South Korea’s ruling party recently suffered a major blow in parliamentary elections, losing its majority for the first time in over a decade and a half. How will this change affect prospects for investors in South Korea?

On April 13th, South Korea’s ruling center-right Saenuri party lost their majority in parliament. Parliamentary elections left Saenuri, the party of current President Park Geun-hye, with only 122 seats. The main opposition parties, the Minjoo and People’s Parties, control 123 and 38 seats respectively. The loss is a sharp blow to conservatives; this is the first time in 16 years that Saenuri has lost its majority in parliament. What are the consequences of the recent shift for Korean economic and foreign policies?

A change in fortunes

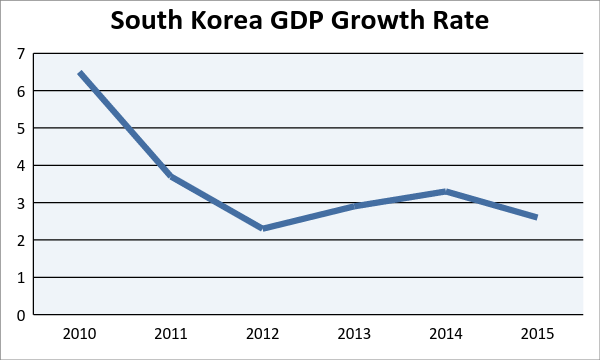

Saenuri’s reversal in fortunes stems in part from Korea’s recent economic challenges. Slowing growth, falling exports, rising debt, and growing unemployment among young Koreans have led to mounting discontent with Saenuri and President Park. Additionally, crackdowns on leftist groups sympathetic to the North Korean regime have left some Koreans wary of Saenuri’s respect for civil and political liberties. Just as significantly, Saenuri’s internal travails, particularly clashes over Park’s leadership style and factional infighting, have undermined the party’s popularity.

Stalemate intensifies

This election will create significant political risks for investors and businesses in Korea by strengthening parliamentary gridlock which will in turn hamper economic reform. Now that Saenuri has lost its majority, it will be even more difficult to get the 60% parliamentary support needed to adopt new legislation.

The Minjoo and People’s parties disagree with key components of Saenuri’s reform initiatives, and will likely stymie efforts at labor reform, deregulation, and changes to monetary policy. Just as importantly, the opposition parties have political incentives to obstruct the Saenuri in the lead up to the 2017 presidential elections. Both parties will look to undermine Saenuri’s economic credentials by hindering Park’s reform agenda when possible.

This increased gridlock will impede Park’s planned reforms to the labor market. South Korea’s labor laws are notoriously restrictive: According to the World Economic Forum, South Korea ranks 121st out of 140 countries in labor market flexibility. Workers enjoy strong legal protections against being fired, seniority-based promotion and annual raises which impose heavy costs on businesses and reduce their ability to reward employees based on performance and merit. They also impede businesses’ ability restructure, downsize, or fire underperforming employees. These restrictions inhibit economic efficiency and make it difficult for young workers to find employment.

At the end of 2015, Park introduced five labor law revisions, agreed to by major business leaders and unions, to the parliament. Even then, the opposition held up voting ahead of the April elections. Without a Saenuri majority, these bills are now dead in the water. Given the Minjoo Party’s emphasis on populism – particularly social justice and economic egalitarianism – it is highly unlikely to acquiesce to these much-needed reforms.

The Saenuri’s poor showing in the parliamentary elections will also throw a wrench in Park’s planned deregulation initiatives. Park has described excess regulations as a “cancer” for the Korean economy. Small-to-medium sized enterprises, for instance, are estimated to spend an average of 30 million won (26,000 US dollars) annually on certifications. As such, Park has targeted several industries – food, medicine, technology, cosmetics, and oil products – for deregulation in order to attract investment. Without a Sanuri majority, however, it is unclear how these reforms will pass in the legislature.

A final casualty of the recent elections is Park’s efforts at quantitative easing (QE). While Park has touted QE as a solution to Korea’s struggles, the opposition has previously criticized monetary policy as a distraction from other challenges, namely powerful chaebols and economic inequality. Given this earlier stance, the new parliament is unlikely to allow QE to go forward.

A gloomy outlook

For investors, stalemated reforms will produce an uncertain outlook for Korea’s struggling economy in the near to mid-term. South Korea will find it difficult to remain competitive so long as it is unable to address its oppressive labor laws and regulatory system.

For businesses in the short-term, these trends will lead to continued difficulties in coping with inflexible labor regulations, but also a degree of policy stability given the fact that gridlock is unlikely to produce any drastic changes in the coming years. That could well be a positive for incumbent foreign businesses uneasy about too many changes in the future.

In the long term, however, there are broader risks to businesses and investors; the rise of populist parties like the Minjoo and People’s Party and anti-market political sympathies could create further challenges for the already struggling Korean economy.

Looking outward: THAAD

Now that Park is hamstrung at home, she may redouble here efforts in foreign affairs – where parliament cannot obstruct her agenda as easily – to bolster her legacy and her party’s credentials. Given North Korea’s recent provocations and its growing nuclear capabilities, Park is likely to prioritize Terminal High Altitude Area Defense (THAAD) cooperation with the US.

THAAD is a mixed bag for investors and businesses in the region. On the one hand, it will help shore up US and South Korea deterrence against aggression from the North by increasing their capacity to defend against missile attacks. This will contribute to strategic stability on the peninsula, reducing the risk of conflict and the resulting losses to investors that would entail.

On the other hand, THAAD will significantly undermine Sino-South Korean relations, creating risks for businesses involved in commerce between the two states – particularly South Korean businesses operating in China and South Korean firms that depend on China for imports or as a market for exports. Beijing has made it clear that it will oppose THAAD, and will doubtlessly use a variety of policy instruments, including economic measures, to pressure Korea to refrain from THAAD cooperation with the US. This could include punitive trade restrictions like those introduced to coerce Japan during recent Senkaku/Diaoyu island spats. It could also involve travel regulations designed to undermine Korea’s profitable tourism industry.

Overall, South Korea’s recent elections will create a more challenging environment for businesses and investors in South Korea in the near to mid-term.