A revolution of the European corporate financing model is underway. As banks retrench and downsize in the face of new regulation and burdened balance sheets, direct lending is emerging as a new, superior source of financing for European mid-market enterprises.

The market for corporate financing in Europe is undergoing a seismic transformation. Challenging a playing field historically dominated by banks, a growing number of funds are now lending directly to mid-sized European companies.

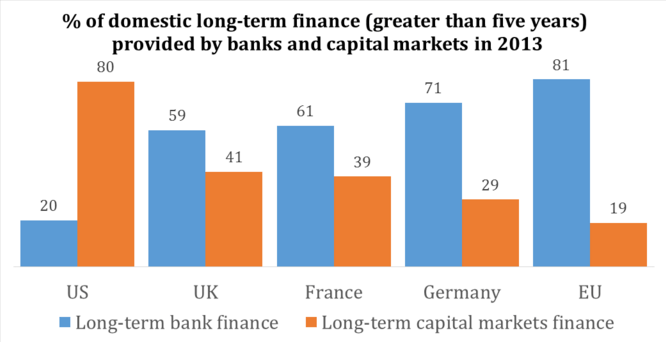

The U.S. is already familiar with this kind of insurgency. Non-bank lenders accounted for a mere 37% of American leveraged loan activity in 1998. They now make up over 85% of this market.

The European non-bank lending market is still far behind its American counterpart. Source: Intermediate Capital Group, M&G Investments

In the EU, non-bank lenders only issue around 20% of corporate loans. This, however, is quickly changing. From 2012 to 2015, the number of European managers engaged in direct lending to companies has jumped from 45 to 85. In 2014, 59% of new lending was done by institutional investors rather than banks.

KKR, the U.S.-based private equity firm, is at the forefront of this surge. It has issued over $500 million in loans to European companies in 2015.

Europe’s share of global capital raised for private debt has rapidly increased. Source: The Economist

Many other private equity funds have also begun diversifying into private debt. Of the $158 billion in deployable capital — or “dry powder — sitting in private debt funds last year, roughly one third was earmarked for European debt.

With banks in retreat and hungry investors aplenty, the rise of private debt funds is an unstoppable force. It is a quiet revolution, but a revolution nonetheless.

What is direct lending?

Direct lending refers to loans issued to corporations by non-bank institutions. These are often asset managers allocating funds raised for this specific purpose.

Targeted companies tend to be in the mid-market, or those with an EBITDA somewhere roughly in the €5-75 million range. This focus is due to the more competitive nature of large-firm lending. Behemoths can tap into the corporate bond market when seeking large loans or otherwise attract the attention of large capital intermediaries, such as investment banks, more easily than smaller firms.

Direct lending typically focuses on mid-market, sub-investment grade loans. Source: Deloitte

Direct lending often takes place under the guise of a private equity sponsor. This means the loans are either issued to finance the buyout of a firm by a private equity fund or to firms with private equity backers. Unsponsored loans, however, are becoming increasingly prevalent. Currently representing 24% of overall transactions, this share is anticipated to reach 30% over the next two years.

There is an immense pool of capital needed by unsponsored firms for expansion, refinancing, or acquisition purposes. To tap into it, private debt funds have begun setting up their own credit infrastructures, allowing them to analyze credit opportunities and perform their own due diligence. Those who undertake the necessary investments are apt to be duly rewarded: Standard & Poor’s estimates mid-market European firms will require up to €3.8 trillion in funding by 2018.

A banking sector in retreat

The global financial crisis of 2008 was the spark that is sending the old established order in flames. The new Basel III capital regulations have increased the cost for banks of issuing medium-term loans to mid-sized corporates. Intense deleveraging in the banking sector compounded this forced retreat from mid-market corporate lending.

Bank funding costs have increased since the financial crisis of 2008. Source: M&G Investments

With the gates thrown open, direct lenders are emerging to fill the vacuum. While banks traditionally have a natural advantage as lenders due to their lower cost of funds, these non-bank lenders are not a mere stopgap.

For one, the new capital regulations are here to stay. Private debt funds are not exempt because of a legal loophole. Contrary to a widespread idea, private debt managers are not shadow banks — investors are locked in, and funds are thus not subject to crises of confidence.

Deep-pocketed funds can also offer companies multiple rounds of financing and build lasting relationships with their borrowers. This is crucial if they are to replace banks as a source of capital for mid-sized family-run companies in Europe, which tend to especially value stability and predictability.

Furthermore, direct lenders are not merely substituting in for banks. Rather, they offer a differentiated product in the form of more flexible arrangements, increased speed of execution, and longer maturities. Covenant terms can be bespoke and tailored to the needs of borrowers.

An appealing asset class

The boom is in no small part driven by a surge of interest in the asset class. Investors with long-term liabilities are attracted by the important liquidity premium offered by these assets. At a time when some sovereigns are borrowing at negative rates, relatively safe direct lending investments can offer appealing returns in the high single digits. Private debt investments are also a source of diversification for fixed-income portfolios. They exhibit a low correlation with public debt and in turn provide a way of increasing risk-adjusted returns.

Similarly, private debt has proven appealing beyond its role as an alternative source of fixed income. Some investors have allocated capital in direct lending funds from private equity, alternative investment, and even hedge fund buckets.

An increasing number of large pension funds are beginning to have specific allocations for private debt. Major financial intelligence firms report that 65% of the institutional investors surveyed are intent on increasing their allocations to private debt over the long term. Those who dipped their toes in during 2015 have no cause for complaint: 90% declared the returns from their private debt portfolios to have exceeded their expectations.

Looking forward

European direct lenders have yet to be tested by the widespread defaults that will ensue when the next recession reaches Europe. The resilience of the asset-class as an attractive alternative may depend on the ability of managers to collect their dues when the cycle inverts and borrowers go into restructuring.

The boom can be expected to subside as the field becomes more crowded and yields are put under pressure. Interest in private debt in the US has waned in recent years as intense competition has driven down returns.

Nonetheless, direct lending funds are here to stay as an important source of financing for European mid-market companies. Investors should hurry while the returns are rosy; it will not be long before they are flooded by late-comers. Markets are not known for giving abnormal returns short shrift. For European companies reliant on their local bank for financing projects and acquisitions, let it be known: there is a new source of credit in town.