Quantitative Easing (QE) in the Eurozone is not perfect, but a better approach may create too much risky exposure for the European Central Bank (ECB) in a manner that is unlikely to please the creditors now fretting about the effects of low interest rates. Ultimately, monetary policy can only be a temporary solution before a more resilient political consensus can be reached about the future of Europe.

Targeted Quantitative Easing, the ECB’s capital key approach and political inertia

The last week of September 2016 was marked by German complaints to Mario Draghi about the negative effect of the ECB’s asset purchases, known as Quantitative Easing (QE), and negative policy rates on savings and pensions. The ECB’s policy is flawed indeed — but these legislators would not welcome the better solution of a more targeted form of QE. More fundamentally, the fact that QE is starting to look increasingly like a permanent policy tool rather than a temporary relief to facilitate reform may threaten long turn productivity and political reform.

Monetary policy in the Eurozone: Orthodox policy tools and Quantitative Easing

In the aftermath of the sovereign debt crisis, the ECB has pursued a consistent and increasingly aggressive policy of market stabilisation through increased liquidity. The approach has relied on lower reserve ratios, long-term loans and since mid-2014, negative interest rates on the overnight loans it offers EZ banks.

All of these actions have been supplemented by QE, which is supposed to improve the real economy in three different ways: by improving confidence and expectations, by raising the value of assets used as collateral and thus lowering borrowing costs, and by increasing the amount of cash being lent. The ECB’s € 80 billion-a-month QE policy is conducted through four dedicated asset purchase programmes focusing on covered bonds (CBPP), asset backed securities (ABSPP), government bonds (PSPP) and since March 2016, corporate bonds (CSPP). The scale of these programmes has been extensive, stretching its balance sheet from € 1.9 trillion in July 2009 to € 3.3 trillion at the end of September 2016. These actions have picked up pace recently, with the share of the ECB’s balance sheet taken up by QE-related asset purchases almost doubling to 43% during the last year. At close to € 1 trillion, the PSPP is the largest component of the ECB’s QE.

The ECB’s capital key approach to Quantitative Easing

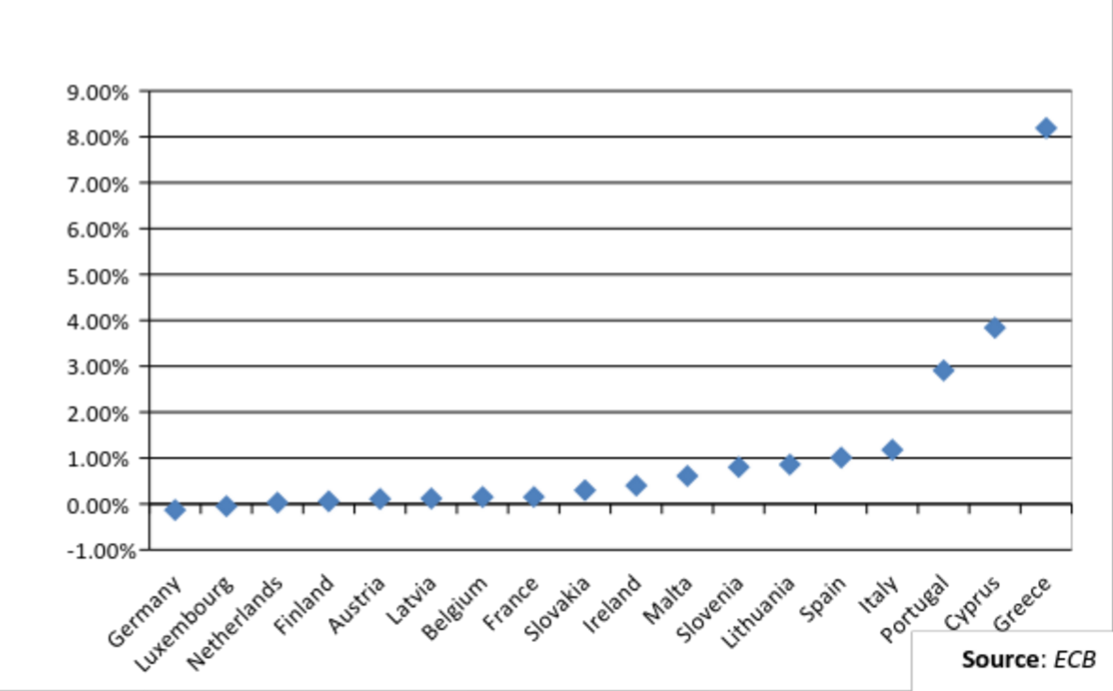

The ECB, contrarily to the Fed, has decided to buy assets along a quota system. When the ECB buys assets across national markets, it does so in proportion to its capital key, which defines how much of its capital is contributed by any given country’s central bank. The biggest contributors to the ECB’s capital are Germany (18%) and France (14%), followed by Italy (12%) and Spain (8%). Portugal, Greece and Ireland contribute a mere 1.7%, 2% and 1%, respectively. So when the ECB conducts QE through government bond markets, it has to buy more German bonds, rather than Portuguese or Greek bonds. This is patent in the distributions of the Public Sector Purchase Programme (PSPP) initiated by the ECB in March 2015.

The result of the capital key approach is that the ECB’s QE ends up being relatively regressive. Ignoring political discussions, the result is that stable markets get flooded with cash they do not need, pushing long-term rates too low, or even below zero (Germany and Luxembourg) while less stable markets (Portugal and Cyprus) may not get the cash they need avoid volatility. Greece’s woes are compounded by the fact that its present credit rating does not even qualify it for PSPP purchases at the moment.

Quantitative Easing, risky trade-offs, and the incomplete union

Quantitative Easing, risky trade-offs, and the incomplete union

German legislators are not wrong when they fret about low interest rates and the negative impact that the ECB’s QE has had on savings and pensions: QE in the Eurozone is even more suboptimal than in the USA. It stopped unimaginable financial and sovereign debt crises from devastating the continent but beyond that, its regressive nature undermines its success. However, one of the appeals of the capital key approach is that it allows the ECB to spread the risk of its balance sheet exposure. It is unlikely that conservative German politicians will welcome a solution to their problem that involves a more targeted approach to QE, focusing asset purchases exclusively on troubled countries.

This trade-off between higher German interest rates and higher ECB risk exposure is not something they are likely to enjoy, but it is possible. Such a targeted approach was taken in the first emergency “Securities Market Programme” (SMP), which was relatively unconditional but ad-hoc, limited in scope and duration, did not follow the capital key approach and had a degree of success. Further motivated by an increased scarcity of government bonds in stable EZ economies, rumours about abandoning the capital key come and go every-so-often as other alternatives are tried so as to not antagonise German politicians any further.

The political risk of complacency is not only relevant for debtor countries. Mario Draghi’s call for European solutions to “common supranational challenges” such as completing the single market puts German legislators in the uncomfortable position of having to discuss international integration at a time when the electorate is increasingly turning inwards. However, because the crisis appears to have passed and the inequalities and instabilities of the EZ have become routine, this pressing need is ignored, allowing dangers to continue to fester and fault-lines to deepen.