The Federal Reserve has little appetite to make policy based on the economic situation outside of the US, but minutes from its most recent meeting show that it is being forced to.

Early in her tenure as Chair of the Federal Reserve, Janet Yellen told the US Senate that what happened in international markets would not affect the Fed policy. At that time, the Fed’s slowdown of quantitative easing had just led to a massive outflow of capital from developing economies. The Fed’s focus would remain on unemployment and inflation, not international capital flows.

Fifteen months later, international markets have become an integral variable in the Federal Reserve’s decision over raising interest rates because they are the greatest threat to sustained economic growth in the US.

In the minutes of the Fed’s late April meeting, a majority of the members of the Federal Open Market Committee (FOMC) seemed to agree on three major points: domestic demand and inflation numbers are moving in the right direction, weakness in international markets has become the main drag on the domestic economy, and the Fed will not raise interest rates at its June meeting.

Despite a number of economic indicators appearing to soften thus far in 2015—including real GDP growth, job growth, industrial production, and residential investment—the minutes and recent statements by Ms. Yellen indicate that FOMC members believe this trend is short-lived. One-time events such as the Northeast’s extreme winter weather and the West Coast port labor disruption were to blame, aided by the numerical impact of low energy prices and statistical noise.

Because the Fed remains confident that the US labor market and inflation are on the right track after considering these transitory factors, the justification for maintaining near-zero interest rates past June came from outside the US. A strong dollar and weakness in certain key international markets were the main reasons.

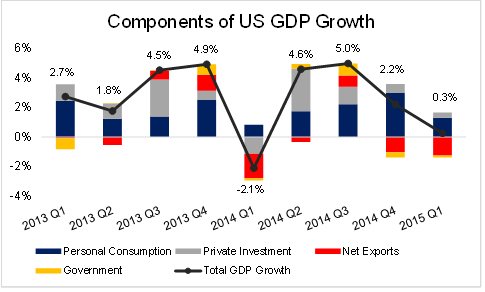

The US dollar is worth 20% more than it was one year ago compared to a basket of six other major currencies, even though it has even fallen 5% from its March highs. As a result, US exports have dwindled as they have become relatively more expensive. In the first quarter of 2015, net exports were a 1.25% drag on US GDP, which grew at a disappointing 0.25% overall.

Source: Bureau of Economic Analysis

The dip in industrial production in recent months is a direct impact of the currency effects, although the Fed minutes noted that auto production appeared to be strong for the second quarter.

But weak exports are only partly a result of exchange rates; the markets that import US products are growing slowly, even in their own currencies.

The Fed acknowledged that it had concerns about this weakness, paying particular attention to Europe and China. With Greece nearly running out of the money it needs to repay its creditors, and negotiations with Europe in a quantum state of advancing and stalling at the same time, financial conditions remain on edge in Europe.

In China, relatively slow growth in the last several months have heightened concern about financial stability and an equity bubble. Combined with a prolonged crackdown on corruption by Premier Xi Jinping, China’s growth and consumption could remain depressed for an extended period of time.

Domestic data has not put the Fed under urgent pressure to raise rates, but a June rate hike was still a reasonable expectation before taking into account the swirl of international uncertainty. Now, Fed officials and observers are leaning towards a September rate hike.

Of course, the first rate hike by the Fed is just the beginning of a multi-year cycle of rate increases. The pace of that cycle may also be slowed by international headwinds. The weak growth that is preventing a rate hike in June is not forecasted to end imminently, and may even be accentuated by the divergence in central bank policy between a tightening Federal Reserve and accommodation by the ECB, People’s Bank of China, and dozens of others.