Despite being the poster child of post-crisis reform, Ireland’s economic policy only has limited usefulness in solving the Greece’s economic crisis.

In response to Greece’s more combative approach to its bailout since the anti-austerity Syriza Party came into office in January, unsympathetic commentators have countered that if Greece had only conducted itself like Ireland, Athens would not find itself again on the edge of default.

Indeed, on the surface there appears to be a case: Ireland’s government debt ballooned after 2008 just like Greece’s, but the former Celtic Tiger was instead able to pay off its bailout—and do so early.

On deeper inspection, however, Ireland and Greece’s stories diverge dramatically. The difference lies not just in the perceived irresponsibility of Greece, but also in the very different nature of the two economies. Ireland found itself fortunate enough to have an economy based on high value-added exports with more resilient trade partners. As Greece tries to begin a recovery, Ireland’s fortuitous trade profile offers a lesson in how to rebuild.

Finding the right trade partners

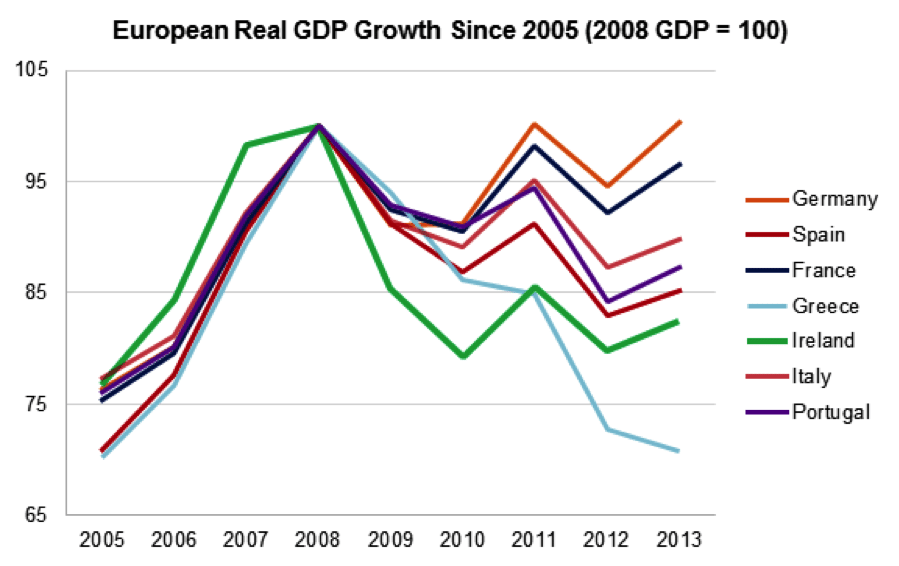

Both Ireland and Greece have struggled to end their respective economic crises. Despite now being the fastest-growing Eurozone country, Ireland still only tops Greece when it comes to growth since the Financial Crisis began.

Source: World Bank

The drag on Greece and Ireland are understandable given the major impact of insolvent and nearly failed banks on their economies. Outside of that, however, structural factors made it possible for Ireland, unlike Greece, to be optimistic about its economy today.

First, Ireland’s exports represented more than three-quarters of its GDP and were sent to economies whose recoveries were relatively fast. This provided a cushion for a struggling domestic economy. The top destinations of Irish exports include nearly all the developed economies that have returned to growth since 2008: the US, UK, Belgium-Luxembourg, and Germany (in that order).

On the other hand, Greece’s exports only made up one-quarter of GDP and are not exported to economic powerhouses, with the exception of Germany. Greece’s top export destinations are Turkey, Italy, Germany, and Bulgaria.

In part, Ireland’s favorable export situation is a product of what it exports: pharmaceuticals and computing hardware. These are extremely lucrative industries with high added value, barriers to entry, and less cyclical volatility—thus protecting Ireland’s producers and employees.

Greece’s exports, on the other hand, are heavily skewed towards commodities: refined petroleum, packaged medicaments, aluminum plating, fresh fish, and raw cotton (in descending order).

Impact of shrinking public sector employment

Greece has been consistently and vigorously criticized for its bloated public sector, where workers are considered to be overpaid and underworked. The austerity required by the terms of its bailout, as well as of Ireland’s, made the cuts to the public sector workforce steep—an effect that rippled through the Greek economy.

In understanding how Greece has stagnated, which may characterize it generously, the whys and wherefores of its public sector bloat are less important than its implications. In 2008, 21% of the Greek labor force worked in a public sector job, while only 17% of Ireland’s did. Since then, Greece has cut its public workforce by 17% and salaries by one-third.

These displaced public employees are not earning wages from the government anymore, and based on the high unemployment in Greece, they are probably not earning a salary from anywhere else, either. In turn, they are buying fewer private sector goods and services, in the end making private businesses worse off.

Greek public sector employees generally earned more than private employees, making the effect even stronger. Ireland’s public sector experienced similar shrinkage, but was a smaller portion of an economy with high private sector wages.

Lessons from Ireland are about industry, not austerity

The lessons from Ireland are not about obliging to austerity. Rather, the lessons Greece can heed as it rebuilds its economy are about the types of industries it wants to foster. Specifically, Greece’s businesses can make higher margins and be more insulated from the economic cycle by exporting fewer unfinished goods.

As a 2012 McKinsey report concluded, Greece should transform its olives and dairy from low-profit margin commodities into high-profit margin olive oil, Greek yogurt, and feta. Of course, that is just one small area of the economy, but it points to a shift in mentality that will benefit domestic companies and their employees.

Ireland has based its export economy off of doing this in the pharmaceutical industry and it attracted multinational businesses and high-wage workers. Of course, Ireland’s accommodative corporate tax system has also helped in this process.

There is no substance to insisting that the Greek government make “tough decisions,” language that is only really useful in campaign rhetoric. Similarly, it is not useful to characterize Ireland as a poster child for austerity success when its economy is still only operating at 85% of its pre-crisis levels and 15% of the nation’s mortgages are in arrears.

This concrete lesson in moving away from a commodities-based economy is much more useful than the vague lessons commentators recommend for Greece.