Latin America is undergoing powerful political changes. These new developments will have significant repercussions on risk, posing challenges to political and economic stability in the region. 2018 will be a crucial year, as Brazil, Venezuela, Colombia, and Mexico hold key elections. GRI analysts Benedetta di Matteo, Lorena Valente, Sam Schofield, and Niall Walsh weigh in on the outlook, in this long-read special report.

The seeds of change are already visible. While 2017’s regional elections resulted in the strengthening of the governments of Nicolas Maduro and Mauricio Macri, Chilean and Ecuadorian results were indicative of political fragmentation.

The countries of this vast region are of course very different, but one trend seems to be on the rise: populism. In Mexico, leftist candidate Andres Manuel Lopez Obrador is leading in the polls for the July 2018 presidential elections. Similarly, in Colombia, the left-wing politician Gustavo Petro is supported by a significant part of the Colombian electorate, which will vote for President in May 2018. Recent polls also show right-wing presidential candidate and former military officer Jair Bolsonaro in second place in Brazil.

This trend is closely linked to discontent with mainstream political parties amongst voters in a region plagued by corruption, organized crime and economic stagnation. Results from Risk Pulse surveys, a new approach to measuring political instability by Dalia Research, showed that 56 percent of Colombians, 72 percent of Brazilians, 59 percent of Mexicans and 77 percent of Venezuelans disapproved of their respective Presidents’ performance in 2017.

Similar findings apply to the perceived performance of national parliaments, ruling political parties and national police forces, as popular approval remained rather low through 2017. The same respondents claimed that corruption in their countries has significantly increased in the past year, with as much as 63 percent of Brazilians, 61 percent of Mexicans and 79 percent of Venezuelans agreeing with the statement. Furthermore, the widespread financial inequalities in the region are a major concern, as the vast majority of the respondents expressed to feel angry about inequality in Brazil, Venezuela and Mexico.

Executive Summary

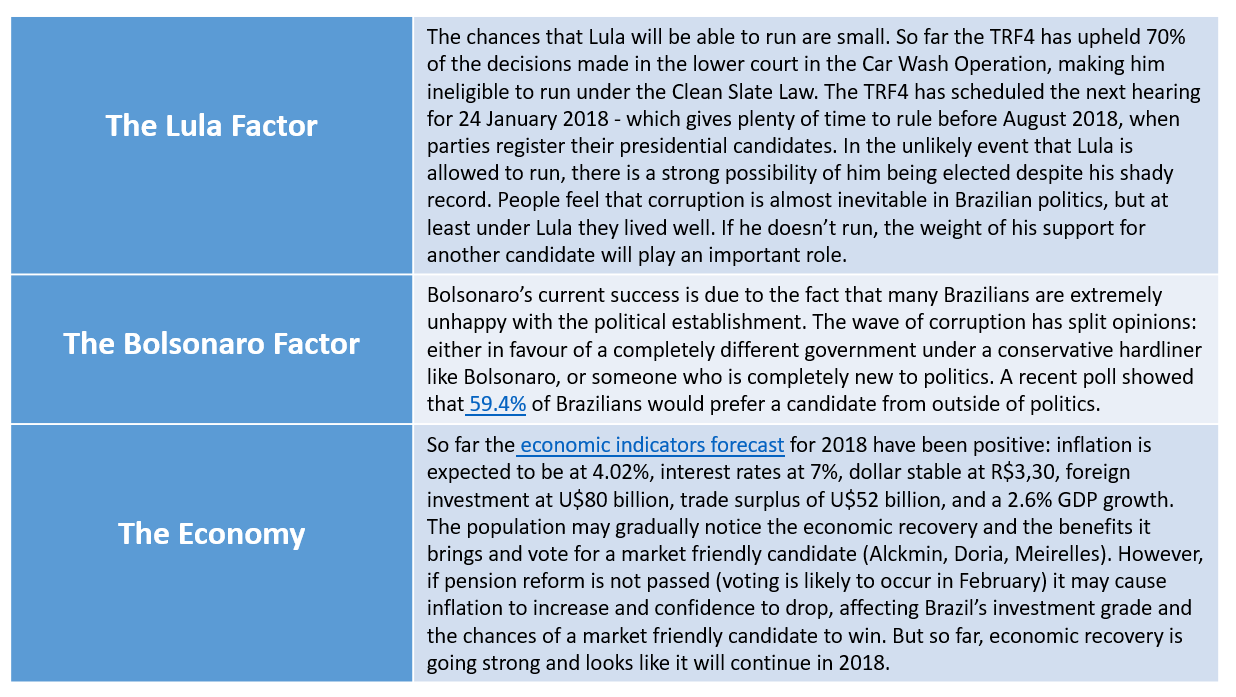

- BRAZIL: It is still uncertain whether the Clean Slate Law will prevent popular former president Lula, under investigation for corruption, from running. If he does not, Brazilians might opt for Jair Bolsonaro, seen by many as an alternative to the political establishment. Scenarios with Lula and Bolsonaro would lead to market uncertainty, likely slowing investment, growth, and job creation.

- VENEZUELA: President Nicolas Maduro is highly likely to stay in power after 2018. The lack of unity in the opposition and high voter abstention rates will strengthen Maduro’s position. High levels of inflation, foreign debt and sanction-led financial restrictions will keep investor confidence towards Venezuela low.

- COLOMBIA: Current pro-business economic policies are likely to prevail. A coalition government is very likely, given that no candidate is currently expected to win a majority of votes due to the fragmented candidacy landscape.

- MEXICO: A victory for Lopez Obrador would cause the highest degree of uncertainty. His reservations about privatization and free trade agreements such as NAFTA would result in Mexico adopting a more isolationist economic stance. Nevertheless, the rise of current Finance Minister Jose Antonio Meade in the polls suggests Mexico might just choose a candidate who will follow a mainstream economic approach.

- THE REGION: Some of the newly elected governments could have a strongly divisive effect on neoliberal regional initiatives such the Lima Group and the Pacific Alliance. Regional support for President Maduro may also increase due to ideological affinities with some of the candidates.

BRAZIL

In 2017, Brazil experienced a political roller-coaster with two corruption accusations against its current President Michel Temer, a massive corruption scandal that continues to engulf high level political figures, and a divided Congress that has shown little support for the President’s economic reform package. However, the country has shown signs of economic recovery with low inflation and interest rates, a stable dollar and stock exchange, an increase in consumption, and a forecast expecting GDP growth.

The context

Brazil’s presidential elections are set to take place on 7 October 2018 with a potential run-off scheduled for October 28, 2018. The latest Datafolha poll in early December shows leftist former President, Luiz Inacio ‘Lula’ da Silva, leading the polls with 36%. In second place is right wing Congressman, Jair Bolsonaro, with 18% followed by center-left former Minister of Environment, Marina Silva, with 10%. In a second scenario without Lula, since he may not be allowed to run under the Clean Slate Law, Bolsonaro leads with 21%, followed by Marina Silva with 16%. In a potential Bolsonaro/Silva runoff, Silva shows as the winner.

There are also three market-friendly candidates worth mentioning who have not polled well so far: Geraldo Alckmin (Governor of Sao Paulo), Joao Doria (Mayor of Sao Paulo), and Henrique Meirelles (Minister of Finance).

Even though the polls show a preference for Lula or Bolsonaro, it is still too early to tell who will win the presidential election given that many candidates have yet to announce their candidacy and full campaigning has not started. Campaign time for TV and radio is determined by number of party members (and coalition members) in the current legislature. As of right now, a candidate supported by the Brazilian Democratic Movement (PMDB – center right) – Michel Temer’s party – would receive 39% of campaign time, followed by 13% of Workers Party (PT – left), and 10% of Brazilian Social Democracy Party (PSDB – center right). In four of the last seven elections the candidate with most TV time won.

The race

Lula is a member of the Worker’s Party (PT – left) and a former President of Brazil who lifted many people out of poverty through social programs and uncontrolled public spending. On 12 July 2017, he was sentenced to nearly 10 years in prison for passive corruption and money laundering and as a result it is still uncertain if he will be able to run due to his legal restrictions. Lula has a history of increasing the role of the state and it was under his term that Brazil lost its investment grade due to fiscal imbalance.

On the other hand, Bolsonaro, who recently affiliated to the Social Liberal (PSL – right), is known is known for his hardline views on guns, God, public security, law and order, and his admiration of the former military dictatorship (1964-1985). Recently, Bolsonaro has softened his economic nationalist rhetoric to favor less state intervention and an independent central bank.

3 factors to watch in the leadup to the election

The presidential election is expected to influence the renewal of congress. All 513 Chamber of Deputies Congressmen and 54 out of 81 senators are also up for re-election in 2018. Historically, the parliamentary renewal rate (percentage of congressmen who are new vs held a position prior to the current legislature) is around 40%; however, given the car wash scandal, 60% of Brazilians say congress’ performance has been unsatisfactory, which may increase the renewal rate for 2018. The future president will strongly depend on congress to pass necessary reforms, especially if pension reform is not approved prior to the election.

The risk outlook

A Lula or Bolsonaro victory would bring market uncertainty, slowing investment, growth, and job creation at a critical time of economic recovery. However, they understand that the success of their presidency will be highly correlated with economic performance, so while there is some downside economic risk it will likely not be as unpredictable as in the past.

If Lula is elected, 96% of investors polled by XP Investments believe the stock market will decline and 98% believe the currency will devalue. Even Bolsonaro is currently polling at decent levels with the market, proving that from a business perspective at this point anyone is better than Lula. On the other hand, if one of the more centrist candidates like Alckmin, Doria, or Meirelles is elected, we should expect a stable dollar and the stock market to rise, inflation targeting, continuing austerity measures to balance accounts, transparency and predictability, and market friendly economic policies such as privatizations and concessions.

Potential good news for pro-market candidates is that according to the latest Dalia survey results, political stability in Brazil is increasing – from July to December 2017 there was a 8 percentage points increase – showing that even though the country is still recovering politically and economically, the population’s perception is that things are settling down. This can result in a stronger preference for a market-friendly candidate as consumer demand continues to grow in the first semester of 2018.

VENEZUELA

The context

Venezuela’s Socialist Party candidates are expected to win the mayoral elections taking place on 10 December across the country. Similarly, Nicolas Maduro’s victory in the October 2017 regional elections has strengthened his leadership position, drastically reducing the opposition’s hope for a victory in the 2018 presidential elections. These triumphs were met with harsh criticisms from the opposition coalition (MUD), which reacted to its unexpected defeat by denouncing the Socialist party of electoral irregularities. Whether or not fraudulent, however, this victory suggests that there is a strong possibility that the PSUV will remain in power after the 2018 presidential elections, with Maduro to stand as candidate.

The race

The President’s willingness to seek reelection is in fact the only certainty to date, with most of the Venezuelan political landscape suffering from a serious lack of cohesion. The ruling PSUV is facing severe criticism from party members and the wider Venezuelan population. The high voter abstention rate in October’s elections is proof of the inability of the ruling party to secure a stable level of public support.

Electoral dissatisfaction with the current political class is overwhelmingly clear, severely undermining Maduro’s legitimacy. According to Dalia Research, as many as 62 percent of Venezuelan survey participants strongly disapprove of the way Maduro is performing his job, while 60 percent feel similarly about the ruling party’s performance. Approval ratings for Maduro and the ruling party remained very low throughout the year, at 9 and 11 percent respectively in the month of December. Furthermore, 82 percent agreed that corruption significantly increased in Venezuela over 2017, with the overwhelming majority of respondents not trusting the courts and police forces to provide justice.

On the other hand, the opposition’s defeat in October’s elections points to its structural weaknesses, which undermine the credibility of its candidates in view of next year. Polling results from Dalia also show that over the course of 2017, the Venezuelan public decreased its support for the opposition, with a lower percent of respondents believing that the political situation in the country would improve were the opposition in power. Moreover, while 53 percent of the respondents claimed they would have voted for opposition candidate Leopoldo Lopez in July 2017, only 27 percent held the same view in December. Instead, 57 percent of participants selected the options “I would not vote”, “Other” and “I don’t know” – which suggests significant voter apathy. The Venezuelan public also showed decreased support for protests, which declined from 74 percent in July to 50 percent in December.

The risk outlook

While likely to stay in power through 2018, Maduro’s administration will face enormous obstacles, casting doubts on its long-term durability. Firstly, the country’s economy is still in a critical state, with hyperinflation and high levels of foreign debts fueling the current crisis.

Furthermore, sanctions against the regime by US and European governments effectively prevent certain investors from conducting business in Venezuela. An estimated 3 billion USD were blocked in the international financial system as a result of sanctions targeting the Venezuelan government and state-owned oil company PDVSA. Such restrictions are unlikely to be lifted, as Maduro’s consolidation of power will result in worsened relations with Western governments.

A couple of recent initiatives have the potential to bring about positive change. The launch of el Petro, a new digital currency backed by the country’s oil and gold reserves, could alleviate businesses from the burden created by hyperinflation and economic sanctions, allowing for banks and investors to carry out financial transactions independently. However, el Petro still needs to be recognized by other countries and its value is currently unknown.

Secondly, the ruling Socialist party and the opposition are continuing to engage with a view to resolving Venezuela’s economic and political crisis. They last met on 15 December in the Dominican Republic. While the parties involved failed to reach such an agreement during past meetings, the worsening state of the country’s economy may pressure them to finally come to terms.

COLOMBIA

The context

In May 2018, Colombians will elect a new president. This election comes at a time when the country appears poised for further growth and prosperity, but its long-term prospects hinge on critical decisions around fiscal management and implementation of a controversial peace agreement with the Revolutionary Armed Forces of Colombia (FARC) paramilitary group.

Current President, Juan Manuel Santos, a center-right leader, has largely stewarded a healthy economy. However, despite winning the Nobel Peace Prize for reaching an agreement with the FARC, the controversial terms of the peace deal have left him unpopular and created a mood for change.

Additionally, a growing middle class has meant that more people have a direct stake in the opportunities and risks that come with certain fiscal, social, and security policies. As a result, more voters have expressed an eagerness to tackle corruption and other issues that they feel put a brake on the country’s – and their own – prosperity.

The FARC peace plan calls for ambitious and expensive workforce reintegration and rural development programs for former FARC soldiers. However, Colombia currently runs a fiscal deficit, largely due to a decline in global commodity prices. Furthermore, Fitch has signaled a possible credit downgrade if GDP growth and revenues do not improve. Any leader will need to reach a balance between satisfying an impatient populace with short-term demands, and maintaining the long-term competitiveness of country via fiscal austerity.

The race

The race has recently narrowed. Current Vice President, German Vargas Lleras, has emerged as a strong candidate. On 24 November, two former Conservative presidents – Alvaro Uribe (2002-2010) and Andres Pastrana – stated they will join forces to back candidates for the presidency and vice-presidency. Ivan Duque, of the Centro Democratico party, is widely seen as Uribe’s chosen candidate. Progressive frontrunners include former peace negotiator Humberto de la Calle, and ex-governor Sergio Fajardo.

A victory by Lleras or the Uribe-Pastrana-backed candidate would result in similar economic policies. Where these groups diverge is the FARC peace plan. Uribe has been a vocal opponent of the peace agreement and lobbied aggressively to kill the deal. Although the right wing parties now view the peace agreement as law, they threaten to tweak components of the deal.

Lleras is committed to the peace deal, but will face pressure from the left to make progress more quickly, and potentially aggressive efforts from the right to prosecute more ex-guerillas and to marginalize the FARC as a political party. His popularity stems from his plans to cut taxes for corporations, dividends and other profits for foreign boldhonders, aimed at boosting FDI. However, these cuts could also limit the ability of the government to plug the deficit and stay within fiscal targets domestically.

Even with Colombia’s impressive growth in recent decades, its credit rating remains only two notches above junk. If tax cuts worsen or sustain the current budget deficit and Colombia’s credit rating drops it would severely narrow the types of investors willing to buy Colombian securities. Any new leader is unlikely to want to bear the brunt of this outcome.

Should one of the progressive candidates prevail, they will commit to implementation of the peace agreement, which will bode well for security. However, a leftist administration may not implement the necessary fiscal reforms, meaning in the longer-term, Colombia could fail to sustain rural economic development, ultimately threatening FARC’s faith in the government and willingness to compromise.

The risk outlook

The highly competitive race could mean no candidate wins a plurality of votes and enters the presidency without a strong mandate. They will then need to form a governing coalition, which will be challenging, especially with the FARC now being a political party with seats in Congress. President Santos’ Social Party of National Unity built a strong moderate coalition in Congress during the early part of his presidency, but that coalition has frayed, meaning even Lleras, as Santos’ center-right successor, would have a lot of work to do.

Elections in other major economies could result in shifts that change the current regional landscape. A leftist victory by Andres Manuel Obrador (AMLO) in Mexico could very possibly result in Mexico pulling out of the successful Pacific Alliance (PA), the trade bloc composed of Chile, Colombia, Peru and Mexico. The PA focuses on increasing its collective trade bargaining power with the Asia-Pacific and other regions and its success has attracted interest from other major Latin American economies such as Costa Rica and Panama. Any shift to the leftist and protectionist policies in Mexico or Colombia, whether self-initiated or in response to a break up of NAFTA, could drastically affect Colombia’s favorable trade terms with its neighbors, and favorable export terms to Pacific markets as an alternative to the US. This in turn could weaken GDP growth and the Colombian peso and risk the country’s ability to deal with its deficit and development goals.

MEXICO

The context

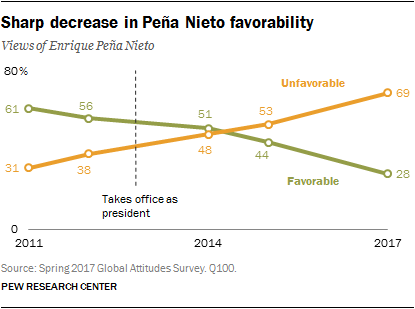

Mexico is another regional economic power facing the wrath of populism and political uncertainty in the year ahead. Enrique Pena Nieto, the Mexican President, is experiencing his lowest approval ratings since coming to power in 2011. With about six months to go until the presidential election, support for Nieto stands at 28%, less than half of the support he enjoyed in 2011.

This trend reflects the disenchantment of many Mexicans with the Nieto administration and the country’s political establishment. On the eve of his election in 2011, Nieto highlighted security as a key priority and vowed to reduce crime and violence throughout the country. However, six years later, high crime rates and systematic corruption have profoundly compromised the government’s legitimacy.

As it stands, 2017 was Mexico’s most violent year in over two decades. According to the interior ministry, 20,878 murder investigations were opened. Murder rates are now higher than when Nieto took office six years ago, exposing his failure to make Mexico a safer country.

High crime rates, predominantly attributed to criminal gangs and the illicit drug trade, are not the only factors undermining the current administration. Corruption has decimated trust in the government. In the last three years, corruption investigations have been directed against ten of Mexico’s state governors. Eight are affiliated with the ruling party, the Partido Revolucionario Institucional (PRI). The accusations of official corruption in Mexico include contracts, money laundering, and collusion.

The race

The patent unpopularity of the Nieto administration has facilitated the rise in populism across Mexico, in the form of Lopez Obrador and his Morena party. Lopez Obrador, also known as AMLO, represents the main opposition to the PRI for next year’s election and his campaign rhetoric resonates with many ordinary Mexicans.

Like populists across the globe, AMLO stands for everything that is at odds with the political establishment and promises to prioritise lives of ordinary Mexicans who have suffered as a result of globalist economics. Lopez Obrador understands the disengagement of many Mexicans with the political system and has positioned popular disenchantment centrally in his campaign. The political veteran has labelled the political establishment in Mexico City as ‘the corrupt mafia’.

Echoing the populist rhetoric north of the Rio Grande, AMLO has vowed to ‘drain the swamp’ and obliterate ‘corruption in government from top to bottom’. There is growing support for AMLO’s populist agenda: in a recent poll by El Universal, he is the front-runner to become president, receiving between 28.6% and 31% support.

AMLO’s main challenger in the presidential race appears to be Jose Antonio Meade, the current Finance Minister. By law, Nieto is not allowed run for a consecutive term. Although Meade has yet to be nominated as the official candidate for the PRI, he is expected to be named following his resignation as Finance Minister. He also has the support of Nieto and many within the PRI. According to a poll following his candidacy registration, he would receive the vote of 23.2% of the electorate. Significantly, Meade is not a member of the PRI, which permits ‘outsiders’ in government and allows them to run for presidency. This is likely to attract cross-party support.

Other challengers include the newly created left-right coalition ‘For Mexico in Front’. This covers the political spectrum by amalgamating the conservative National Action Party (PAN), the centre-left Party of the Democratic Revolution (PRD) and the Citizens Movement party.

The risk outlook

The election of AMLO would spark major changes. He vows to pursue an economic nationalist agenda in order to improve the lives of ordinary Mexicans. He is opposed to the neoliberal policies that have symbolised the country’s regional significance in the last twenty years and believes foreign influence in the Mexican economy is incompatible with the needs of Mexican citizens.

Considering his anti-trade and anti-privatisation stances, one of the major areas of concern will be AMLO’s opposition to NAFTA. He sees the agreement as another attempt to internationalise the Mexican economy at the expense of its people. Given his pronounced ‘Mexico First’ stance, coupled with economic nationalism in the United States, the election of AMLO could seriously threaten the future of NAFTA and change Mexico’s role in the global economy.

Investors will be hoping for a victory for Meade. Meade, an economist with a doctorate from Yale, has held successful cabinet positions in different administrations and is regarded as somebody clean of the corruption that has engulfed the PRI. If elected, his economic policies are likely to follow a mainstream approach that views the international economy as vital to Mexico’s social and economic development.

As it stands, Mexicans are facing the choice between someone who favours political and economic continuity, and a candidate who vows to break down the current order. Since 1929, the PRI has dominated the Mexican political arena. Considering the lack of support for Mexico’s political establishment, a vote for Lopez Obrador represents an opportunity to vote against the country’s political class. Thus, what AMLO stands against could be a major factor in the outcome of the election.

This report was prepared with inputs from Risk Pulse, as part of a new collaboration with Dalia Research that draws on cutting-edge public opinion data collected monthly by Dalia with the specific aim of forecasting political risk.