With negotiations failing and missed debt payments mounting, Puerto Rico’s debt crisis keeps getting worse. What lessons will be learned from how the Isle of Enchantment weathers the storm?

In the red

On Friday, January 22, the latest negotiations to restructure a large portion of Puerto Rico’s debt fell through. Failure to reach a settlement on the nearly $9 billion debt held by Puerto Rico’s state power company could lead to the largest default yet in the island’s worsening crisis.

Merely buying more time, the utility was able to reach a forbearance agreement with lenders that protects it from default related litigation until February 12, 2016. If a solution is not agreed upon by that date it may result the third default since June of 2015 when the Governor of Puerto Rico, Alejandro Garcia Padilla, announced the US territory could not pay its debts.

Puerto Rico has accumulated more debt per capita than any other US state, and, at roughly $72 billion, total debt amounts are only exceeded by the states of California and New York. Debts have piled up as more than 1.5 million Puerto Ricans have been receiving government paid health insurance since health reform legislation in 2005 and at least 25% of the island’s workforce is employed by the government itself.

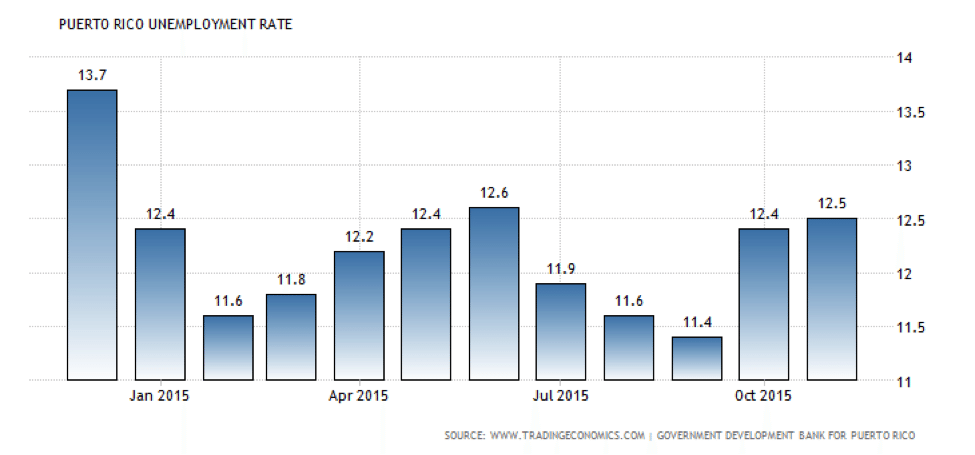

Unemployment in Puerto Rico has been in the double-digits for more than 10 years and GDP has been contracting for most of the last decade as well. Such depressed economics have been strained further as lawmakers instituted myriad new taxes to, not only fund operations, but issue and service even more debt.

To date, Puerto Rico has defaulted on $58 million in payments due in August 2015, and another $37 million that was due January 1 of this year. Deadlines continue to loom, but the best solution the island’s lawmakers can hope may be political rather than financial.

Investor exposure

The risk of further and accelerating defaults falls almost completely with in the United States. Due to Puerto Rico’s status as a US territory, it enjoys access to the nation’s municipal bond markets. As a result, risk exposure is concentrated exclusively in US mutual funds, pensions, hedge funds and banks.

Puerto Rico’s muni-bonds were especially attractive investment vehicles for these funds because they are exempt from federal, state, and local taxes. This triple exemption combined with higher than average yields make for an enticing return on capital – that is, as long as the issuer can actually honor the contract.

To put the size of the risk exposure in perspective, it is useful to compare this debt crisis with another more infamous (and repeating) crisis: Greece. In 2009, US bank exposure to the $300+ billion Greek debt was approximately $18 billion – and that has been high water mark ever since as US banks have steadily reduced exposure to the perennially disappointing sovereign.

In contrast, 100% of Puerto Rico’s approximate $72 billion in debt is held within the United States through the municipal bond market; quadrupling the direct risk to the world’s biggest economy posed by Greek default.

To be fair, the financial world was so nervous about Greece because of the extensive interdependence among Eurozone debt structures and worries of what the domino effect of contagion would mean indirectly for world markets. Indirect risks therefore represented a much more harmful result than direct exposure alone.

However, despite the differences in each debt crisis, Puerto Rico offers its own unique risk of contagion.

Precedent

Currently, Puerto Rican debt issuers (state-run utilities, etc.) are unable to declare conventional bankruptcy the way intra-state municipalities in the US have done, such as the bankruptcy filing of Stockton, California. This gives the island few options to force restructuring of the debt through the US legal system.

Since paying off the debt as contracted is mathematically impossible given current revenues, Puerto Rican authorities are increasingly looking to a political solution. Responding to calls for help from the Puerto Rican Congressional Delegation, this week the President of the United States and leaders in Congress have made finding a solution to the crisis a priority.

Treasury Secretary, Jack Lew, has called for legislation to retroactively give Puerto Rico access to federal bankruptcy regimes and congressional supports. This solution, however, does little to affect the root causes of the island’s fiscal problems and instead sets a dangerous legal precedent.

As previously mentioned, states as a whole are legally prohibited from declaring bankruptcy. Many states with unsustainable debt loads such as California, Illinois, and New York would quickly look to a Puerto Rican precedent to support their case for forced restructuring should they find themselves in a similar fiscal situation.

If lawmakers give Puerto Rico the ability to file bankruptcy, it would create a new legal framework that seemingly allows states to restructure debts without investors’ consent. This would raise borrowing costs for states overnight, as investors consider the new risks to the return of their capital.

Increasing borrowing costs would further exacerbate financial headwinds of the most indebted states that require issuing debt to keep their financial structures afloat. Should debt servicing become too expensive as a result of investors’ increasing risk aversion, large states with mounting liabilities could chance a fiscal death spiral such as that Puerto Rico is experiencing today.

Investors in mutual funds and pensions should watch political developments closely for such precedent setting legislation. Much as Greece’s relatively small economy risked dangerous knock-on effects for the rest of Europe, proposed debt solutions for Puerto Rico risk exponential contagion beyond their own shores.