While many associate digital currencies such as Bitcoin with places like Silicon Valley, in actuality the major region for cryptocurrency activity is Asia. The three largest economies in the Asia Pacific; China, Japan, and South Korea have all begun to implement their digital currency frameworks, with varying results.

China

The recent announcement by the People’s Bank of China (PBOC), that it is seeking to launch its own digital currency as soon as possible has caused international headlines. The PBOC cited lower operating costs, increased transparency and greater policy control over monetary supplies as incentives behind its efforts on the matter.

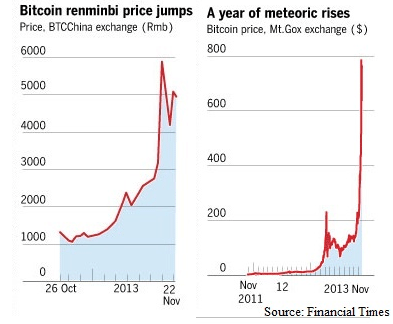

China has become the largest market for bitcoin users and miners as Chinese regulators have largely adopted a hands off approach to bitcoin businesses and exchanges. This has been surprising given China’s otherwise conservative controls on its financial markets. Indeed four of the five largest exchanges (based on trade volume) are based in China: Huobi, OkCoin, BTCC, and lakeBTC. The yuan is also the most traded currency on bitcoin exchanges, with Huobi’s 30 day yuan-bitcoin trade volume 42 times larger than the trading volume of the largest non-yuan exchange.

It is important to note that the Chinese government is not ignoring the sector, having intervened in the past when it saw fit. Specifically, the digital currency market exploded in China in late 2013, with early adopter BTC China outpacing Japan’s MT Gox and EU based Bitstamp to become the largest exchange by November 2013. During the same time both Baidu and Alibaba accepted Bitcoin as payment for subsidiary services.

By December 2013, the Chinese government intervened, restricting activity, followed by Baidu and Alibaba dropping Bitcoin payment options. Despite this initial intervention, the digital currency market has continued to grow in China, with many successful exchanges popping up. While physical goods cannot be purchased with bitcoins, many Chinese are increasingly using digital currency to diversify investments and get around capital controls.

Consequently Beijing’s efforts to push forward on the creation of its own digital currency has several motivations.

Firstly, Beijing fears the unknown, and while it is pragmatic enough to recognize and adopt a winning trend when it sees it, it will still seek to minimize its exposure to risk. The idea of allowing an entire economic sector to be based on a cryptocurrency created by unknown (an individual or group called Satoshi Nakamoto created Bitcoin in 2009) entity with unknown allegiances and/or access to back-end code, deeply concerns Beijing.

Secondly, Beijing has been badly stung by its initial efforts to liberalize financial markets, and as such is seeking to reign in potential bubble producing trends. While digital currency transactions do not pose a destabilizing threat to the Chinese economy, Beijing is seeking to implement its own digital currency to forestall the creation of a financial sub-sector outside the control of the central bank.

Lastly, given the high usages rates of digital retailers such as Taobao (C2C), Tmall (B2C), and Alibaba (B2B) in China, the implementation of a state sanctioned digital currency could further domesticate China’s internet ecosystem. In other words, China already has its own versions of Amazon, Ebay, Google etc. so promoting its own in-house digital currency becomes much easier when all the pillars of the e-commerce ecosystem are based in China.

The government can push companies to encourage transactions using the government’s digital currency, thus affording the government substantial control over the rapidly expanding e-commerce sector.

Japan

Alongside China’s recent announcement, Japan has also stated that it will be implementing new cryptocurrency regulations. These include the registration of exchanges with the Financial Services Agency, regular auditing, minimum capital requirements, and identity verification for customers.

This meteoric rise came to a crashing halt in 2014, when Mt.Gox filed for bankruptcy following the alleged theft of 750,000 customer bitcoins and an additional 100,000 firm owned bitcoins due to a security software malfunction. Since then Mt.Gox CEO Mark Karpeles, has been arrested twice for the disappearance of the aforementioned bitcoins valued at $480 million.

While the Mt.Gox scandal soured Bitcoin in the minds of the Japanese public, there are is still significant interest among Japanese firms. The new regulations further cement a code of conduct for bitcoin exchanges, reducing uncertainty and risk for companies interested in joining the digital fray. Interested parties include Sumitomo Mitsui Financial Group, Fujitsu, and Mitsubishi UFJ Financial Corporation.

Japanese financial firms are seeking new markets, and are viewing digital currency markets as a potential growth market. Currently, said corporations are limited by Japanese laws that permit banks from owning more than five percent of a venture outside of the financial sector, or more than fifteen percent in the case of bank holding companies.

Japanese entrepreneurs have noticed the void left by the collapse of Mt.Gox and have not only sought to create new exchanges, but also create their own ‘Made in Japan’ digital currencies. One of these is FujiCoin, created by an eponymous company in June 2014.

South Korea

2013 was also a portentous year for digital currencies in South Korea, as in December the Bank of Korea moderated its hitherto negative stance, musing on their eventual usage by the general public. While not a seemingly big announcement, it marked a shift in the Korean cryptocurrency landscape. During the same period, Korean bakery chain Paris Baguettes, became the first physical store to accept bitcoin payments.

Fast forward to 2016, and Kevin Lee, CEO of Bitcoin Korea highlights that “most Koreans are interested in bitcoin for investment purposes. They do not care about the central bank of Korea’s policy. The Korean government will follow the international trend of bitcoin.”

A major hurdle for digital currencies in any country is increasing awareness and usage outside the limited circle of early adopters and tech aficionados. To this end, South Korea has seen a major effort to promote digital currency use, with 7,000 regular ATMs now allowing bitcoin purchases. This is the result of a partnership between Coinplug, a Korean bitcoin exchange, and Nautilus Hyosung, the world’s fourth largest ATM hardware producer.

All three governments are wading into uncharted territory, with interesting developments to unfold in 2016.