The recent deal struck between Russia, Saudi Arabia, Qatar and Venezuela to prop up oil prices by freezing production levels at January levels might have a psychological effect on oil markets, but it will not secure a major breakthrough from the current deadlock.

Oil exporters such as Venezuela and Nigeria have been calling for OPEC to cut production for almost a year now. The reason is obvious: persistent low prices are slowly killing-off the economies of many oil producers. Some of them – Saudi Arabia and the rich Gulf countries – can sustain themselves longer due to their fat hard currency reserves, but others cannot.

But what is the key reason behind the Saudi and Russian decision to bring the deal to the table? It could be two-fold.

On the one hand, both Riyadh and Moscow undoubtedly bear the heavy brunt of low oil prices, and the deal would be a subtle way to reverse the current trend without giving in too much. Another potential reason is the assessment that there is not much left to achieve in terms of market share or suffocating the high-cost producers.

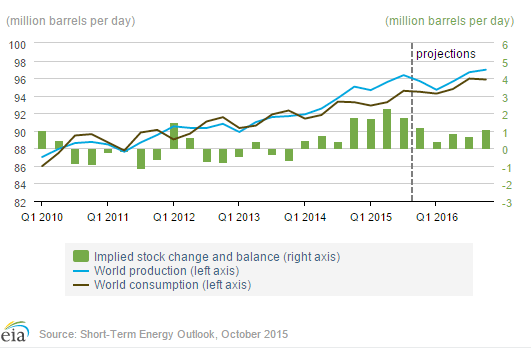

At 10.2 and 10.8 million barrels per day respectively, Saudi and Russian production is already at its peak, which makes their spare capacities extremely thin, and questions their ability to raise production further without significant investment. In the current low price oil-glut environment, and with stretched fiscal capabilities of both countries, wasting valuable capital reserves on new projects that might additionally increase production capacities is highly unlikely.

Another issue is the deal’s high level of conditionality. Not only are the countries involved not committed to cut production, but they also require others to join in before the agreement takes effect.

This will be hard to achieve. Although Iran has show some warmth to the idea, it is still not clear what Tehran might get out of it. Iran has consistently repeated that it plans to increase production by at least 500,000 barrels per day over the next six months in order to compensate for the losses incurred in the sanction years.

The US — currently the third largest global producer after Russia and Saudi Arabia — is not included in the deal, and it certainly has no plans to cut production. In addition, if the deal achieves its purpose and helps lift the prices, this will only help the US producers to quickly resume and further increase their production. Despite fervent Saudi efforts to drive out shale oil, US production has fallen by less than 400,000 barrels, from its peak in June 2015, and it still holds at above nine million barrels per day.

In terms of global supply and demand, the potential agreement does not offer any relief in the current form, at least not until global consumption picks up, and it is questionable if this can occur any time soon. Due to weak commodity prices and the slowdown in China, Europe, and the US, the OECD recently downgraded its forecasts for global growth from 3.3% to 3% for 2016.

We have therefore entered a vicious circle where low oil and commodity prices are one of the reasons for slow economic growth, while the slow growth additionally suffocates any potential for increase in oil demand that might clear the current oil glut.

Even if the deal between the oil producers takes effect, it will take much more to resolve the current deadlock. It is doubtful however if the largest producers are ready to do it.

Historical records tell us that similar measures rarely worked in the past. Both in the 1990s and in 2001 such deals quickly failed, because producers reneged on their promises.

The current oil crisis is not a product of another supply and demand cycle, but the result of a structural shift caused by the ascent of shale oil in the United States and the loss of Saudi Arabia’s ability to control global oil prices. The only sustainable way forward is establishing a supply and demand equilibrium.

In the current over-supplied markets this can only be achieved with significant cuts in production or a strong increase in demand. Neither is likely to happen in the near future. Furthermore, there might still be some unwanted consequences along the way: political and economic crises that might bring new volatilities to oil markets and the global economy.