The United States’ monetary policy has far-reaching, sometimes unintended consequences, and these past few years have seen unprecedented liquidity injections from the Fed. One way the stimulus manifests itself is as bubbles in other economies, where the ultra-low rate set by the Fed is like pouring gasoline on an already raging fire.

Singapore’s benchmark interest rate, the SIBOR, is tied to the U.S. Fed Funds Rate to minimise large swings in the USD-Singapore dollar exchange rate. Low interest rates are a direct cause of credit bubbles, and Singapore is no exception.

Since the SIBOR is used to price most of the loans and mortgages in Singapore, a very low SIBOR means cheap credit for Singaporeans. The ratio of household debt to gross domestic product now stands at around 75%, up from 55% in 2010 and 45% in 2005, according to data compiled by Standard Chartered.

Furthermore, 70% of those loans have floating interest rates, meaning that once the Fed tapers, mortgage repayments will increase too, possibly exposing unsustainable debt in the system.

Chart 1. Loans to private sector, Singapore (Source: Trading Economics)

Arguably, there is a region-wide emerging markets bubble, encompassing not just Singapore, but also Malaysia, Thailand, the Philippines and Indonesia. Singapore just happens to be the financial hub of the region and thus benefits from the skyrocketing price indices and booming household debt, as long as it lasts.

It has not required a lot of persuasion to allure investors to emerging markets, in a time when Western sovereigns and companies have nursed their post-2008 headache.

This emerging markets bubble is likely to burst, once the Chinese bubble and thus commodity prices pop. Given the makeup of Singapore’s economy, mainly characterized by finance and real estate, the chain of events could unfold in a way that echoes the financial crisis in Iceland and Ireland. However, as is usual with bubbles, they tend to be flat-out denied until they burst for little or no apparent reason.

Chart 2. Property Price Index, Singapore (Source: Trading Economics)

The credit bubble is linked to the soaring property price index because Singaporeans invest in housing or buy a property beyond their means, just as their American counterparts did in the run-up to the credit crunch.

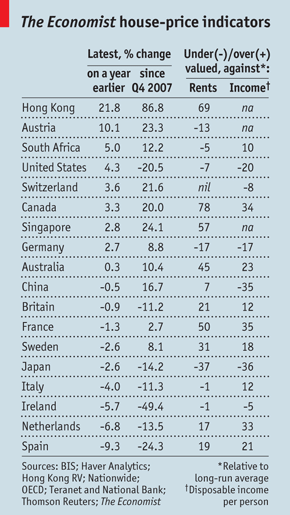

The Economist labels Singapore as the third most expensive residential property market in the world, on a price-to-rent basis, causing a 57% overvaluation relative to the long-term average. Only Canada and Hong Kong are pricier. If the property market goes, so does the banking sector, since the banks hold almost 50% of their credit portfolios in property-related loans, residential mortgages making up nearly a third.

Although the Monetary Authority of Singapore claims the property market is stabilizing, it looks more like the ‘permanent, high plateau’-theory touted for housing at the height of past real estate bubbles in the US.

The evolution of Singapore’s bubble is closely tied to US monetary policy, and though the causality is far from clear, Singaporean home price indices did reflect the first decline in seven quarters in 2013 Q4, as the Fed started tapering. Since the process of returning to non-zero interest rates in the US is likely to be extremely slow, the bursting of Singapore’s bubble is hardly imminent.

However, as Yellen and co. inch the rate upwards, the situation in Singapore will deteriorate. If recent history is any guide, the 1997 Asian Financial Crisis should suggest that contagion is a significant risk in the region. If Singapore (or Malaysia, Indonesia, the Philippines, Thailand) goes, so may the rest.

{kind=link}