Could Zambia’s Debt Default Signal a Domino Effect on the African Continent?

https://pixabay.com/photos/zambia-roadsign-africa-2646990/

In November 2020, news outlets reported that Zambia had become the first African country to default on debt against the backdrop of the Covid-19 pandemic, after opting out of a $42.5 million eurobond repayment. Zambia’s external debt payments have increased significantly since 2014, from 4% of government revenue to an estimated 33% in early 2021. As neighbouring countries in Sub-Saharan Africa continue to suffer the economic squeeze of the pandemic, there are fears that others will follow Zambia in defaulting sooner than experts anticipated.

How did we get here?

Zambia was impoverished in the 1980s due to large debt payments, falling copper prices and austerity policies introduced by the Zambian government. Large spending cuts, as a result of trade liberalisation, worsened Zambia’s economic situation. The economy only began to improve in 2005 after the country finally qualified for debt relief from the IMF and the World Bank. However as a result of accepting the debt relief, the IMF prescribed privatisation of many Zambian institutions. This meant the government was forced to overturn a parliamentary vote against privatising a bank. The move was unpopular with Members of Parliament despite the failure of state-owned enterprises in the 1990s, due to concerns that development finance institutions would take full control of the country’s economic recovery. However, the granting of debt relief coincided with an increase in the price of copper, one of the country’s most valuable exports, which together kickstarted Zambia’s economic recovery.

But despite these positive economic developments, Zambia remained a very socio-economically unequal country. Poverty levels in urban areas were estimated to be 53% and in rural areas, up to 78%, at the turn of the 21st century. Compounding Zambia’s economic challenges was high interest loans, paid by private lenders interested in making a quick profit.

Zambia’s prayers were seemingly answered in April 2020 when the G20 announced that some bilateral debt would be suspended. This would have, in principle, helped Zambia solve its debt problem. However, the so-called ‘Debt Service Suspension Initiative’ was criticised for not including private lenders or multilateral institutions. Most of the debt burden in Zambia is owed to private lenders, which were exempt from the initiative, with some set to make a healthy 75% to 250% profit from Zambia’s debt. These private lenders found themselves with more to gain than lose financially from continuing to lend to Zambia.

With a debt burden now aggravated by the effects of Covid-19, Zambia had requested a suspension of debt and interest payments from the private lenders. However, this has been denied after Zambia missed the deadline to pay interest on US dollar bonds, following its failure to secure an agreement with bondholders for a six-month standstill on debt repayments. This, ultimately, pushed the country into default.

Debt and Covid-19: Implications for Zambia

The announcement of the default came in November 2020, approximately nine months after the first cases of Covid-19 were discovered in the country. However, the economy was suffering due to mounting levels of debt prior to the pandemic. Zambia was already due to pay $1.7bn to service its debts, which equated to more than 8% of the country’s GDP for 2020. Worryingly, Zambia now faces a prolonged period of discussion about the terms of the default with the IMF in hope that there will be an agreement for a $1.3 billion loan. Political experts believe that the terms could serve as a template for other countries on the verge of default including Angola, Chad and Congo-Brazzaville.

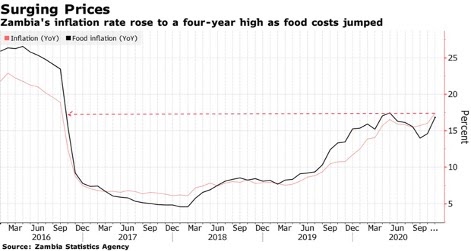

In the meantime, Zambia is proposing to reduce the economic debt caused by the pandemic by reducing spending on healthcare and increasing spending on the serving of debt repayments. But Zambia’s economic forecast remains bleak. By the close of 2020, Zambia’s inflation rate had climbed to 17.4% – its highest level in four years. The inflation rate, coupled with a rapidly depreciating currency, has tipped many Zambians into poverty. Within two months of the announcement of the default, non-food prices rose by approximately 18.2%. Eurodad estimates that the total percentage of the population living below the poverty line, which has sat at around 58% since 2005, is likely to increase as a result of the ‘default effect’ and the broader implications of the pandemic for Zambia’s economy.

A key impact of the pandemic, for example, has been disruption to businesses in the informal economy, as a result of measures to prevent face-to-face interactions. In addition, the tourism industry, which contributed a considerable 7% to Zambia’s GDP in 2019, suffered damaging losses due to border closures and international travel restrictions.

Fast-forward to March 2021, and Zambia is facing a surge in Covid-19 cases, just six months after the government authorised the reopening of the economy following the first wave of cases in early 2020. Coupled with a decrease in healthcare spending, Zambian health facilities are feeling the strain of limited resources, notably a lack of oxygen supplies, ventilators and personal protective equipment.

Credit: https://www.bloombergquint.com/onweb/zambian-inflation-accelerates-to-four-year-high

Could Covid-19 Push More African Countries into Default?

It’s safe to say that the effects of the pandemic have been significantly felt by Zambia’s fragile economy, and the same can be said for neighbouring countries as well. Should more countries in Africa default, the effects would be devastating for healthcare systems. In neighbouring Zimbabwe, where people have endured years of economic hardship, doctors have gone on strike to protest against unpaid wages, unsafe working conditions and being over-worked during the pandemic.

Even though this geographic area was named one of the world’s fastest growing economies in 2019, it now faces its first recession in 25 years. The most adversely impacted countries are likely to be those that are politically unstable, and those which are dependent on the export of commodities such as oil and metals, as well as the tourism sector. Most of the countries falling into those categories are also the ones who have large outstanding debt repayments, which is likely to compound their susceptibility to economic downturn.

Planning Ahead

International aid agencies including Oxfam have called for debt to be cancelled, especially for countries in Sub-Saharan Africa who simply cannot repay their debts. At the current moment however, this is unlikely. For this reason, Zambia’s upcoming presidential elections could prove more significant and consequential than usual elections as the new administration is set to make pivotal decisions about the country’s economic future. The serving president, Edgar Lungu, is expected to forgo any efforts for fiscal reform to protect his chances of retaining the presidency in August 2021. His administration’s strained relationship with the IMF and his personal desire to implement his agenda without the influence of Western powers, also inform his opposition to fiscal reform. The IMF, although having initially met with Zambian representatives to discuss a loan, may therefore choose not to agree to an extended credit facility until after the elections to avoid possible interference.

Zambia and its neighbours face an agonisingly long few months, as the Covid-19 pandemic continues to damage fragile economies. It will therefore not come as a surprise if other countries follow Zambia suit and default before the end of the year. Now, development finance institutions working in collaboration with countries at risk, must carefully plan out the road ahead to prevent a default domino effect toppling the economy of the African continent.