Vehicle production is taking a toll due to the ongoing computer chip shortage. According to a report by Goldman Sachs and forecasts by advisory experts, they predict the shortfall to persist throughout the rest of 2021, into 2022, and 2023, since demand will remain strong and supply will remain restricted.

Reasons behind the chip shortage

Several automakers such as Tesla, GM, and Fiat Chrysler cut output in the first half of 2020 in anticipation of low sales due to the COVID-19 pandemic. The manufacturers’ primary setback was the decline in sales. To prevent the virus from spreading among workers, most firms in North America have shut down their operations. The demand for automobiles rebounded after the pandemic’s height, but chip supply could not keep up. Automobile manufacturers have had a particularly difficult time obtaining these chips since semiconductor manufacturers prioritize smartphone and other electronic goods manufacturers because they are often more profitable customers. Because of the pandemic and the switch millions of Americans made to working remotely, this caused a surge in PC sales and other consumer electronics. Because these electronics rely on chips, it creates a ripple effect across other markets in the U.S. (i.e., the automobile industry).

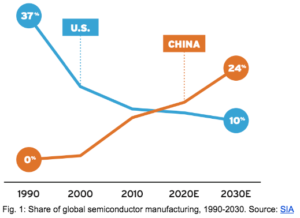

Due to the effect of these shortages, automobile manufacturers have ceased manufacturing, which means fewer automobiles for dealers to sell, which also means fewer incentives and offers. Additionally, this implies that used vehicle costs are once again on the increase. Due to the pandemic, people are purchasing more “smart” devices, which is also delaying manufacturing. Globally, China was somewhat more proactive, stockpiling as many of these chips as possible. While many manufacturers were unable to purchase due to a lack of demand, that demand suddenly increased, leaving them with a supply shortfall. According to a report by the U.S. Semiconductor Industry Association and Boston Consulting Group, the United States’ share of global installed wafer fab capacity has decreased from 37% in 1990 to 12% in 2020. Asia saw a precipitous increase in the creation of new fabs over the same time, to the point that it currently accounts for 80 percent of global capacity.

Fig. 1: Share of global semiconductor manufacturing, 1990-2030 | Source: (https://semiengineering.com/can-the-u-s-regain-its-edge-in-chip-manufacturing/)

Even if a firm develops its own chips, it is unlikely to manufacture them. Companies such as Taiwan Semiconductor Manufacturing Company (TSMC) or Intel have outsourced them to nations such as China. The reason for this is that it has become more affordable to construct semiconductor production plants outside of the United States. These foreign governments provide more enticing financial incentives for semiconductor plant construction, such as tax cuts and grants. Additionally, there is less regulation in countries like Asia. Additionally, there are not as many jobs generated in the US to operate such high-tech industries. It’s critical to understand that a semiconductor chip is not interchangeable with a smartphone or a vehicle. Each is application-specific. A particular chip is required for technology in phones and automobiles, and demand is strong as manufacturing ramps back up and demand for new vehicles reaches an all-time high. As we add more safety technologies and manufacture more electric vehicles, demand exceeds supply. Numerous automobile manufacturers are finally regaining control of this critical product, but they will not be able to scale it up quickly enough.

The Ripple Effect

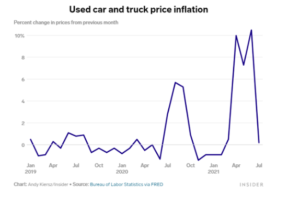

That’s not all; with a rubber scarcity, another problem arises. Rubber from trees is utilized in wiper blades, belts, tires, and gaskets, among other applications. What happened to all the rubber? To be sure, demand for auto components was low, but demand for rubber gloves was strong. As a result of the increasing demand, rubber suppliers delivered it all to rubber glove makers. Rubber trees thrive in warm areas such as Thailand, and the scarcity may last for a long time. The reason for this is that it takes about seven years for a rubber tree to develop to the point where the material can be used. The basic conclusion is that there is a strong demand for new automobiles. There are fewer options at dealerships, and consumers are now looking at used vehicles, which have also risen in price by approximately 0.5% in March of 2020 to 10.5% in June 2021. A surge in car prices can all be attributed to the following factors: chip shortage, automobile manufacturers’ inability to fulfill demand, cheap loan rates from lenders combined with good credit scores, and more consumer savings.

Fig. 2: Used car and truck price inflation, Mar 2020-Jul 2021 | Source: (https://fred.stlouisfed.org/series/CUSR0000SETA02#0)

Chinese companies continue to depend significantly on Qualcomm chips in the United States. Additionally, they depend on chips produced by Taiwan’s TSMC. China has recognized that it is reliant on a number of foreign firms to provide semiconductor equipment. China has placed more importance on chips in recent years. Semiconductors are included in the Made in China 2025 industrial strategy, a government effort aimed at increasing the production of high-value-added goods. China’s goal is to manufacture 40% of the semiconductors it consumes by 2020 and 70% by 2025. This is backed up by Beijing’s billion-dollar investment in the country’s semiconductor sector. The drive to become more self-sufficient in semiconductors has been accelerated by the US-China trade war and Washington’s deliberate targeting of China’s access to critical chips.

When Will the Shortage End?

The Biden Administration has taken steps towards finding a solution to the shortage. In February, President Joe Biden issued an executive order mandating a 100-day assessment of semiconductors and other critical items. The Biden administration is increasing chip manufacturing and forming a task group to address supply chain issues in a variety of electronics-dependent industries. The administration is also dedicated to improving apprenticeship and training programs for a sector that has long had a skills shortage.

This past June, the U.S. Senate passed the U.S. Innovation and Competition Act, a $250 billion measure aimed at countering China’s technological ambitions. The law specifically dedicates $52 billion to semiconductor R&D and manufacturing efforts. In addition, a grant program administered by the Commerce Department would be established to match financial incentives provided by states and local governments to chipmakers that upgrade their existing facilities or construct new ones under the terms of the bill.

Critics of Biden’s plan believe $52 billion is insufficient in the semiconductor sector. Numerous advanced fabrication plants used to manufacture these chips cost $10 billion or more. Particularly when one considers what other nations are doing. South Korea launched a $450 billion joint venture with many of its largest businesses, including SK Hynix Inc. and Samsung which will go toward semiconductor R&D. China has committed almost $1.4 trillion to a variety of technological projects, including chip development. Other critics believe the $52 billion is simply a short-term solution; and without a strong manufacturing supply chain capable of supporting systems-level production, even the finest chips would fail to provide the industry with the resilience, security, and creativity that consumers want. Ignoring long-neglected supply chain sectors will have a detrimental effect on the entire electronics manufacturing industry in America and the economy as a whole.

Some experts, on the other hand, fully oppose the federal spending going towards U.S. semiconductor production. They argue this method will neither help the U.S. microelectronics sector compete on a global scale nor use corporate or other private resources to assist in doing so. And that the long-term consequence of this strategy is that the U.S. microelectronics industry will be at a significant disadvantage. Republican lawmakers highlight the risk associated with the approach of the bill. U.S. Senator Mike Lee of Utah argues that the U.S. should avoid excessive reliance on government-funded research. America’s technical advantage over centralized economies, such as those controlled by China, is due to the private sector, which produces novel ideas and takes calculated risks that government bureaucrats avoid. The less freedom the private sector has to explore new ideas and the more rewarded it is for focusing its research on a small number of government-approved areas, the quicker the US technological edge will erode. Other opponents emphasize the fact that the $52 billion has been labeled as emergency spending. This classification allows for more government spending and for it not to count toward budget limits.

Analysts believe that the majority of the most troubling shortages will begin to alleviate in the third or fourth quarters of 2021. Though, it may take until mid-2022 for the resultant ships to make their way through the supply chain and deliver vehicles to lots. The supply relief will most likely not come from large-scale national investments by the U.S. The problem with such investments and establishing new foundries, such as those in Arizona, is the amount of time needed to get them up and running. In fact, according to International Data Corporation (IDC) analysts, the semiconductor shortage is expected to subside far before any of these facilities come online. It is more likely that supply relief will come from older chip fabrication facilities and foundries that use less creative methods but are still capable of producing and shipping goods.