COVID-19 and the green revolution: A new energy order in the making?

The pandemic has accelerated an ongoing switch towards greener energy, to the point that some foresee a “new energy order” in the making. But these calls are likely exaggerated, with traditional energy sources predicted to stay dominant.

The pandemic and energy markets

It is no exaggeration to say that the “American century” was also oil’s century, with so-called ‘black gold’ orienting economics and geopolitics. But CoViD-19 may inaugurate a new energy world order that will phase oil out.

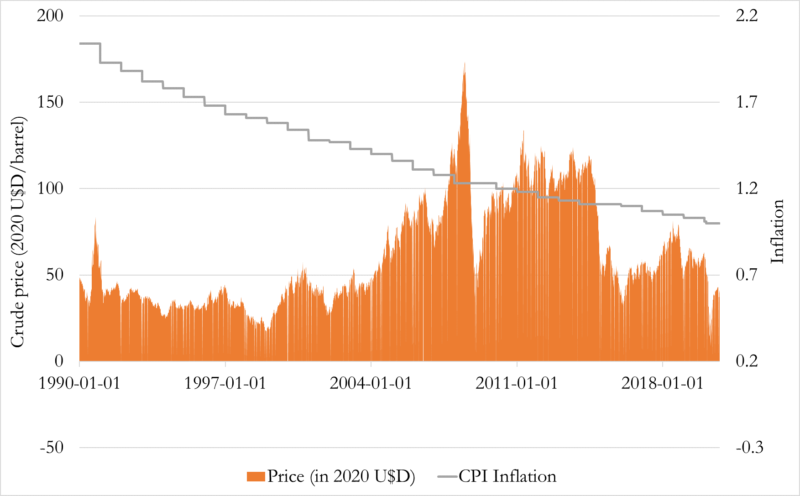

West Texas Intermediate (WTI) crude oil prices from 1990.01.01 to 2020.09.21, adjusted for Consumer Price Index (CPI) inflation. © Fabio A. Telarico Data: Federal Reserve Bank of St. Louis; U.S. Bureau of Labor Statistics.

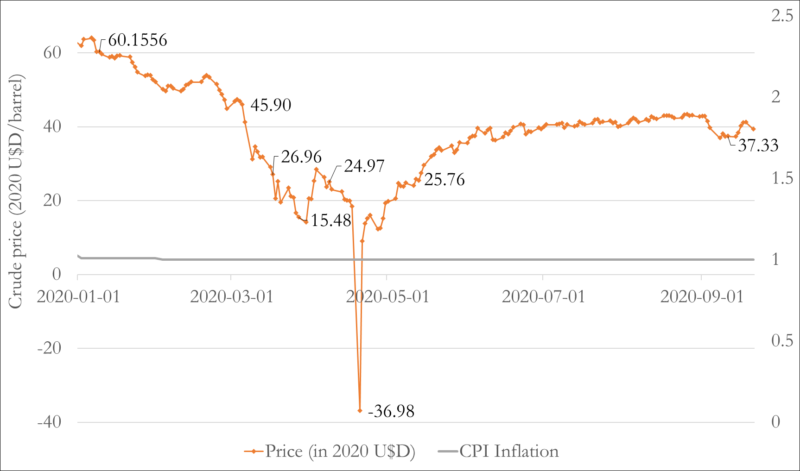

As the pandemic struck parts of Europe and North America, oil demand worldwide collapsed by almost 12 million barrels per day year-over-year and prices fell below $10/barrel. Amid a “significant crude surplus”, Russia fought a commercial war with Saudi Arabia, and the oil price “crashed the most in 29 years.” The fall was so abrupt that between January 3 and March 20, prices collapsed by 158%, or 1.46% per day (see Figure 2).

Figure 2 Crude Oil Prices (West Texas Intermediate, WTI) from 2020.01.01 to 2020.09.21, adjusted for Consumer Price Index (CPI) inflation. © Fabio A. Telarico Data: Federal Reserve Bank of St. Louis; U.S. Bureau of Labor Statistics.

Politicians’ “green” responses met by entrepreneurs’ timidity

The seismic waves destabilising the energy market pushed politicians’ rhetoric towards a ‘green energy revolution’. As might be predicted, the EU conquered an early lead. Brussels targeted a reduction in “greenhouse gas emissions by at least 55% by 2030, compared to 1990 levels.”. Meanwhile, Joe Biden, Democratic president-elect, promised to decarbonise the USA’s economy, embracing the Green New Deal.

However, China is also currently pioneering the clean energy sector, with “deployment and investment in renewable energy” an area in which “China is genuinely interested in leading the world.” To this end, Xi Jinping has announced plans to cut “emissions to nearly zero by 2060.” Besides tightening the previous target to cut greenhouse gases, Xi anticipated “higher spending on green power.”

In the meantime, large energy conglomerates are accommodating the shift. Danish Ørsted, Italian Enel and Spanish Iberdrola are building giant wind and solar farms all around the world. But other private investors seem more sceptical or, at least, prudent. In fact, only one in three EU firms have set ‘green’ targets for 2025. The same can be said of the US. In effect, US firms and the government have done little to curb emissions, leading to a 3.2% net increase on the 1990 Kyoto baseline. President Trump has stated that he is proud of the USA’s “energy dominance” as “the number one energy superpower in the world”.

Green Revolution: hopes…

Recent estimates underline the connection between hydrocarbons and greenhouse gases. Excess atmospheric carbon dioxide (CO2) exists “primarily because of emissions from combustion of fossil fuels and cement production”. CO2 is “responsible for about 82% of the increase” in the greenhouse effect over the last decade.

Thus, the ‘green energy revolution’ can be branded as the way towards a “better future for all.” Since “global warming is primarily due to fossil fuels,” clean energy should reduce the pace of global climatic change. Consequently, it promises to reduce or contain droughts, floods and connected migratory fluxes (so-called “climate refugees”). Furthermore, some argue that “it is more difficult to control, cut the supply or manipulate the price” of renewables. Thus, the switch will “reduce the scope for conflict among states”. Clean energy’s inherent geographical diversification should be good for political stability too.

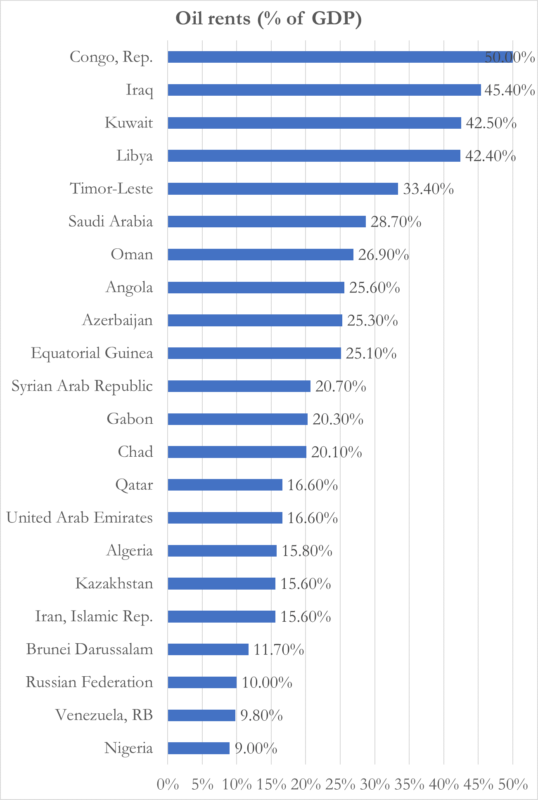

Figure 4 The countries with the heaviest dependence on oil according to the World Bank, measured as the difference between the value of crude oil production at world prices and the total costs of production. © Fabio A. Telarico Data: World Bank

… behind a risky bet

But, in reality, this is one of the riskiest gambles in recent geo-economic history. About 10% of humankind lives in – often poor – countries whose wealth depends heavily on hydrocarbon exports (see Figure 4). The shift will cause a decline in petroleum revenue that “could also lead to political instability” and economic woes in already volatile commodity-exporting regions. It could also threaten already vulnerable people’s livelihoods in so-called “petrostates”.

Moreover, a very fast transition could have even riskier consequences for the economic and political status quo. A sudden switch away from combustion, if it happened now, would see Beijing benefitting more than any other country. In effect, China has

a leading position in manufacturing, but also in innovation and deployment of renewable energy technologies. It is the biggest location for renewable energy investment, accounting for more than 45% of the global total in 2017.

Moreover, Chinese firms dominate the production of lithium-ion batteries from mining to assembling. Thus, in light of the ongoing power- and wealth-shift eastwards, the ‘green energy revolution’ may accelerate China’s reach for the throne.

Oil will still move the world of tomorrow

To its discredit, oil fuelled much of the last century’s instability. Without the two “oil shocks” of 1963 and 1966 the world economy would look more Fordist than it does. Meanwhile, the Middle East would have been spared some foreign interventions and the 60,000 pairs of US boots still on its soil. However, the international economic system built on oil has improved in resilience and stability. For the decades after 1945, countries were exposed to “high risk” due to their oil supply sources not being “well diversified” — as the 1979 Iranian Revolution showed. Under the “OPEC+” label, Russian-Saudi cooperation tried to remedy this instability and strengthen the global economic system. But, as mentioned above, Moscow’s interests do not always align with Riyadh’s.

Yet, what OPEC+ could not achieve is now being provided by the exploitation of shale oil and the commercialisation of liquified natural gas (LNG) in the US. These new sources of energy are “more flexible”, make transportation easier and reinvigorate market competition. Consequently, as the market shrinks, the race is set to turn sour. Saudi oil is cheap to produce, but the government budget’s break-even point is around $80–85/barrel. Such a situation is not sustainable. Nonetheless, the“global energy transition does not mean the end of the petrostate”. Instead, the future will belong to the cheapest possible “clean” crude producers on the market.

Forecast

In conclusion, predictions are mostly overstating the reach of the ongoing shift. About 85% of the world’s energy still comes from fossil fuels. Growing by about 3% this year, renewables make up 5% of the world’s energy mix. Meanwhile, talk of China becoming an “electrostate” is devoid of substance as its economy is far too diversified for it to be the ‘petrostate of the green energy era’. A new energy order is indeed in the making. But, being fraught with geopolitical consequences, its birth will not come without complications. In the meantime, investing in hydrocarbon production may become a rather complex choice requiring political and geo-economic awareness, but it will still be profitable for wallets of all sizes.