The US’s schizophrenic recovery: Banks’ earnings on the rise as the government bails out families

Talks of a “K-shaped” recovery after the pandemic crisis started in 2020, predicting that some sectors of the economy will benefit disproportionately by the pandemic, while everyone else bears the costs for it. Big banks and the world of finance are surely to be on the benefiting end. However, policy-makers, shareholders and executives seem to be missing a key lesson of the Great Recession -the risk of an enriching bank system that loses touch of reality may aggravate the schizophrenia of the post-pandemic economies.

Introduction

The pandemic has struck virtually every country in the world with progressively growing morbidity in the second half of 2020. Governments’ response to the spreading virus was decisive — where there ed one, to begin with. Those measures have inflicted immense pain on the economy both in developed and developing countries. However, these negative effects’ unequal distribution amongst economic sectors has been manifest since the very beginning of the contagion-lockdown-recession cycle.

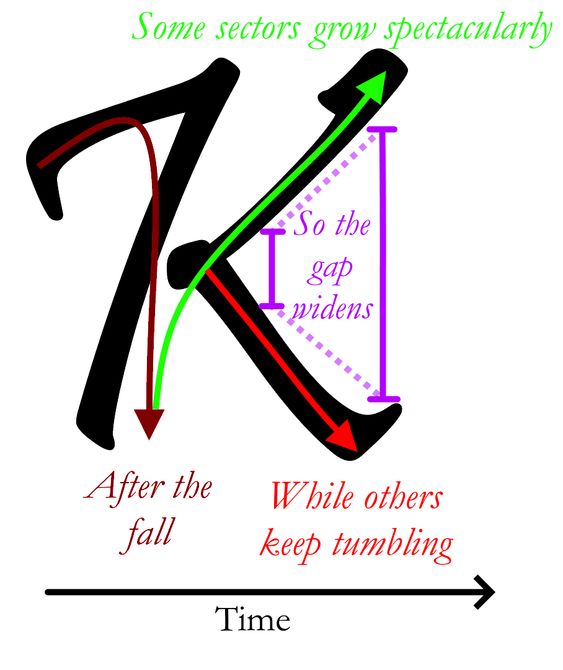

Economists coined the term “K-shaped recovery” to describe how the gap between those who fared well during the pandemic and everyone else is widening. The idea is simple: after a collapse of the entire productive system only certain markets will recover. Unsurprisingly, banks are front and centre of this perverse mechanism as it is the case in for US economy at least since the third quarter of 2020 (2020Q3).

Figure 1: The economy of K-shaped recoveries

© F.A. Telarico via Pinterest

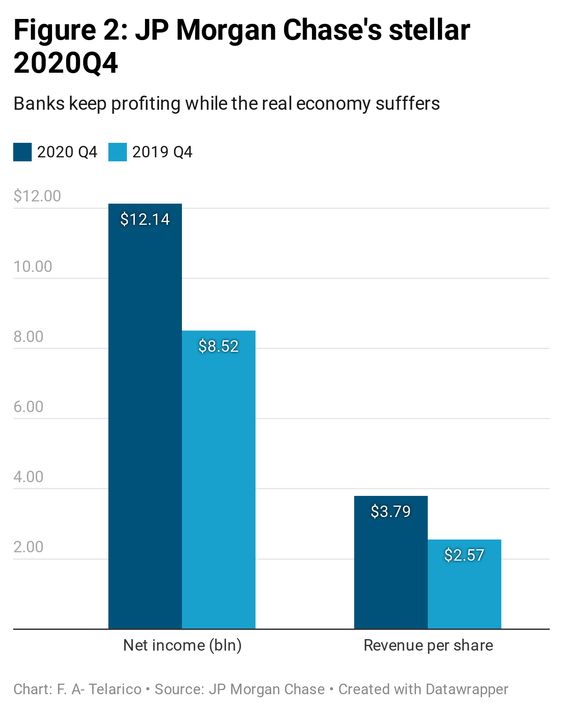

A case study in the booming banking sector: JP Morgan Chase’s 2020Q4 earnings

Against this backdrop – and bearing in mind the idea of K-shaped recovery – US bank’s latest reports appear at least worrying. One example pulled from the quartet of the most recent fourth-quarter earning reports for big banks is self-explanatory. On January 15, J.P. Morgan reported an astonishing 2020Q4 net over $12 billion. By reducing its precautionary reserve by almost $3 billion, the banks boosted revenues, earnings per share and net-interest income over the expectations.

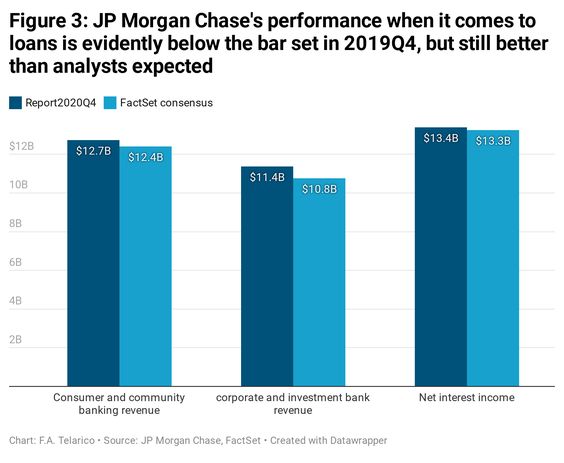

The reduction of cautionary reserves may seem to suggest that loans are getting ‘safer’, with the banks expecting less defaults. However, retail activity (i.e., consumer and community banking) was possibly the area in which JP Morgan fared worse (Figure 3). Even though analysts were expecting an even worse performance, revenue fell 8.3% year on year. Obviously, the bank’s net interest income suffered heavily due to lower interest rates on loans. These revenues fell 7% on their 2019Q4 level, but topped the FactSet consensus of $13.26 billion.

Investors reacted positively to these data, making JP Morgan one of the best-performing banking stocks in the US market. According to expert estimates, the stock rose by almost 39% during 2020Q4, against the 26% of selected financial-sector stocks and the meagre 9% of the Dow Jones.

The schizophrenia behind the data

True to the facts, US and EU banks are both quite solid, as recent stress tests have shown. could be at a point where there’s less worry of loan defaults. But a question looms over talks of prosperity, as Aperture Investors CEO Peter Kraus stated:

“We expected trading income to be pretty robust and it turned out to be the case. That’s not surprising. […] They’re probably a little bit better than what people expected. But then the question is: is that trading revenue really sustainable? And you’re going to see that going into the future and that’s [where] consumer income is actually more predictive of what we might actually see in the next three months to six months.”

The reasons why these positive bank results cannot be sustainable in the long run are evident: big banks’ profits are doing better than the economy. The greatest danger lies precisely in the falling profitability of retail loans — a key factor in fuelling economic growth. In effect, the promise of a ‘better 2021’ has injected enthusiasm in investors’ veins — opening their purses. Currently, “the industry is slowly emerging from a worst-case scenario of low-interest rates, a struggling economy, and […] loan defaults.” But the demand for loans is plummeting, and negative expectations on the real economy are here to stay.

A scenario for growing inequalities and economic imbalances

Lockdown-induced crises around the world have extolled a much higher price on the poorest, adding insult to injury. Arguably, the reasons for that lays at least partly on a combination of factors encompassing policy responses and longstanding trends. The Great Recession became a global crisis and brought banks on their knees due to the so-called credit-crunch effect. Thus, banks felt lending money to partners (i.e., other banks) and clients with unclear collaterals was too risky. Consequently, the flux of debt that nourishes capitalism was cut off. On the opposite, this time around central banks – and the Federal Reserve in particular – lavished the markets in liquidity. This choice allowed the financial sector – and, particularly, so-called universal banks – to fare better this time around.

Figure 4: Jerome Powell, the Trump-appointed chair of the FED, has promised to keep interest rates low through quantitative easing. The Fed is creating the perfect conditions for the stock market to thrive while the economy recedes.

© Drew Angerer for Time

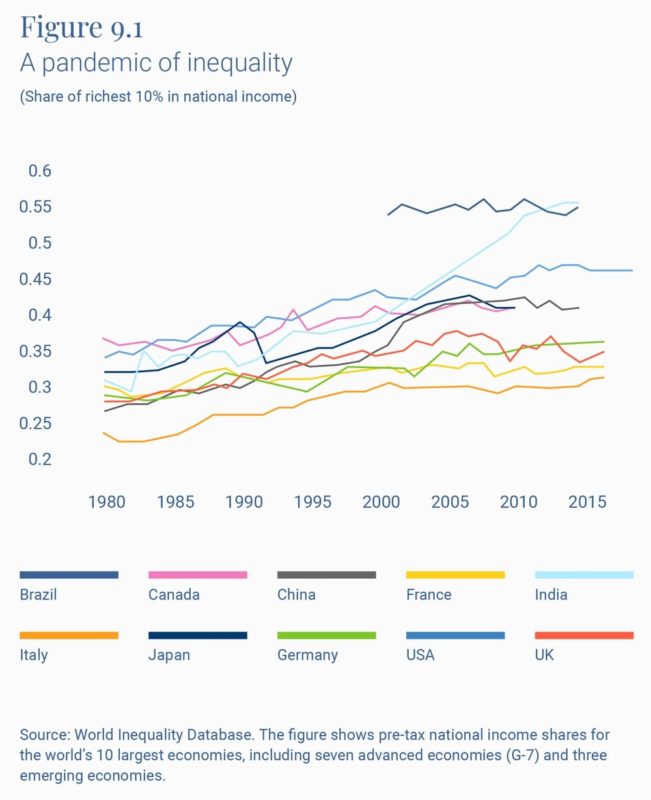

The reason why the real economy will keep struggling under current policies is in the marginal propension to save. Put simply, this is the indicator of how much people would save per any dollar of extra income. Clearly, poorer households cannot afford to save as much as richer ones. An increase in income will mostly – or exclusively – be devoted to the need to increase consumption of goods and services. The contrary applies to wealthier people, who are already buying all they desire to consume. Since easing monetary policy favoured investors by rocket-starting the stock market, the wealthier benefited disproportionately. Consequently, inequalities are rising around the globe (see Figure 5).

Figure 5: Share of the richest 10% in national incomes.

© Brookings Institution

In conclusion, preemptively saving the banking market can be a counter-productive bet, especially if such a policy is pursued for the sake of doing it. The large body of scientific literature explaining why the wealthiest benefit the most from it should not be discarded. Investors may want to bet against this schizophrenia. After all, sooner or later, stock markets will have to fall in line – or, better, down – with the real economy.