When European Central Bank (ECB) President Mario Draghi began his tenure in 2011, Berlin and Frankfurt were relatively supportive with the understanding that they retained tacit, informal influence over ECB actions. This relationship has since deteriorated, first with the Outright Monetary Transactions program initiated in 2012 and the subsequent Asset Purchase Program (APP). The motivation for each program, designed to raise Eurozone liquidity, is to slow the fall in inflation levels and fend off deflation.

Initiated in March 2015, the APP is a 2 year, €1.8 trillion bond buying program, primarily targeting the purchase of government bonds to increase money supply, spur growth, and trigger inflationary pressure to stabilise falling prices.

At its inception, policy makers in Berlin begrudgingly accepted the programme which, for the first year fetched approximately €60 billion in monthly bond purchases. In March 2016, this monthly average was increased to €80 billion, leading to outcries from the German government and legal actions to curtail the bond purchases.

Weakening German influence

The significant uptick in monthly bond purchasing has clearly demonstrated that any perceived influence, Berlin and Frankfurt may have had over ECB activity has vanished. Germany has long seen the ECB as a Bundesbank writ large for the European Monetary Union (EMU), but recently the ECB’s actions fly in the face of the traditionally tighter monetary policy they prefer.

Bundesbank President Jens Weidmann exemplified the German preference for tightened liquidity in a recent appeal for Brussels to do more to control Member States’ budgetary spending.

German Finance Minister Wolfgang Schäuble is perhaps the most vocal and direct in his condemnation of recent ECB actions. Mr. Schäuble attributes the rise of German right wing populism to the ECB’s quantitative easing measures, and his aversion is echoed in a series of legal actions directed against the ECB challenging changes to the implementation of the APP.

In addition to the increase in monthly bond purchases, the ECB promises to start buying corporate debt, a move litigant Markus Kerber argues will artificially distort capital markets.

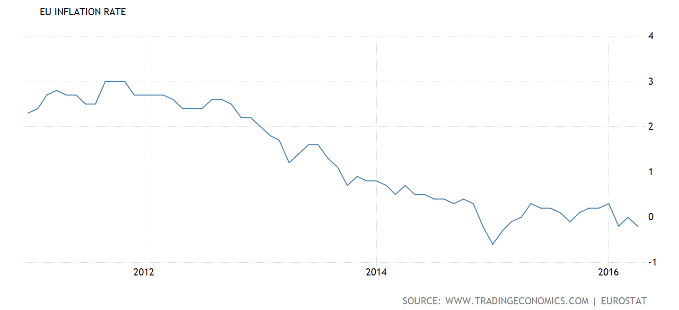

Draghi defends recent actions reminding challengers that one of the few roles of the ECB is to maintain stability of the Euro, an effort which in recent years has been met with failure as inflation levels have fallen.

Further, the ECB’s actions reflect the actions of central banks around the world which have used and are using similar measures to spur growth. Recently, price levels have stabilised somewhat around zero, but Mr. Draghi intends to continue a policy of quantitative easing until price levels have risen to a stable 2% inflation rate.

It is unlikely continued German opposition to ECB loose money policy will be heeded. Previous legal challenges have been unsuccessful in curtailing ECB actions through the courts. Ironically, it is a cherished hallmark of German monetary history which holds the strongest protection for ECB actions, the absolute independence of the central bank.

To this end, Bundesbank board member Andreas Dombret provided some cover for ECB actions in May, defending the autonomy of the bank from political attack.

Implications for Germany’s domestic economy

As it appears that the ECB policy of quantitative easing will continue at least through March 2017, the ongoing infusion of liquidity will continue to impact the German macro-economic climate.

The German cultural propensity to save will be affected by the increase in liquidity. As interest rates fall and the APP continues to flood liquidity into the market, the value of German savings will drop as well. This does not bode well for Germany with a 10% personal savings rate.

While savings will be hit by the ECB’s policy choices, German exports have realized significant growth. Germany’s balance of trade is surging with the devaluation of the Euro against an international currency basket. Complemented by a recent uptick in Germany foreign currency reserves, the reduced cost of German goods has driven a rise in a historically export-driven economy.

Led by the automotive industry, German export levels reached an all time high in March 2016. These trends are likely to continue for the duration of the ECB’s quantitiative easing activities.