Under the Radar: Is a land lottery the solution to China’s housing boom?

Nanjing has begun a land lottery to decide winners among competing bids from housing developers. Will this game of chance reduce or increase corruption?

The demands of China’s surging real estate market has forced Chinese cities to come up with new ways of dealing with rampant developer demand. In a state dominated market, developers have created bidding wars in Chinese cities as the largest urbanization in human history continues apace, despite – and in some cases because of – China’s economic slowdown. Indeed as only 55% of China’s population is urban, there is plenty of growth potential in the Chinese housing market.

Is Lady Luck a good developer?

Development land has become scarce in cities such as Shanghai, Beijing, and Shenzhen; where prices have jumped by 25% over the last year. Shanghai authorities even had to dispel rumors that they were tightening ownership restrictions for married couples, after municipal offices were swamped with couples seeking “divorces” in order to continue purchasing property. With developers in top Chinese cities needing to sell property at up to $15,000 per square foot just to break even, many are turning their attention to China’s second-tier cities.

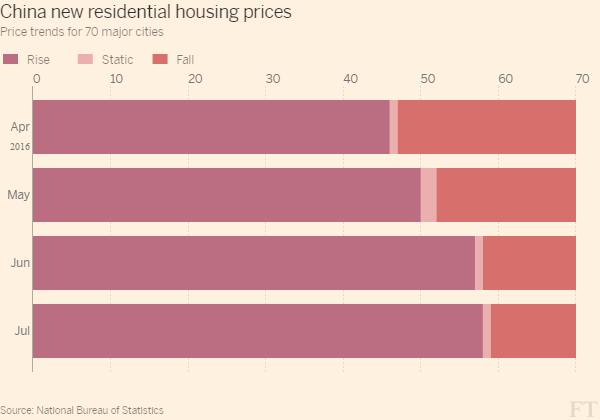

This trend presents Chinese cities with substantial revenue streams, as the sale of development land in China is monopolized by municipal governments. With average house prices in 70 Chinese cities increasing by 7.9% in July and 9.2% in August, municipal governments are raking in the cash. In the past eight months, revenues from land sales across China have reached $300 billion, a 14% increase from the same period last year. As a result Hangzhou has seen its land sale revenue triple since January, with Suzhou, Hefei, Wuhan, Zhengzhou, Shenzhen, and Ningbo all doubling their land sale takings.

The bidding war among developers is so intense, that Nanjing has had to implement a ceiling price on development land. This has not resolved the issue, so this week the city has launched a land lottery system in order to determine winning bids for development land. Specifically, if two or more bidders are willing to pay the ceiling price for a lot, the city will institute a lottery, with the winner of the draw being awarded the contract. Nanjing’s initial four-day land auction this week saw 14 of the 18 lots up for sale reach the ceiling price. This latest auction has already netted Nanjing an astounding $6.07 billion in municipal revenue.

China’s real estate market is not the same as America’s

The money printing efforts of China’s central bank, combined with a lack of alternative investment options has seen real estate become a major sponge for the country’s excess liquidity. Real estate is seen as a safe bet for many investors, who are banking on Beijing’s intervention in the event of a downturn. Consequently, in the first eight months of 2016, real estate investment rose to $960 billion, a 5.4% year-on-year increase. Residential real estate and construction now accounts for more than 10% of China’s GDP.

Such increases in housing prices have raised concerns about the creation of a Chinese housing bubble. While systemic risks are increasing, China is not in the same position as the U.S was prior to the subprime mortgage crisis. Firstly, the images of Chinese ghost-towns are misleading, as they (generally) highlight a difference in Chinese consumer trends, rather than speculative oversupply. The majority of homes sold in China are apartments, and 80% of these are purchased a year or two prior to construction. This process, known as pre-sale, is what creates ghost cities like Zhengzhou.

Yet while Zhengzhou has often been displayed on lists of Chinese ghost cities, buyers purposely purchased houses with the intention of not moving in for several years. This was a calculated move to wait for other municipal infrastructure – like the local metro – to be completed, thus raising housing prices. This combined with the fact that less than 10% of Chinese home buyers are investors looking to park money – the vast majority are owner-occupied – means that Zhengzhou is now a thriving city.

More than 70% of Chinese household wealth is in housing; similar to the U.S. Both tacit and implicit assumptions about government efforts to safeguard the housing market has seen banks go on a lending spree: new mortgage growth has increased by 111% in the last 12 months. Another element is the fact that China allows tenants to purchase their government housing at a deep discount; a policy that has led China to have one of highest homeowner rates in the world – 89% compared to 64% in the U.S and UK. Despite this, increasing incomes coupled with the often sub-standard nature of state housing creates a major incentive for newly wealthy urbanites to upgrade, a key consumer demographic in China.

Price increases have seen the average cost per square foot in China reach $171, versus $132 in the U.S. However, unlike the U.S, there are low levels of leverage in the Chinese housing market, as 15% of buyers pay with cash, and potential homeowners must provide a minimum 30% deposit. These facts, combined with the 300% increase in Chinese household savings over the last 10 years (now $8.5 trillion) puts the Chinese market in totally different world than the U.S. For instance, whereas housing prices surged past real income growth in the U.S, China’s average 9% annual housing price increase over the past 10 years has been outpaced by 12% annual nominal urban income growth.

Corruption rise accompanies housing boom

While the fundamentals of China’s housing market are relatively sound, the sector does face risks. Firstly, risk distribution is skewed, with municipalities halfheartedly trying to dampen the boom, while benefiting hugely from their development land monopoly. Moreover, municipalities can easily become complicit in price inflation, expecting a blank cheque from Beijing should the market burst.

China’s housing boom has coincided with Xi Jinping’s anti-corruption drive, and as such corruption in the real estate market has come into Beijing’s cross-hairs. Beijing has made it a foreign policy priority to clamp down on money illegally leaving the country only to end up in foreign real estate investments. Moreover, China is pressuring countries to extradite corrupt investors and developers. Despite this, the main risk facing China is domestic corruption, especially in the housing market.

Zhao Jin’s illegally tall development project

For instance, in 2014, wealthy developer Zhao Jin and his father were arrested on corruption charges. Zhao had used his father’s influence as former secretary general of the CCP committee for Jiangsu province to seal development deals in Tianjin. Municipal authorities were further incensed when in 2015 the Waterfront Ginza development built by a company owned by Zhao ignored its building permits. Specifically, the three buildings were up to 30 stories taller than originally promised. The Tianjin government decided to tear down the brand new buildings, in a poignant warning to corrupt developers.

More recently, as of July the mother of the mayor of Vancouver’s Chinese girlfriend is facing the death penalty for her involvement in a real estate scam. Qu Zhang Mingjie, a former Harbin city official conspired with the head of Dangjiang Agricultural Technology Co, Wei Qi. As the official overseeing the purchase of farmland, Zhang worked with Wei to doctor the sale agreement to transfer construction rights to Wei’s company. Said rights were later transferred to Harbin Xiafa Real Estate Development Co. another one of Wei’s companies, with the aim of building a high rise development. Over the course of several years after the 2009 deal, Zhang embezzled $52.5 million from local farmers and the Harbin government.

Zhang and Zhao’s cases demonstrate the dangers facing China from collusion between municipal officials and developers, especially given the monopoly on development land enjoyed by Chinese cities. Concerns about favoritism and a rigged system (especially if lotteries become the norm) will undermine investor confidence and damage China as an investment destination. In this light Nanjing’s land lottery could easily be manipulated. Introducing and formalizing an element of chance into billion dollar development deals only makes it easier for corrupt entities to game the system.

Under the Radar uncovers political risk events around the world overlooked by mainstream media. By detecting hidden risks, we keep you ahead of the pack and ready for new opportunities.

Under the Radar is written by Jeremy Luedi.