished.

Gazprom still standing firm

Besides growing gas demand in Asia, another hurdle for US LNG Europe is Gazprom’s historically dominant position in the continent. The Russian state-run company delivered record gas volumes to EU countries in 2016 and 2017. After a decline of approximately 100 bcm between 2010 and 2014 — mainly due to a drop in electricity consumption, competition with coal, and the emergence of renewable energies — gas demand in Europe rebounded in 2015 and increased rapidly in 2016 and 2017, with year-on-year demand growth of 6% and 7% respectively.

A series of cold winters combined with increased coal-to-gas switching, and the resumption of economic growth across Europe were the main factors behind this boosted gas demand, which pushed Gazprom gas exports to an all-time high of 193.3 billion cbm in 2017. In the current state of affairs, Gazprom, which supplies more than a third of the EU’s gas, is the only player which can meet the European companies’ need for uninterrupted supplies of inexpensive gas, whether for use by power generators, space heating and cooking, or industrial consumers.

In 2016, Gazprom announced that it will seek to maintain a share of at least 30% of the European market in the medium and long term, suggesting that the company could rely on strategy similar to that of Saudi Arabia on the oil market if faced with the threat of US LNG. According to its 2017 export figures, the company is in line with its stated goal, as Gazprom’s share of the European gas market increased to more than 35%, from about 33% in 2016, making it the indisputable leader in Europe.

This reflects Gazprom’s recent strategy changes, especially the adjustment of its pricing system in response to complaints from importing countries, as well as pressure from the European Commission. At its 2018 Investor Day in London, Gazprom’s Deputy CEO Alexander Medvedev revealed that only a third of contracts are still linked to oil prices (the formula preferred by the Russians), while one third are now linked to hub prices (the market-based pricing that is now prevalent in Europe), and another third are hybrid contracts. In the long-term, this shift in pricing terms will make Russian gas more competitive in terms of price, allowing Gazprom to compete with almost any alternative source of supply.

Finally, although the political risks over the future of gas transit through Ukraine could create opportunities for US LNG to capture additional market share in Europe in the first half of the 2020s, the Nord Stream 2 and Turkish Stream pipelines projects have the potential to bolster Gazprom’s dominant role on the European gas market. The two pipelines have a respective capacity of 55 billion cbm and 31.5 billion cbm, and would substantially reduce gas transit via Ukraine. At this time, neither the threat of US sanctions nor legal efforts by the European Commission have succeeded in derailing the two projects, especially Nord Stream 2, which will ensure the transit of 80% of Russian gas exports through one route. These projects will ensure that Russian gas will be readily available in Europe, while changes to Gazprom’s pricing will enhance its desirability, even as the continent remains only of secondary importance for US exports.

Let Leo Kabouche be your guide to the issues that matter in the energy sector. The Energy Briefing breaks down the complexities and signposts the risks in key markets around the world.