In an unusual move, President Trump did not reappoint Janet Yellen as chair of the Federal Reserve, instead nominating Jerome Powell as the new chairman. Although Powell is widely expected to continue the course Yellen set for the Fed, he won’t merely be a prolongation of the past four years. Pressure to ease regulation, as well as the continued objective to normalise interest rates and the Fed’s balance sheet will present Powell with numerous challenges during his tenure.

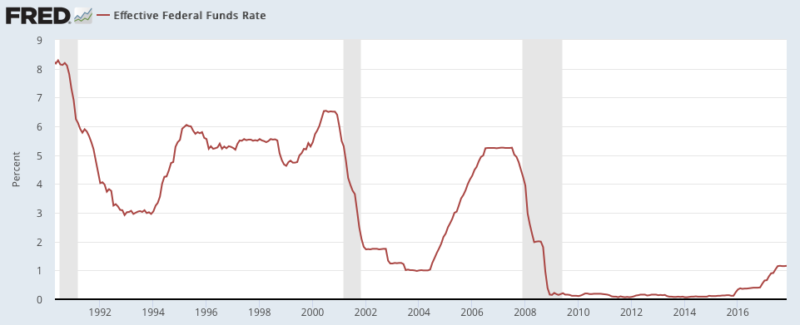

Ten years after the 2007 subprime mortgage crisis, the U.S. economy has undergone a substantial recovery. In November, the unemployment rate sat comfortably at 4.1% and real GDP had a growth rate of 3.1%. When Janet Yellen took over the chair in 2014, interest rates hovered above zero at 0.07%. Today she leaves her chairmanship with interest rates at 1.25-1.50%.

Regarded as a continuation of chair Janet Yellen, Trump appointee Jerome Powell is not expected to diverge from the Fed’s current course. Under Yellen’s leadership, Powell supported all of the Federal Reserve’s interest rate hikes as well as the normalization of the Fed’s policies and balance sheet for a post-recession economy.

Business as usual?

Powell is anticipated to continue gradually raising interest rates. Following its December meeting, the Federal Open Market Committee (FOMC) announced that three more rate hikes should be expected in 2018, followed by two in 2019. During his confirmation hearing before the Committee on Banking, Housing, and Urban Affairs, on November 28, Powell reiterated much of the same sentiment– saying that he and his colleagues “expect interest rates to rise somewhat further.” Markets reacted positively to the announcement, as raising interest rates will have a positive effect on financial markets; however, consumers will face higher borrowing costs with further rate hikes.

Source: https://fred.stlouisfed.org

However, the Republican’s tax reform might force a change in Powell’s vision of slow and steady rate hikes. The tax bill comes with a $1.5 billion tax cut, first expected to provide a substantial boost to the economy, which is already close to full employment, then is expected to cause the debt to significantly increase. While Yellen welcomed such an economic boost, she voiced concerns over even greater debt during her testimony on “The Current Economic Outlook and Monetary Policy” on 29 November.

Meanwhile, low inflation rates continue to be a conundrum. Currently at 1.6%, inflation continues to miss the Fed’s target of 2%. Although the Fed still expects rates to meet their target in 2020, as core inflation should reach 1.9% in 2018, Yellen also acknowledged that, given low inflation rates among developed economies in general, “something more structural may be going on”. She suggested that global technological developments may be keeping inflation down, and that confidence in the U.S. labor markets might have been exaggerated.

Besides low-interest rates, the recession left the Fed with a huge balance sheet. In an effort to counter the crisis, the Fed hoovered up treasuries and mortgage-backed-securities, growing the balance sheet from $750 billion in 2007 to $4.5 trillion in 2014. To trim its ledger, the Fed announced that it would stop reinvesting all of the money it receives when its assets start to mature. While this could mean a boost for long and short-term yields, it also ultimately means a tighter money supply. If done too quickly, consumers and businesses could turn to very short-term debt to offset a lack of credit availability, increasing the risk financial market instability. Therefore balance sheet “normalisation” will have to be ushered in gradually.

The Fed’s continued transparency towards the planned balance sheet normalization has been crucial for its success. Powell plans to maintain this openness, stating that he is “strongly committed to [the] framework of transparency and accountability”. During his confirmation hearing, Powell explained that although the size of the balance sheet will be smaller than the current one, it will however also be bigger than it was pre-crisis, and is expected to range between USD 2.5 trillion and USD 3 trillion. Should the balance sheet normalisation prove unsuccessful, the economy will be facing significant inflationary consequences.

Facing the prospect of deregulation

In addition to normalising its balance sheet, the Fed will also begin to review post-crisis financial regulations. Regulations set in place in 2010, namely the Dodd-Frank Wall Street Reform and Consumer Protection Act, included higher capital and liquidity requirements, stress tests, and living wills. Proponents for increased deregulation urge that regulation ought to be more specific in its scope, and highlight the positive impact decreased regulations will have on the economy.

Deregulation was a prominent issue during the 2016 Presidential Campaign and continues to be debated in Congress. A bi-partisan bill put forward by the Senate Banking Committee, led by Mike Crapo (R-Idaho), “The Economic Growth, Regulatory Relief, and Consumer Protection Act”, would make it easier for consumers to get mortgages and obtain credit, while reducing the scrutiny on financial institutions.

Among the most ardent opponents to deregulation is Senator Elisabeth Warren (D-Massachusetts) who voiced her disappointment over Powell’s statements during his confirmation hearing. Powell stated in his speech before the Committee on Banking, Housing, and Urban Affairs on 22 June that “small banking organizations could be exempt from the Volcker rule and from incentive compensation requirements of the Dodd-Frank Act”. The Volcker rule, which bans bank from propriety trading, would be perhaps the most prominent rule under consideration for modification.

Regardless of the economic benefits of deregulation, the Fed should remain cautious and should stick to lessons learned from the Great Recession. Suggested tweaks to current regulations, such as revoking the Volcker rule, would require a substantial improvement in regulatory capacity before any changes can be made.

In addition, Trump has his own agenda for the Fed, though it will remain to be seen how much influence he is able to have on its policies. He has already appointed Randal Quarles, Vice Chair for Supervision, who has announced that plans to revisit stress tests, as well as Marvin Goodfriend as member of the Board of Governors of the Federal Reserve System. He is also expected to appoint a new Vice Chair after Stanley Fisher retires, as well as a new president for the New York Fed in mid-2018. This reshuffling of the Fed may have policies chart a different course than the current one, specifically leaning towards more deregulation and interest rates hikes.

Overall, markets responded well to the appointment of Jerome Powell. Regarded as a continuation of chair Janet Yellen, Jerome Powell is expected to continue the steady path of rate increases and the implementation and oversight of balance sheet normalisation. However, with a restructured Fed dominated by Trump appointments, a shift in policy – in particular towards deregulation – is possible. Wall Street banks will further encourage deregulation on an array of stringent policy measures set in place as a result of the financial crisis, especially as soaring stock markets and regained market confidence cause complacency towards regulation. Powell may have big shoes to fill at the Fed; however, he will most likely be able to leave a mark himself.