Recent declines in the dollar have once again raised questions about its status as the de facto global reserve currency. But the current depreciation in the greenback is more the result of a perfect short-term storm, as opposed to a permanent international retreat from the dollar.

During times of crisis, the greenback usually appreciates. This is because investors flock towards safe, liquid assets – such as US treasuries – that is backed by a strong institutional framework, namely a Central Bank. Unlike the Eurozone members, the US cannot default on its debt, unless it willingly chooses to. Unsurprisingly, the coronavirus pandemic has been no different, at least in the initial stages. But several recent developments have forced a decline, leading some to believe that its status as a safe-haven, de facto global reserve currency is eroding. Is it?

What explains the decline in the dollar?

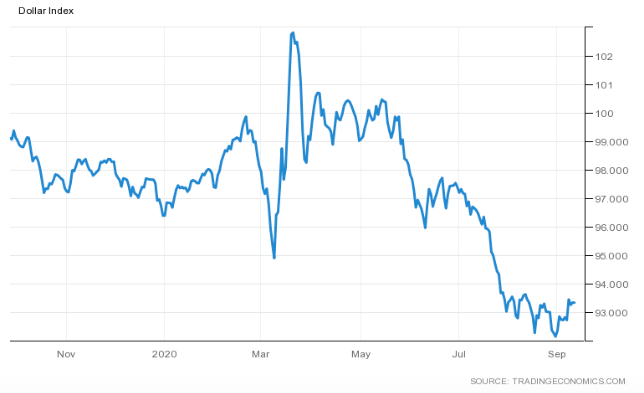

Since its peak in March, the dollar index has fallen more than 10 percent, though it has slightly recovered recently. There are several reasons for this.

The failure of the US government to effectively contain the coronavirus, broader social unrest, an uneasy political climate and growing public debt concerns have dampened long-term confidence in the dollar. Moreover, additional rate cuts have eroded the differentials between the U.S. economy and other developed economies. A perfect storm of sorts.

But, perhaps, most importantly, the main concern has been the Federal Reserve’s recent decision to allow inflation to run above 2 percent, in an attempt to meet a 2 per cent average inflation rate. The goal is to accelerate growth and bring down unemployment.

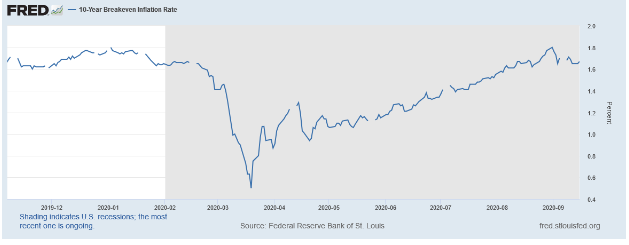

Allowing inflation to take off will inevitably undermine the dollar as a store of value, albeit in the short-term. The break-even rate, which measures the spread between the yield of a nominal bond and an inflation-linked bond of the same maturity, for the 10-year US treasuries, has been widening, which points to growing inflation expectations. But it has stalled in recent days, suggesting that investors are sceptical of the Fed’s ability to raise inflation. After all, globalisation, demographic shifts and technological developments have limited the ability of Central Banks to reach their inflation targets.

But if inflation takes off, Wall Street economists do not expect the type of runaway inflation witnessed in the 1970s. However, with interest rates at such depressed levels, even a modest rise in prices has the potential to wipe out a significant portion of bond yields – leaving both equity markets and long-term bond investors increasingly exposed.

Is the dollar losing its de facto global reserve currency status?

Restructuring the financial system cannot happen overnight. Nor are there viable replacements. The Euro and the Renminbi, to a lesser extent, are obvious contenders. But neither offer the deep liquidity dollar markets offer.

Dollars still account for just over 60 percent of allocated global foreign exchange reserves – down from around 66 percent in 2015. Euros, which come in second place, account for 20 percent – 8 percent less than in 2009. The Chinese renminbi, 2 percent.

The Eurozone agreed on a 750bn euro recovery fund, which could boost the euro’s share of global foreign exchange reserves. Peripheral markets, such as Greece, offer positive returns at a time when most high-rated debt is trading at sub-zero yields. But, as a whole, the Eurozone’s longer-term prospects remain grim, which reduces the attractiveness of euro-denominated assets in the future. Much like the US, it has productivity concerns, rising public debt levels and extremely low-interest rates.

Even before the pandemic, Germany was flirting with a recession. Italy still faces significant structural issues. Others aren’t doing better either. The OECD forecasts that unemployment in Spain will reach 22 percent by the end of 2020. Non-performing loans still account for 43.6 per cent of total loans in Greece. Unlike in the US, Eurozone economies can face insolvency risks.

The bloc is also more structurally prone to political paralysis. The current US political climate, while tense, is simply the result of the election season – which will pass. Moreover, the financial infrastructure of the Eurozone currency bloc is vulnerable to bank runs. Until the banking and capital markets unions are complete, it cannot protect itself against economic shocks.

As for the renminbi, it will likely grow in stature as the BRI countries deepen their financial and economic integration. But as long as it employs tight capital controls, it cannot replace the dollar. Moreover, geopolitical considerations limit China’s ability to push itself to the forefront of global currency arrangements.

As such, little is likely to change in the short-to-medium term, provided the US doesn’t undergo a monetary implosion. Despite the recent decline, the Federal Reserve extended swap lines to several countries in March in an attempt to boost dollar funding markets, once again demonstrating its pivotal role in global financial processes. Countries still need dollars to finance current-account deficits and repay external borrowing. Some $12tn global liabilities are denominated in the US dollar. In terms of trade, around 23 percent of global exports are invoiced in the currency. Commodity markets are almost completely dollarized.

Moreover, the euro has an interest in curbing a prolonged appreciation in its currency, particularly against the dollar. A stronger currency undermines exports, a reality that should eventually force the dollar up against the euro. Deflation in the Eurozone will also force policymakers to consider shifting the current exchange rate.

Concluding remarks & forecast

The dollar’s value has generally declined in recent months. But it is still relatively strong, having appreciated 17 percent against the Euro between 2010 and 2020. Instead, the decline appears to be the result of a truly perfect short-term storm. As such, expect it to continue its slide intermittently in the immediate future, particularly as the presidential race intensifies and emotions across both the political and social spectrum peak. Inflation, while not guaranteed, will also place some downward pressure. But these are, most likely, temporary developments. Moreover, America will benefit from its flexible labour market, which will likely lead to a faster recovery and a rebound in productivity – raising demand for dollar-denominated assets. This is what happened after the financial crisis.

As such, permanent dollar displacement is highly unlikely. Sluggish growth prospects and an uneven recovery in the Eurozone will undermine demand for euro-denominated assets outside of German and EU bonds. The head of Germany’s central bank, Jens Weidmann, wants to scale back fiscal and monetary support soon, suggesting that high debt ratios must be tackled right after the crisis. If the ECB steps back, bond yields will increase, which may trigger a sell-off, driving interest rates even higher. Without artificial support, countries hit hard by the coronavirus will be at the mercy of private capital markets. As such, they will have to convince investors of the quality of their bonds. The only way to do so is through reform and re-adjustment. But this takes time and will.

China, meanwhile, may see growing interest in using the Renminbi as a means of payment within the BRI. But until it loosens its capital account, it also cannot intensify its internationalization process. But China faces geopolitical obstacles, as its authoritarian tendencies do not inspire confidence.

If anything, it is geopolitical forces, such as the persistent use of the dollar as a foreign policy tool, that undercut the dollar’s global position. If dollar weaponization continues, the rest of the world will have an interest in establishing alternative pricing arrangements for products such as oil. The Euro is an option.

Regardless, economic forces continue to reserve an important role for the greenback during crises, as was noticeable in March. Dollar liquidity remains essential to global financial stability, not to mention international trade. But it would also be naive to assume that current arrangements are eternal. The point is, the dollar’s main threat, at this point in time, is its issuer. Nobody else. The recent declines are temporary events, and global confidence in the dollar has not disappeared just yet.