Evolutionary and revolutionary changes are aligned to restructure the global insurance industry, including the London Market Group. Can LMG and the industry “read the writing on the wall”?

In his 2003 book, The New Financial Order: Risk in the 21st Century, Robert J. Shiller writes, “new information technology… puts economics today roughly where astronomy was when the telescope was invented.” Shiller considers science and technology so powerful that they will eventually lead to “financial institutions sharply different from the ones we have today.”

To Shiller, an obvious beneficiary of this innovation is the global insurance industry, which could “make extensive use of digital information to reduce and manage a whole range of previously uninsured risks.”

If any industry is ripe for disruption, it is insurance. So little has the business model changed that were Edward Lloyd to visit today, he would easily recognize what began in his London coffee house in 1696.

Despite understandable reluctance to harness dynamic forces driving global insurance towards something “sharply different” from what know today, the industry itself is beginning to evolve.

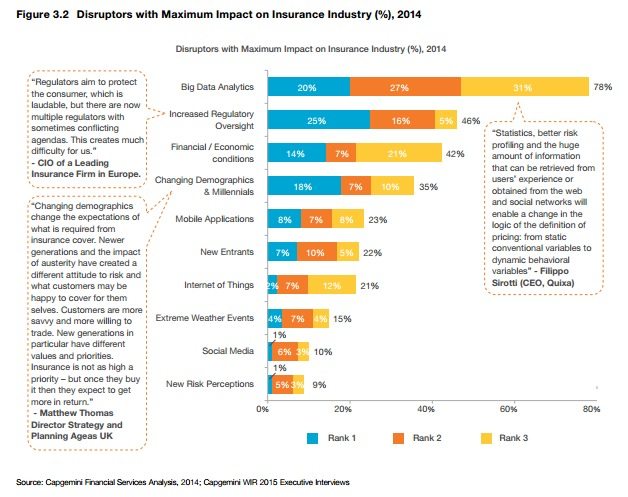

The term “disruption” is not an insurance executive favorite. Yet, the CapGemini 2015 World Insurance Report uses the d-word almost promiscuously. It says, “industry executives identified Big Data analytics as having the greatest impact on the insurance industry, with 78% ranking it as one of the top three disruptors,” far ahead of regulation and economic conditions.

London Matters, a London Market Group (LMG) study on its competitive position, recognizes the importance of data analytics, though LMG downplays the disruptor angle.

“London’s competitive position could be impacted by… smart analytics taking a more central role in the underwriting process,” it states. “The use of analytics is extending beyond just risk pricing to focus on operational efficiency and claims handling.”

It is not evident how smart analytics integrate into London’s competitive advantage without causing disruption. Consider the strengths of the London Market as LMG regards them (see below). Smart analytics will transform all four components of London’s competitive advantage: underwriting, distribution, security and ratings, and ecosystem.

In its “Call to Action,” LMG urges a quick response to preserve its competitive advantage. “London’s capabilities are founded on the specific characteristics of the London Market,” which “risk becoming a weakness when rapid change is required.”

Disruptive forces are reshaping the industry, but LMG does not state clearly what its response should be.

The way forward

The London Market will have to redefine its value proposition to preserve its centuries-old competitive advantage: “Offering analytical capability will add value for the customer,” the reports finds. This much it recognizes, at least on paper.

It is not possible for London to create that value without restructuring its value chain to integrate data analytics into underwriting, operations, and claims. This sort of restructuring is by definition disruptive. It is especially disruptive when the industry, of which LMG is a part, is itself undergoing restructuring due to the same forces driving change in the London Market.

The Boston Consulting Group (BCG), co-author of London Matters, argues that Big Data can have an evolutionary or revolutionary impact on the insurance value chain and improving competitive advantage. For the London Market Group, it will probably cause both.

BCG identifies fraud detection and claims mitigation and prevention as two areas in which data analytics has had an evolutionary effect. But it is at the heart of insurance operations – underwriting – that data analytics will have its revolutionary impact. “In the past, the prediction of probabilities based on averages and the mutualization of risk… was the cornerstone” of insurance.

These predictions are accomplished by what LMG calls “judgemental underwriting.”

Big Data and data analytics offer “predictions… based on individual characteristics.” This is revolutionary. As The Economist puts it, “the law of large numbers is threatened by the rule of precise data.”

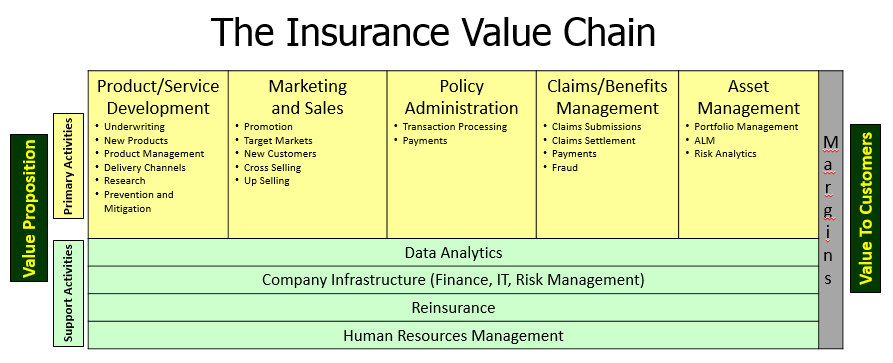

Instead of underwriting large risk pools, data analytics allows for narrow risk pools, even to the point of individual underwriting and pricing, a segment-of-one model. They allow for entirely new types of data – non-traditional data – to be combined with powerful predictive risk modelling to yield superior underwriting decisions. How data analytics will impact the value chain is illustrated below.

A revolution in underwriting poses major impediment for LMG. Its historic competitive advantage rests on ‘expertise-based’ underwriting, which allows London to differentiate its products and price them accordingly. But data analytics is fundamentally a force to commoditize insurance. Its impact narrows margins.

London will find it a very difficult to transition from a differentiation strategy to a low-cost strategy. The two approaches necessitate very different value chain structures. And it is not clear how LMG can use data analytics to preserve its differentiation strategy.

To be fair, LMG sees an opportunity to “reinforce London’s strength in expertise based underwriting.” Culturally, it seems London cannot accept the threat technology represents. At best, London needs “to combine analytical underwriting tools with the experience of the underwriter, not to replace the underwriter altogether.” But that is all they have got.

What is the worst that could happen?

LMG lacks strategy, which is a distinct competitive disadvantage. LMG knows competitive forces are driving fundamental change. It foresees its strength morphing into weakness. It has ideas about what needs to be done. But there is nothing in London Matters to execute, despite the acknowledged need for rapid change.

LMG needs one set of strategies to reconstruct its value chain and another set to compete within a restructuring insurance industry. There is little doubt LMG is working on them, but it seems to have neither at hand, so its concern that “London’s position as the undisputed global market for specialty commercial insurance is under threat” is well-founded.

Change is already here. It appears LMG has an idea of what is coming, but it does not look prepared. To sustain its competitiveness, LMG will have to become an institution “sharply different” from what it has been since Lloyd’s time.