Since the end of World War II, the US dollar has consistently functioned as a safe harbour for investors caught by any sort of turbulence. Thus, no one was surprised by its appreciation at the height of the current pandemic, which began in April 2020. And no one will be surprised if vaccine makers’ promises to end the pandemic null all those gains. Yet, the currency’s status and reputation have been weakening since the demise of the Bretton Woods Accord in 1974 to the point that, as a side-effect, COVID and its cures may be lethal for the dollar’s international dominance.

How the Dollar became Dominant

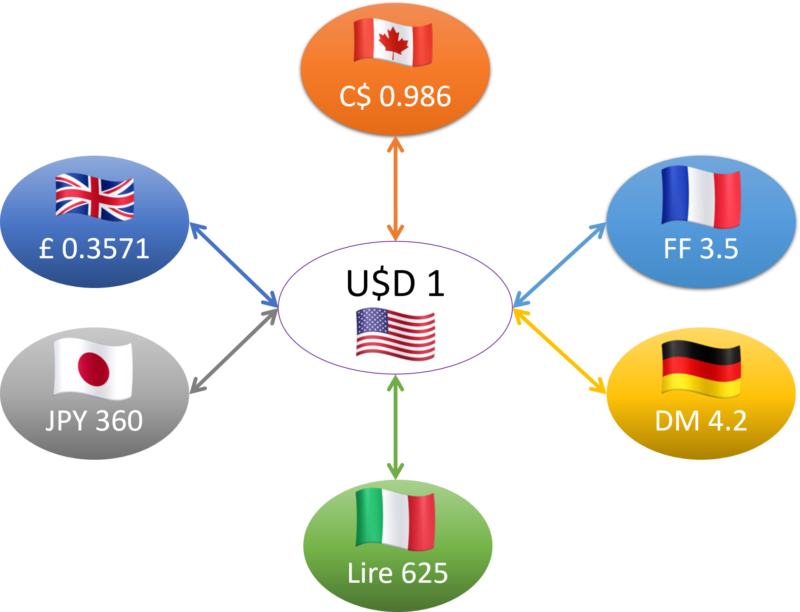

There was a time when the US was a semi-peripheral economy, mostly disconnected from the rest of the world. Everything changed after the end of World War II. As US and Soviet troops freed Europe and East Asia, a new economic world order emerged. At Bretton Woods, the US acquired a “central position […] in the emerging international financial order.” The accord established a ‘gold exchange standard’ on the ruins of the ‘golden standard’ that had collapsed in 1914–1919. The new international monetary system had two rules. First, the price of gold had to be “fixed in terms of the dollar, which was convertible into gold.” Second, each other country had to maintain a ‘parity’ in terms of the dollar. Thus, the dollar became so important that the US developed “a strong interest in maintaining the stability of that order”.

Figure 1 The ‘parity’ rates established ‘golden exchange rate’ established by the Bretton-Woods system.

© F. A. Telarico on Pinterest

Each signatory country’s central bank had to keep its currency from oscillating against the dollar. In other words, they endeavoured so that each currency could buy a certain fixed amount of dollars at any moment. At the same time, the system limited US monetary policy greatly. In fact, to make parity easier to achieve, the dollar could not abandon its “anchor”: the price of gold. Thus, the Federal Reserve could not simply decide to issue more/less notes to accommodate the necessities of the US economy.

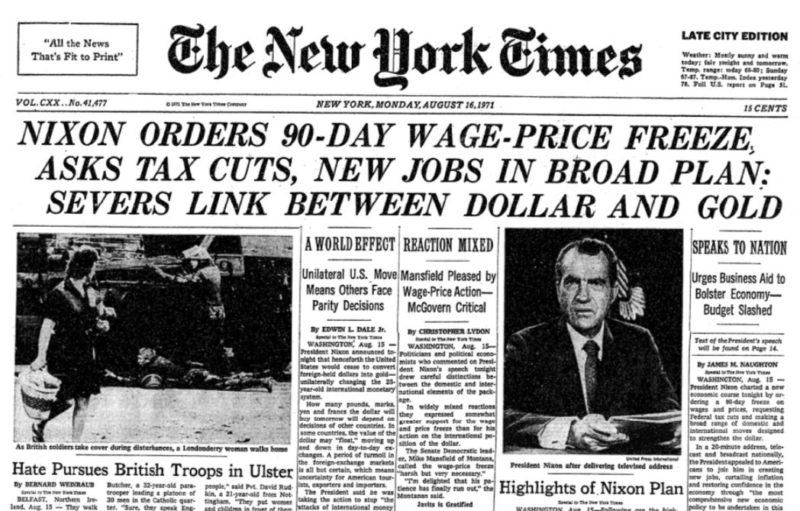

Figure 2 Cover of The New York Times of August 16, 1971. On that day Nixon announced the start of his “New Economic Policy”. Receding the bound between gold and the dollar was to become the first step towards the dismantling of Bretton Woods.

Source: Twitter

Eventually, in 1974 under Richard Nixon’s “New Economic Policy” the US forfeited the rules of Bretton Woods. Yet, the US dollar survived the Nixon Shock and kept its role as the cornerstone of international finance. As the number of currencies has kept growing and their stability has decreased, the dollar remains a safe heaven. Yet, external actors have observed a slow decline in the sense of security offered by the greenback.

The Dollar as a Safe Haven in the Great Recession

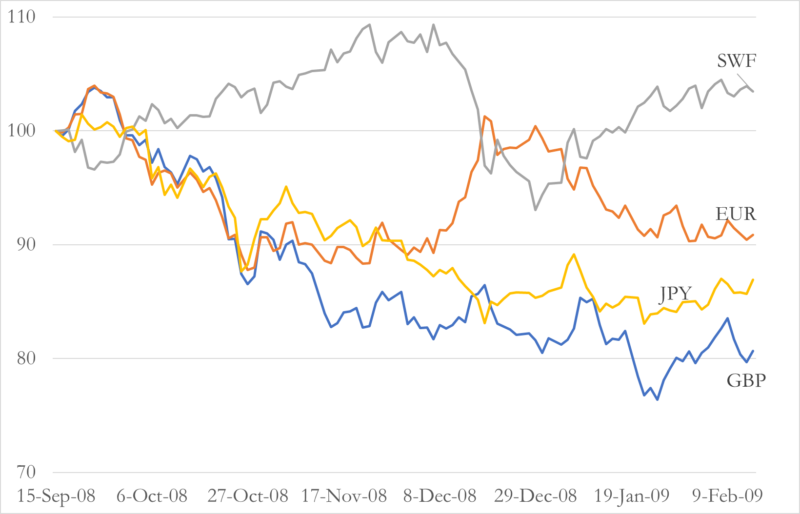

The dollar plays the role of the “world’s reserve currency” despite Bretton Woods being no more. Hence, if a crash is nearing international investors hoard on dollar-denominated assets, it could lead to an appreciation of the currency. For instance, six months after Lehman Brothers’ bankruptcy all the main currencies had lost positions against the green back. The UK pound (GBP) had fallen by 19.33%, the Euro (EUR) by 9.14% and the Japanese Yen (JPY) by 13.09%. Still, on October 15, 2008 – February 13, 2009 the Swiss Franc (SWF) appreciated against the greenback (see Figure 3). However, the SWF is itself a safe-haven investment. Therefore, this figure does not contradict the general argument for a rallying dollar.

Figure 3 The dollar was seen as a safe haven after the collapse of Lehman Brothers in 2008. In February 2009, about six months after the ignition of the crisis, other major currencies had already lost several percentage points in value against the greenback.

© F. A. Telarico via Pinterest on Official FED data.

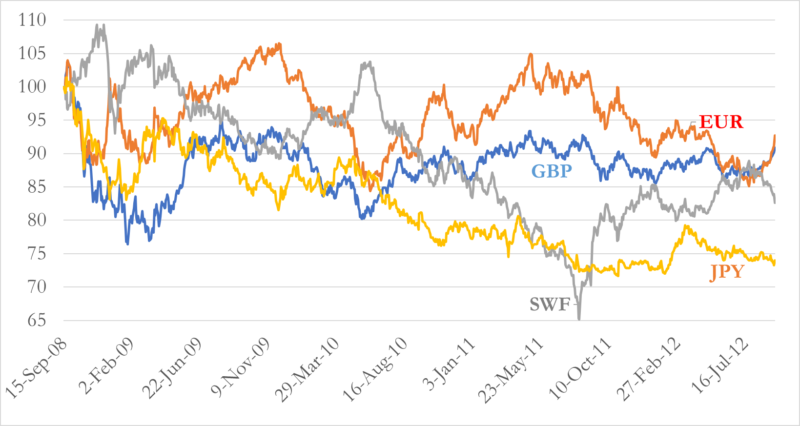

Given that the crisis kept upsetting financial markets for years after 2008, the rise of the dollar continued. In fact, by 2012 no major currency had strengthened against the greenback. Since the SWF’s value sank as well, the dollar’s value proved its pre-eminence as the safe-haven asset once again (Figure 4).

Figure 4 By September 2012, about four years after the beginning of the crisis, other major currencies were trading at much lower rates against the greenback than they used to in 2008.

© F. A. Telarico via Pinterest on Official FED data.

The Greenback and the Pandemic

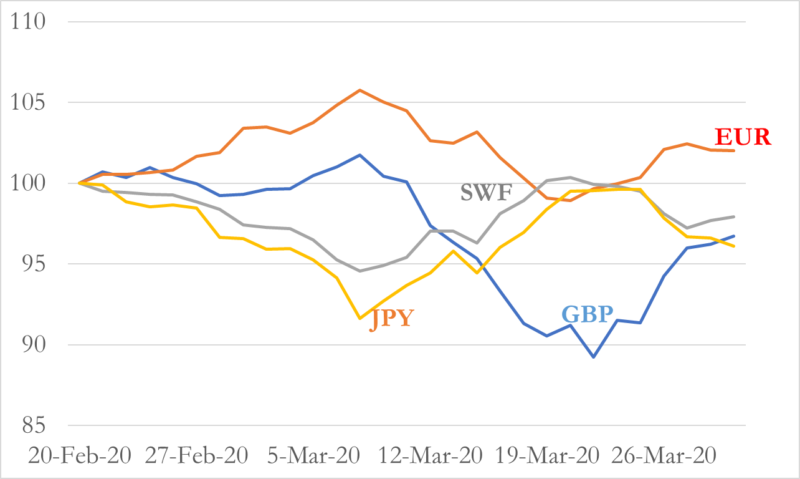

“When fears over coronavirus started to gnaw into markets, the dollar did not climb.” Between February 23 and March 31, the dollar’s fluctuation against major currencies was trendless. The GBP lost 5.12 percentage points against the dollar, and the JPY fell by the 4.21%. Meanwhile, the Euro rose by 1.61%. The SWF’s slight slump (-1.54%) reinforces the hypothesis that investors still perceived the market situation as favourable (Figure 5).

Figure 5 In February–March 2020, at the onset of the pandemic crisis, the dollar went through a period of trendless fluctuation against other major currencies unlike what happened in 2008.

© F. A. Telarico via Pinterest on Official FED data.

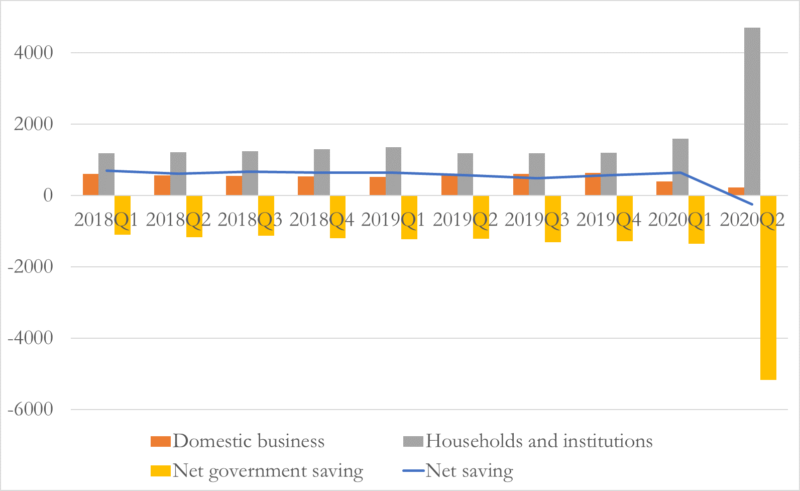

To make sense of why this happened one has to understand that the dollar was structurally feckless in 2020. In fact, the estimates of the Congressional Budget Office for 2020–2030 are not reassuring on at least two points. Internationally, its role as a global reserve currency has been challenged with some success by China and Mario Draghi’s ECB. Meanwhile, domestically, the stock of net savings has decreased (see Figure 6) while current-account deficits have ballooned.

Figure 6 By 2020, the stock of net savings has decreased in the US since 2018.

© F. A. Telarico via Pinterest on Official data by the Bureau of Economic Analysis at the US Department of Commerce.

Eventually, a senior analyst at Deutsche Bank had to admit that many had “underestimated how acute dollar-funding pressures would become.” Surely, there are some who have overestimated the greenback’s weakness. In effect, as the situation worsened in Europe and elsewhere, demand for dollars increased exponentially.

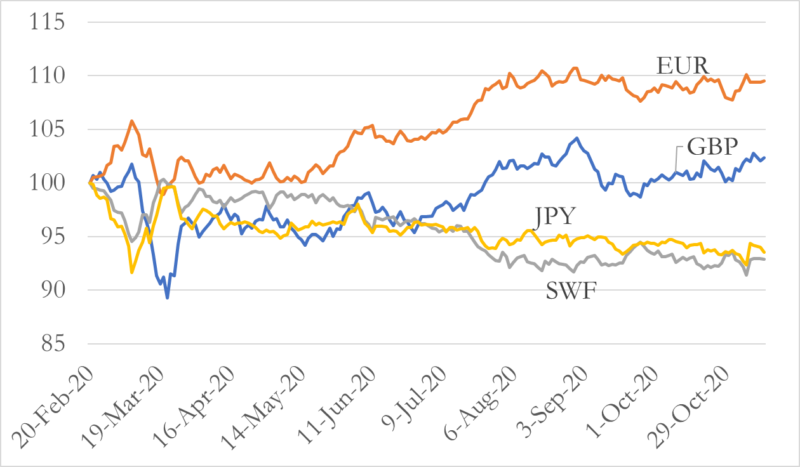

Nevertheless, others have exceeded in doing the contrary in lamenting a “dollar shortage more difficult [to fix] than policymakers think”. In effect, the dollar did not outperform other currencies by the large margins of 2008–2012. Investors started to price in the risks of regime instability in the then-forthcoming presidential elections. Thus, the dollar became less appetible than other safe-haven investments. Subsequently, when one of the two sides reported a sufficiently-convincing victory, the perception of risk lowered. Thus, buyers ushered in more-risky assets. On the contrary, some currencies were stronger in comparison to the greenback in November than they had been in February. The GBP appreciated by 2.32%, and the Euro by a staggering 9.51% (see Figure 7).

Figure 7 The dollar didn’t pick up strongly against other currencies in 2020.

© F. A. Telarico via Pinterest on Official FED data.

Forecast: Monetary Side-Effects of COVID Vaccines

What was described above is a long-term decline of the dollar, which is likely to have far-reaching geo-strategic implications. Some Wall Street analysts and several banks forecast that COVID will accelerate these pre-extant tendencies. For a start, “it’s expected that the dollar will [lose value …] as the economy recovers.” However, Citi bank launched the provocative idea that “the dollar will decline 20 per cent” next year alone. According to Deutsche Bank, when a vaccine will be available – perhaps more than one – the environment will be “perfect […] for a rally in risky assets, a weaker dollar and stronger growth-sensitive currencies through the end of the year”. A weakening dollar will favour US exports, but also contribute to the destabilisation of the world economy. Investors ought to be ready soon to ditch the dollar and grab substantial gains from a currently overvalued currency and related overpriced assets.