“Vladimir Putin at the Russian Energy Week International Forum (2019-10-02) 04.jpg” by The Presidential Press and Information Office

As Brussels and DC continue to expand their sanctions package they risk hurting the Russian people more than the Russian state. To target the Russian state, the West must consider oil and gas export restrictions and stop insulating the Kremlin’s main source of income through SWIFT loopholes.

Russia as a gas station

In 2014, John McCain memorably stated that Russia is a gas station masquerading as a country. This claim holds true even more today than when McCain said it eight years ago. In 2021, $1.18 Trillion of Moscow’s total $2.37 Trillion government revenue was collected from oil and gas. This accounts for almost exactly half of the government revenues in 2021. By comparison, in 2020 (the most recent year available), “the oil kingdom” of Saudi Arabia received 53% of its government revenues from oil and gas.

While the high federal revenue that Russia generates from oil and gas may surprise some readers, what is even more striking is that oil and gas only account for between 15-20% of Russia’s GDP. Thus, a sector that constitutes less than a fifth of the economy is filling around half of Russia’s coffers. Compare this to Saudi Arabia, where 53% of Riyadh’s funds come from oil and gas but the sector accounts for a proportionate 50% of Saudi’s GDP. Putin’s public takeover of Russian oil and gas in the early 2000s led to disproportionate funding from the industry which gave it the moniker of a “rent-seeking revisionist.” Thus, perhaps it is more accurate to say that the Russian State is a gas station (which also sells substantial amounts of steel and commodities) masquerading as a country.

Putin’s ability to “capture” Gazprom—Russia’s largest company—serves as a telling example of the concentration and politicization of the Russian oil and gas industry. In 2000, Putin installed his close associate Dmitry Medvedev as chair of the company, a position where he remained until he relieved Putin as President for one term in 2008. During his tenure at Gazprom, Medvedev consolidated the industry with the Kremlin’s blessing. Once Gazprom reached monopoly status, the company began to use its prices as a political tool. It artificially increased domestic supply to lower costs and garner political support while simultaneously limiting supply and raising prices to certain countries in Europe. Some states such as Germany have perennially paid for expensive gas, others such as Ukraine, Moldova and the Baltic states have faced intermittent gas shortages and price hikes due to politically motivated causes. All the while Gazprom substantially increased its contributions to the Russian state, which accounted for a whopping 25% of Russia’s federal tax revenue in 2011.

Former Deputy Prime Minister and close Putin Associate Victor Zubkov currently serves as the chairman of Gazprom. In 2020, the state-owned company accounted for nearly 90% of all of Russia’s gas production. The oil industry is not as concentrated as the gas sector, but it is still largely controlled and directed by the state. In 2020, over 80% of Russian oil production came from the following five firms:

- Rosneft: majority state-owned

- Surgutneftegas: close ties to Kremlin

- Gazprom: majority state-owned

- Tatneft: wholly state-owned

- Lukoil: it’s complicated

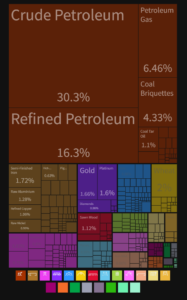

To better understand Moscow’s economic lifeblood, view the export chart below. In 2019, Russian exports totaled $407 Billion, which translated to 28% of Russia’s GDP. Of these exports, 63% were fuels and energy products (of which crude oil and natural gas accounted for 26 percent and 12 percent respectively). Thus, almost two-thirds of Russia’s exports are in an industry that is captured by the state and where revenues will flow directly into Moscow’s coffers. Base metals and steel are another notable source of export revenue for Moscow at roughly 15% of exports, but they pale in comparison to the oil and gas revenue.

Figure 1: 2019 Russian Exports by Category (sum $407 Billion)

Why sanctions should not target the Russian population

While the White House and Treasury have moved away from using the term “targeted” to characterize the sanctions regime, they still argue that the objective of sanctions is to manage Putin’s long-term strategic ambitions, which would presumably come about through degrading Russia’s federal government funding. Yet the current sanctions regime broadly inflicts pain across several sectors in the Russian economy and insulates the Russian government’s largest income stream. Some may question whether the sanctions regime should be precise, after all, wouldn’t sanctions that hurt the Russian population lead to discontent and possible regime change?

There are several reasons why broad sanctions regimes should be avoided, but the principal reason is that they come at the expense of large swathes of the population who do not have the power to influence policy and generally they don’t work. The literature shows broad sanctions to be unreliable in forcing policy change. Moreover, measuring for GDP decline after sanction imposition is unfulfilling given the many confounding variables such as commodity prices. For instance, the weak economic growth in Russia in 2014 and 2015 has now been attributed to low oil and gas prices, not sanctions as some originally thought.

The history of sanctions with broad effects has resulted in nationalist fervor and people rallying around the flag rather than people voicing discontent towards their own government. Such sanctions expand the role of the state in the domestic economy through import substitution and more autarky. By contrast, sanctions that target gas and oil specifically would damage the state’s capacity to govern and cause reputational loss to Putin without inflicting widespread economic pain. The oil and gas sector in Russia accounts for nearly half of federal revenues but only a small percentage of GDP and merley 5% of the workforce.

The current sanctions regime is targeted in name only

Of the sanctions provisions undertaken, few are targeted. The war on the ruble and runaway inflation hurt Russian consumers. In fact, the only people spared are the ultra wealthy who has foreign-denominated assets squirreled away. Sanctioning Russian oligarchs and politicians seems like a reasonable strategy to sow discontent among the Russian elite, but this strategy was implemented in 2014 and now reaps diminishing returns. Security Council Secretary Patrushev, FSB Director Bortnikov, and Director of Foreign Intelligence Naryshkin, along with most of Putin’s inner circle, have already been blacklisted by the US treasury in response to their role in the annexation of Crimea.

In a similar vein as Alexander Gabuev of Carnegie Moscow points out in The Economist, separating the Russian consumer from Western goods can have the unintended consequence of helping Russian oligarchs fill the void through import substitution. One striking example is the booming growth of Russian agribusiness since the self-imposed reciprocal food bans that Russia imposed in 2014. Barring Russian travel and especially Russian student exchange almost exclusively hurts the Russian middle class and coincidentally ends important forms of cultural exchange with the West.

Perhaps tech sanctions are the most successful example of a targeted sanction. While blocking Russian access to high-tech goods and specifically semiconductors is a good start, it has shortcomings. Russia currently buys 70% of its semiconductor chips from China (albeit lower quality chips). Furthermore, most of the world’s neon gas and pallidum, which are integral to the semiconductor supply chain, are sourced in Russia and Russian-occupied Ukraine, making long-term tech sanctions impractical.

Finally, the SWIFT “ban” works in precisely the opposite way of a targeted sanction by specifically excluding oil, gas, and mineral sectors. As Columbia Economic Historian Adam Tooze said, these provisions “must indicate to (Russia) that the West does not really have the stomach for a painful fight over Ukraine.” While this is not a comprehensive list of all of the Euro-American sanctions, the trend is clear, the lifeblood of the Russian state remains flowing.

Targeted sanctions are oil and gas dependent

9 of the top 10 richest men in Russia (not including Putin) are either in the steel or energy industry. Furthermore, Putin’s wealth by all estimates comes at least in large part from the energy sector. While it may be impossible to find where he hides his assets, sanctioning Russian oil and gas would prevent Putin from amassing even larger sums. There is no better-targeted tool than restricting Russia’s oil and gas exports. Commentators argue that the so-called “nuclear option” of sanctions has already been deployed but this does not match reality.

According to Javier Blas of Bloomberg, in the first 24 hours of the Russian invasion alone the EU, UK, and the US collectively bought more than $350 of Russian oil, $250 million worth of Russian natural gas, plus tens of millions of dollars worth of other commodities. The sum of one day’s worth of ongoing energy exports from Russia dwarfs the military and humanitarian assistance that Western governments have sent to Ukraine. The $700 million recorded in one day is also larger than the entire value of arms and military equipment shipments made by the US in 2021.

These observations are not made to downplay the actions of Western governments, but rather to show the scale of energy dependence that the West and primarily Europe have upon Russia. Self-congratulatory messages from DC and Brussels lessen the urgency to act and even obscure the pivotal issue of energy dependence altogether. In the short-term, it is possible that the US will be able to end energy imports and financing in its domestic markets. The EU, however, is not in a position to take steps to wean itself off Russian gas at least until spring comes. Europe is also unlikely to find an alternative oil source in the short-term unless there is a sudden change in Venezuelan and Iranian sanctions negotiations. In the medium-term, Europe can invest in larger LNG terminals, embrace alternative energy sources such as nuclear and increase its strategic reserves to become less susceptible to Russian energy coercion.

The risk of not including provisions for oil and gas in the sanctions regime is that NATO could resort to much riskier measures including limited military engagement if policymakers think that all economic deterrents have been exhausted. War optimism is rife in the US and according to the latest poll data, 74% of Americans support creating a no-fly zone over Ukraine which could lead to a disastrous military escalation between NATO and Russian air forces. The West has long been dependent on Russian energy exports and this could be the final wake-up call to change course and weaken Putin’s ability to impose his will on Europe through energy coercion.