Low risk premia for emerging market assets are persistent. Yet, the world is awash with turmoil and uncertainty. How do we explain this seeming contradiction?

The Bank of International Settlements (BIS) usually concerns itself with bonds, bond markets, and bond yields. But a report issued by BIS this month brings to mind simply Bond. James Bond. No kidding. The report attempts to address persistent low levels of volatility in equity and bond markets in developed and emerging economies. It is called, “Volatility Stirs, Markets Unshaken.”

Bloomberg calls the current spate of global crises “symptoms of the most profound revolution in world affairs in almost four centuries.” Yet, markets appear blasé, though they managed to rise from their mid-summer torpor to give short-lived recognition to developing risks. “Geopolitical tensions in late July triggered a temporary rise in volatility,” the BIS states, but by late August “investor risk appetite recovered…and volatility in other asset classes also fell back to the low levels seen in early July.”

Despite this blip, current risk readings remain at some of the lowest levels seen in the last five years, as shown by the CBOE Emerging Markets ETF Volatility Index (below).

If there was one lesson to be learned from the Great Recession of 2007, it is that markets and investors are sometimes catastrophically wrong about pricing risk. In fact, underpricing risk contributes directly to asset overvaluation through artificially low discount rates. As asset bubbles inflate, greed trumps fear.

The BIS report puts it more delicately. “An environment of low yields…coupled with investor confidence…foster risk-taking behaviour. This then tends to be reflected in…a general narrowing of risk premia. As market participants further revise down their perceptions of (market) risk, they may be inclined to take larger positions in risky assets, boosting prices and pushing volatility even lower.”

This mechanism contributes to what we have witnessed in emerging markets lately. There, risk premia have been on a general downward trend relative to US Treasury rates for three years, as can be seen in the following FRED chart.

Bloomberg puts the current emerging market corporate debt risk premium over US Treasuries at 285 bps. That is roughly the same spread home buyers pay today on their secured 30-year fixed jumbo mortgages in the US.

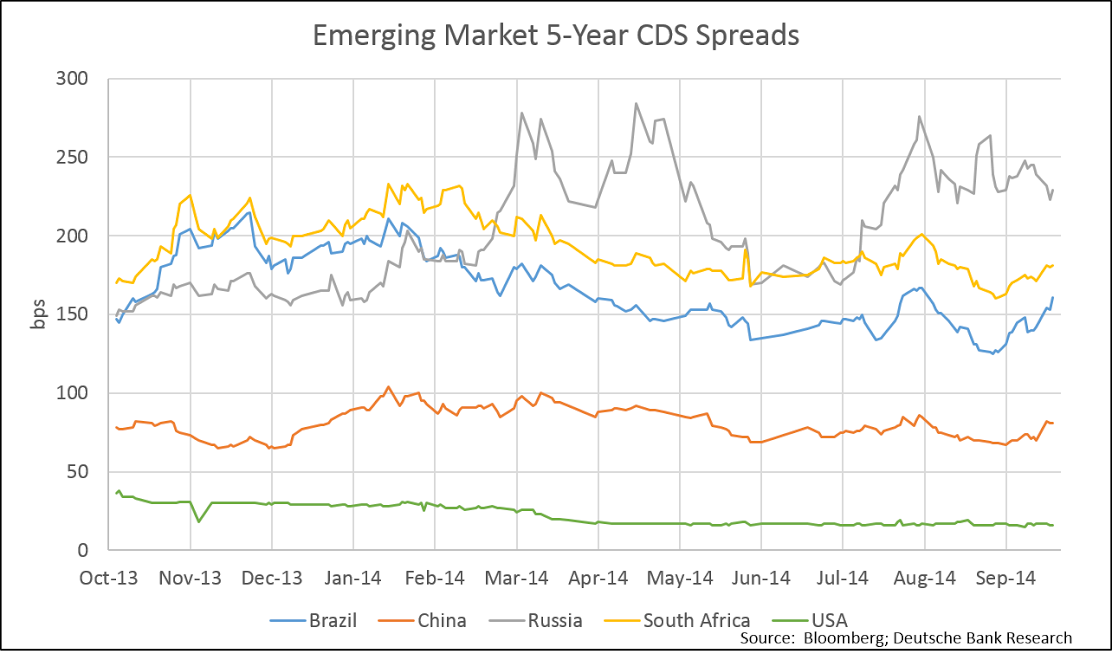

Another way to look at problematic emerging market risk premia is through the lens of sovereign credit default swap rates for important emerging markets. Except for Russia, swap rates have not changed much in the last twelve months. That is, the cost of insuring emerging market sovereign debt is not any higher in today’s turbulent environment than it was last October. This is consistent the other signals already mentioned.

So why are markets not demanding greater risk premia – that is higher returns – in what appears to be a much riskier environment?

Under market conditions such as those we see in emerging markets today, risk awareness and identification is often not a top asset management priority, even for traditionally conservative investors. Northern Asset Management Trust published a study last week that found 82% of global institutional investors surveyed were only fairly to moderately certain (some were even completely uncertain) of the risk exposures across their portfolios.

Another piece of the puzzle is that risk premia do not accurately capture the cost of uncertainty. Risk is priced using models based on normal parameters – mean and standard deviation – a practice which itself contributes to the underpricing of risk, as we saw most recently in the Great Recession. The methods used to price uncertainty are even less reliable and are inexact estimates at best.

To some degree, we can observe risk-free rates. But when it comes to risky rates and the constituent premia that make up the spreads between them and their risk-free counterparts, your guess is as good as mine, essentially. Add to this that risk-free rates are already up against their zero lower bounds due to the policies of major central banks, and risk premia calculations are likely to be a bit light.

There is also a natural bias towards underestimating risk and its costs. In addition, there is little incentive to accurately estimate risk premia and plenty of incentive to keep estimates low, especially at the top end of a frothy market. Given the discounted cash flow models at the heart of all asset valuation methods, the lower the discount rate we use the better the valuations (or the higher the multiples) that result.

Regardless, if you happen to believe that risk-free rates are destined to rise, market risk premia are likely to respond similarly. The resulting increase in discount rates will have a predictable and deleterious impact on asset valuations, including those in the emerging markets.

Robert J. Shiller of Yale University has an interesting take on this phenomenon and thinks equities in general are “not a bad investment, all things considered.” He sees good old-fashioned fear and greed at work, with a twist.

Speaking recently on CNBC, Shiller said, “You might think the stock market should go down when people are anxious. But people are anxious now because of the international situation … and they’re anxious now because inequality is getting worse. People are worried about being replaced by a computer. All these things are on people’s mind and it creates kind of a desire to save more. The economy has been relatively weak, (so people) bid up the prices of everything.”

To be sure, emerging markets have their forceful advocates. Dr. Ed Yardeni blogs emerging markets are outperforming because “economic reforms could spur more domestic growth” in their economies. Templeton’s Mark Mobius told Institutional Investor in August that emerging markets are doing well because “there is just too much money waiting to be invested.” Institutional Investor gushes, “The numbers back him up.”

That is the magazine serving the same group of eponymous asset managers who are not too sure of their risk exposures, by the way.