It came as a shock to most, and certainly to markets, when Greek PM Antonis Samaras announced that presidential elections would take place on December 17th rather than in March 2015.

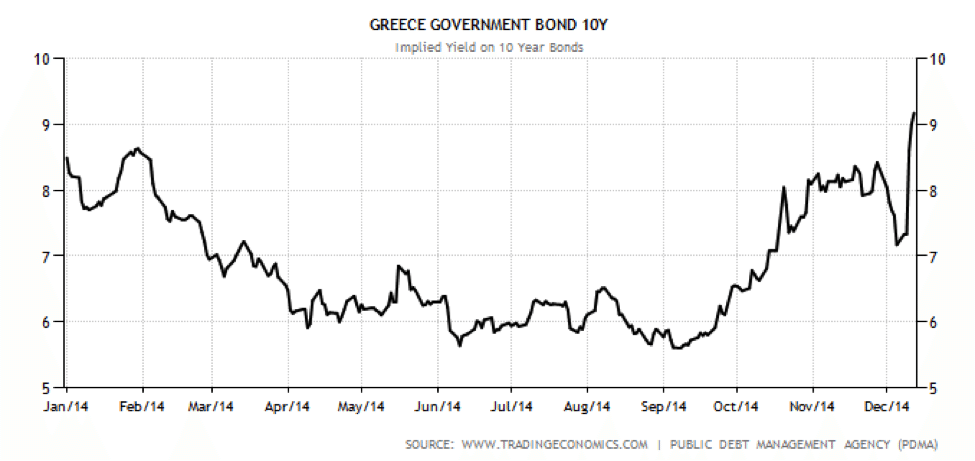

Athens benchmark stock index fell 12.8 percent on Tuesday after the announcement late Monday, and the tailspin has been ongoing since. As stocks have nosedived, the yield on Greek sovereign bonds has soared. It rose to 8.158 percent on 10-year government bonds that Tuesday, and at the moment of writing, the yield has reached 9.15 percent.

The motivation for elections is PM Samaras’ declining sense of control, as his pledge to evict bailout lenders by the end of 2014 is likely to fail. The way yields on Greek sovereign debt have climbed since October has shown that markets do not believe Greece is ready to finance itself without assistance and to carry out reforms.

Moreover, the Greek parliament failed to elect Samaras’ presidential nominee, Stavros Dimas, a pro-European candidate. Samaras’ basis for authority has crumbled. The election is his attempt to reassert himself.

The timing of this election is quite tricky, as the bailout program propping up the Greek economy runs out in two months. Samaras has had to accept a precautionary credit line, the details of which are being ironed out with international lenders, and he might have to stick with the IMF program as well, until March 2016 as planned.

The hope is that the election will sweep uncertainty about the future aside, and provide a clear signal that Greece “wants to be solid.”

Markets jitters have been caused not only by Greece’s questionable creditworthiness, but also by the rise of far-left party Syriza, headed by Alexis Tsipras. Syriza’s calls for erasing Greek debt and ending austerity measures have resonated with the Greek populace. Currently, Syriza is leading the polls, with a 40-point platform. Their policies include:

- An audit of the public debt and renegotiation of interest due and suspension of payments until the economy has revived and growth and employment returned (point 1).

- Prohibition of speculative financial derivatives (point 7)

- Nationalization of banks and ex-public (service & utilities) companies in strategic sectors (points 18 and 19)

It is no wonder that Syriza has drawn votes from austerity-weary Greeks, and that this has worried the markets. Its platform is tailor-made to please, and it reflects no accounting for viability.

In the event that Alexis Tsipras and his party wins, there will likely be tremendous uncertainty about the future of Greece. Claims from debt holders could also become a major issue, seeing as Syriza intends to renegotiate Greek debt. It will be down to a choice between Grexit and debt relief and restructuring.

Jean-Claude Juncker, head of the EU Commission, stated during a debate that he does not want Syriza to assume power in Greece. “I think that the Greeks […] know very well what a wrong election result would mean for Greece and the Eurozone.”

Should Syriza gain power in the election, Greece’s EU membership could become questionable. Samaras seems to hope that the threat of financial chaos will prompt independent MPs and MPs from smaller parties to back him.

His coalition counts 155 votes, and he needs 180. Significant entities will go to great lengths to prevent Syriza rising.

Political powers outside Greece, the IMF and EU are very keen to avoid the prospect of election victory for Syriza. If Syriza is leading in the run-up to the final vote on December 29th, Samaras is likely to promise some version of international relief to win over voters.

Although this is only a presidential election for a post, which in most matters is ceremonial, there is a risk that the Parliament will be dissolved if it fails to appoint a President. In such a scenario, national elections would be necessary, and here too, Syriza is ahead of the pack.

Given the daunting prospect of political instability and financial uncertainty, a far-left victory is less probable but not impossible.

Pierre Moscovici, EU Economic Chief said, “I believe if Prime Minister Samaras chose this way it’s because he’s confident in his capacity to have a successful election.” But if voters were predictable and politicians well-informed of their expected behavior, elections would hardly be necessary in the first place. This one is not a given, either.