Tectonic shifts in the global coal market are underway, posing a series of questions for traditional coal supply markets.

Coal has historically played and continues to play a central role in the industrialization and development of nations. A convergence of factors, including China’s spectacular rise, has however had a significant destabilizing effect on the global coal market.

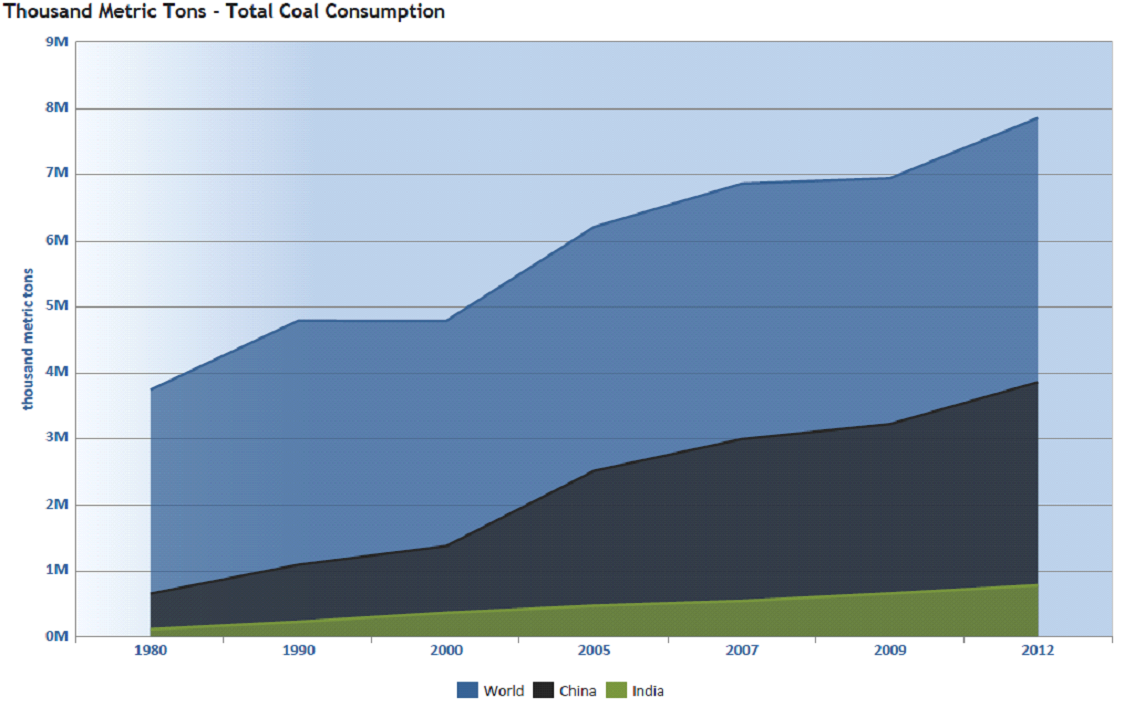

New era for coal

For much of the recent history, global coal export demand was driven by European and Japanese post-war reconstruction and the emergence of the Tiger economies of South Korea and Taiwan. China and, until recently, India, have been late but significant players in the global coal market.

Source: Knoema, World Bank

Accounting for 75% of China’s and 73% of India’s primary energy mix , recent EIA statistics (2014) reveal that China alone consumes and produces more coal than half of the world’s total coal production of 7 876 Mt – with new estimates 14% higher than previously reported. India, too, has become a major producer of coal, increasing output from 116 Mt in 1980 to a current level of 600Mt – with an ambitious target of 1.5 billion Mt set for 2020.

What distinguishes both China and India from traditional coal markets in Europe and Asia, however, are their relatively high degree of historical and continued coal self-sufficiency. Unlike South Korea at 98% or Japan at 100% dependent on imported coal, China and India rely on imports for a total of 7% and 11% respectively.

Coal’s continued relevance

Often the debate on coal’s future centers on pollution, climate change, and the increasingly low-cost attractiveness of renewable energy production. Though these arguments are valid, over 473GW of coal power capacity was brought online in the period 2010-15, led by China and India. A further 338GW is currently under construction, rendering coal an indissoluble cog in global energy production in the medium to long-term.

China alone accounted for 297GW of coal power capacity in the period. By way of comparison, the entire US coal fleet is 315GW, with China annually adding on average roughly half (49GW) of the UK’s total installed capacity in coal power alone.

This also does not take into account the role of coal as a fuel source used in industrial furnaces for smelting and baking processes, or as an additive in chemical derivatives and industrial applications.

Ironing out inefficiencies

In China, pollution, climate change, and overcapacity concerns have, however, provided impetus for the country to review the role of coal in its energy mix. With its total installed electricity capacity increasing on average by 10% in the period 2007-2013 to 1257.68GW, China has halted the construction of over 200 approved coal fired power stations until 2018.

Halting the approved build program with combined electricity output of 105GW – equivalent to 73% of Africa’s total installed capacity – must be seen in light of arguably the most significant growth phase in modern industrial history, with total installed electrical capacity more than tripling since 2000 (298GW). The peak of this growth phase (2007-2011) saw China building the equivalent of two 500MW coal power stations per week.

The hiatus in new plant construction comes on the heels of significant losses in plant utilization rates, plummeting from 60% in 2011 to 49% in 2014, expected to fall to 46% in 2016. Coal power plants with less than 100MW output have also been earmarked for closure, with 60GW of coal power announced to be removed from the grid in the 2016-2020 period.

In a similar vein, over 4300 small, inefficient coal-mining operations have been earmarked for closure in addition to the 7250 that have been closed in the last 5 years, slashing a further 560 Mt. In total ,1.3 million coal and 500 000 steel jobs will be lost as part of a broader economic restructuring. India too has been struggling with inefficiencies following a remarkable growth phase that saw its total installed electricity capacity practically double in the period 2006-2014, from 124GW to 245GW.

Along with China, India’s coal-fired power stations are among the most inefficient globally. Due to bottlenecks in the supply of coal to power stations by rail, with over 50Mt of coal stranded at mines in 2014, modernization of existing coal power plants has been identified as essential to keep pace with an electricity demand of 4.9% per year.

Further corrections to the global coal market are expected in the short-term as China and India grapple with weighty inefficiencies at mine, power plant level and factory level.

Past the peak

Significant cutbacks on imports are expected to increase, with annual Chinese demand down 35% in 2015, registering a total drop in coal demand of over 5% in the 2014-15 period and set to continue into 2016. With coal imports down 34% annually, India’s Prime Minister Modi recently declared war on coal imports, stating that no imports will be allowed past 2019.

Source: eia

This trend towards energy autonomy can be seen in part as a drive to reduce risk of future shocks due to price volatility as witnessed in the previous decade with coal reaching an all-time high of over $160 in 2008.

Source: Index Mundi

Counting the cost

The key consideration for the future of coal rests on balancing supply with global demand. As developed economies wean themselves from coal, traditional export markets are on the decline. Recent reductions in demand from China and India, with stockpiles rising at the world leading coal terminals, have resulted in coal exporters scrambling to find customers.

High-cost players are being eliminated in emerging and developed markets. One such example is the recent liquidation of Peabody Energy with a market cap of $20 billion in 2011, reduced to $38 million in early 2016. Big coal has seen a steady decline in the US, with the Obama presidency’s effort to shutter the industry hastening the end. A shale gas surge and the significant drop in crude oil prices have also had a significant deleterious effect on coal’s place in the US and world’s energy mix, with 2015 declared the worst year for US coal.

Tough environmental regulations and sanctions in developed economies, a competitive renewable energy sector competing directly with coal, and the recent signing of the Paris climate accord have all diminished coal’s place in many developed economies. December 2015 saw the closure of the UK’s last deep coal mine, Kellingley colliery. Most recently, eastern Europe’s largest private coal miner, Czech-based New World Resources, scrambled to secure a bailout because of the need to support 13 000 jobs.

Shifting centers of production

A re-balancing of Chinese and Indian coal markets in the short to medium-term could send significant shockwaves through the global coal market. Several uncertainties could prove troublesome for global coal, including the extent of the glut in Chinese and Indian domestic coal markets. Addressing the significant inefficiencies in existing electricity-generation infrastructure could also flatten demand for coal further. Possibly more troublesome, however, is the prospect of China and India becoming net exporters of coal.

For the two largest exporters of coal, Indonesia (16% of global coal exports) and Australia (13%), with export markets accounting for 80% and 72% of total production respectively, the risks are high. With coal prices down 60-90%, the leading investor in Indonesian coal, BHP Billiton, has recently in a shock announcement signaled its intention to exit from Indonesian coal – a key supplier to China.

Source: eia

For the remaining top exporters including Russia, South Africa, Colombia and a beleaguered US, the impact could be equally negative, resulting in mine closures, retrenchments, and the loss of a key foreign exchange earner. Much will depend on the reliability of the short-term coal fundamentals emerging from China and India.