April 20th, 2020 was the first day in history where oil recorded negative prices. US oil benchmark West Texas Intermediate (WTI) fell from $17.85 at the start of the trading day to negative $37.63 by the close. This comes at a time when OPEC+ have agreed to cut output by 10million barrels a day in an attempt to stabilise oil prices.. This demonstrates that in the face of efforts from supply-side nations to prop up prices, demand continues to descend at a relentless pace, showing no signs of wavering in the short term. This, coupled with limitations in storage facilities at American hub Cushing, Oklahoma, indicates only a deepening bearish market sentiment of oil markets from investors.

Covid-19 Impact: Initial oil volatility is worsening

Since the beginning of the Coronavirus pandemic, there has been a loss of 1/3rd global demand – more than 30 million barrels per day (BPD). The virus instilled a level of uncertainty for oil traders, but the catalyst for the initial drop in price can be attributed to the escalating price war between Russia and Saudi for market share, eventually leading Saudi to flood the market with oil. This oversupply dragged WTI prices below $20 a barrel at the end of March. Thus, increasing divergence in power politics from major producers created an initial frenzy in the oil market and an increasingly unsettling omen for investors.

Supply-side reach an agreed consensus

Tensions eased following the OPEC+ meeting on 9th April, where Russia, Saudi Arabia and the US reached an agreement to cut output by 10million BPD. In theory, this may sound significant, but given that global consumption is approximately 100million barrels per day, this reduction no longer seems appreciable. This was reflected in the markets as oil prices continued to tank even after this consensus was reached, demonstrating the general public’s scepticism of whether these cuts are sufficient enough to dampen oil demand and questioning OPEC+’s ability to reach a future agreement.

WTI Crude prices reach negative

20th April saw WTI oil prices plunge from $17.85 to -$37.63, more than a 300% drop, the largest one day drop for US crude in history. The panic is apparent in the futures market as the May contract expiry approached and traders deliberated on how they would take delivery of physical barrels of oil when storage sites are reaching full maximisation. In contrast, the June contract traded at volumes 70 times higher and rose to $21, entering a super-contango futures market. This large front-month spread made traders not want to roll, nor did they want to hold and take delivery, hence they dumped instead. This expiration squeeze has caused a sell-off of May contracts further pushing down the price and augmenting bearish market sentiment. This has all occurred as driving season approaches and producers are gearing up to increase production for the summertime, making it that much harder and unlikely for oil rigs to be turned off fast enough and protect against a further surplus.

WTI vs Brent

This occurs at a time when Brent Crude remains more stable, declining 3.4% on April 20th. This is largely because Brent is seaborne and can be easily transported through various pipelines and stored via floating storage. Traders are increasingly seeking to store oil in this way as onshore storage facilities become increasingly scarce. This is a major difference Brent and WTI that is currently being highlighted. The US is struggling as they creep increasingly closer to full capacity in its major storage hub in Cushing, Oklahoma. Storage has skyrocketed 48% to almost 55million BDP since the end of February, and according to the Energy Information Administration (EIA), the storage site only has a working capacity of 76million.

Future prospects?

Negative pricing has been a common trend in commodity markets. US natural gas markets fall susceptible due to the dearth of pipeline space, whilst electricity markets, especially in California, often drops below zero due to excess solar. Therefore although this marks a first for oil markets heading into negative territory, from looking at the precedent of wider commodities, we can assume there is a high likelihood that it will take a few weeks for WTI crude to start to recover.

Indicators of how quick this bounce-back will be, partly lie in the June contract, which Goldman Sachs analysts predict will likely see downward pressure in the next couple of weeks and also witnessing of “violent rebalancing” in US production as storage reaches close to full capacity. Following on from this oil crisis will be forced production closures as this supply surplus leaves no other option than to leave oil in the ground. Unless the US can clear up its storage problem, regardless of any unrealistic pick up in demand, it is likely to see future contracts move lower down into single digits. Especially June-20 and July-20 contracts as this storage situation is unlikely to change any time soon. With float storage already far above the 5-year average, hitting max capacity in Cushing will only tank prices even further.

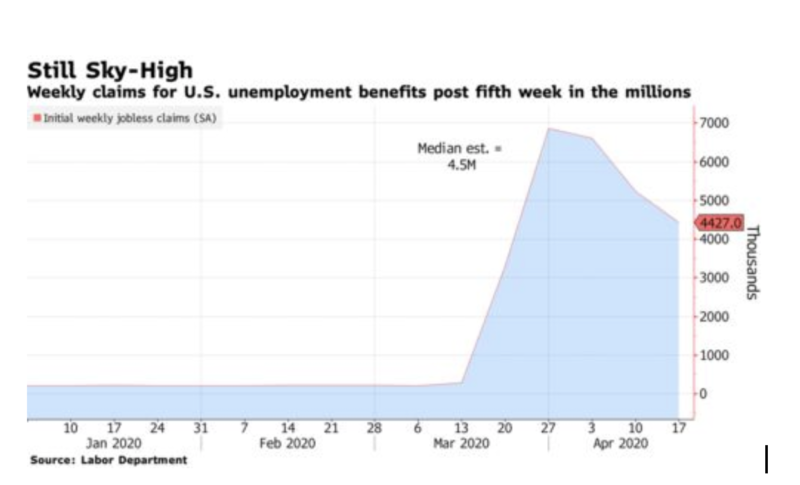

In macroeconomic terms, Coronavirus has wiped out approximately 25 million jobs in the US, taking out all the jobs created since the 2003 and 2008 recessions. Central Banks globally have cut interest rates, restarted Quantitative Easing and provided other fiscal stimuli to try and keep the economy afloat. Despite the S&P 500 recovering about half of its approximate 35% loss since its February highs, it is more than likely that a further downside is to come over the next year for both global equities and employment rates. The longer-term consequences of Coronavirus are still unknown. In the meantime, a deflationary ripple effect across the global economy can be seen, as Central Banks attempt to sustain economies’ survival as the Coronavirus pandemic continues to debilitate businesses and paralyzes transportation worldwide.

Who gains from this crisis?

Whilst disaster struck in oil markets, we see a polar opposite reaction in the renewable energy markets, with the US increasingly depending on renewables for electricity, whilst across the globe, renewables share rising to 43% in the UK and Europe. Such events have the high potential to further push global economies’ incentive to increase usage of renewables and dampen our dependence on fossil fuels. In addition to renewable energy companies, major importing nations such as China and India also have the potential to gain. Continued risk and volatility in oil markets allow for cheaper prices for importers.

Conclusion

Coronavirus is likely to be the catalyst that puts an end to the longest US bull cycle in history. With the FED slowly running out of tools, it will likely see the economy continue to contract as unemployment rates and job claims increase. With oil demand falling and supply proving harder than expected to control, US storage sites will make their way up to max capacity. In the short term, no change in demand will save oil prices. One will have to wait and see what OPEC has up their sleeves to see whether or not a supply cut is enough to offset the demand massacre.