While not without risks, the recent opening of Burma to the outside world creates a plethora of new opportunities for investors.

Since Burma (also known as Myanmar) began to re-engage with the outside world in 2010, the country has made great strides in liberalizing politically and economically. The military junta has stepped back from running the country, former leading general Thein Sein has accepted defeat after contentious 2015 elections, and the government is now in the hands of National League for Democracy (NDL).

Since officially gaining power in 2016, the NDL has worked to empower its Nobel-Laureate leader, Aung San Suu Kyi, by creating the post of State Counsellor for her, as she is barred by the Constitution from holding the Presidency. Ms. Kyi has shown every intention of further reforming Burma, starting with the recent freeing of its few remaining political prisoners.

Due to Burma’s ongoing economic liberalization, natural resources, and geographic positioning, it has the potential to experience prolonged and rapid growth. While not without risks, Burma offers international investors many new opportunities in 2016.

Economic liberalization

Until recently, Burma was all but cut off from the outside world. The military government kept the country isolated in order to cement its reign at any cost, famously refusing outside assistance after Cyclone Nargis in 2008 — an act which the United Nations warned would create a “second catastrophe” as the survivors starved or succumbed to disease.

Much has changed since then. After Thein Sein assumed control of the country in 2010, that isolation steadily began to dissipate. As the government encouraged freedom of expression and released political prisoners, the West began dismantling the sanctions regime that had prevented outside investment in the country.

The government also actively courted foreign investors through a series of reforms which eased domestic ownership requirements and provided preferential taxes and export tariffs. Foreign investors quickly responded to these reforms and poured an estimated $8.1 billion into the country in 2014 — roughly 25 times the amount of foreign investment the country received before the military ceded power.

Engines of growth in Burma

Burma has several features that, with democratic transition now appearing to be stably underway, make it attractive for outside investors. Because the country is relatively unindustrialized, it offers high returns to investment for industries that intensively use unskilled labor, such as textiles. Burma’s potential as a manufacturing hub can readily be seen in industrializing countries such as neighboring Bangladesh, which has experienced explosive textile growth since the 1980s.

Even more attractive are Burma’s potential oil and natural gas deposits. While the exact amount of Burmese reserves is unknown, estimates place it on par with Brazil’s reserves. This obviously represents a massive potential windfall, and it is consequently unsurprising that oil and gas represented about a third of Foreign Direct Investment in Burma in 2015. Recent developments are also promising — earlier this year, the Australian oil company Woodside announced that it had discovered gas fields during exploratory offshore drilling.

Burma also benefits from an advantageous geographic location that allows it easier to access world markets. While much of the infrastructure needed to support industries is underdeveloped in the interior of the country, the country’s ports provide it with ready access to the Indian Ocean and global shipping.

These coastal regions could easily be encouraged to develop into centers of economic growth which could in turn provide the necessary revenue for the government to fund infrastructure improvements across the country.

Enduring risks?

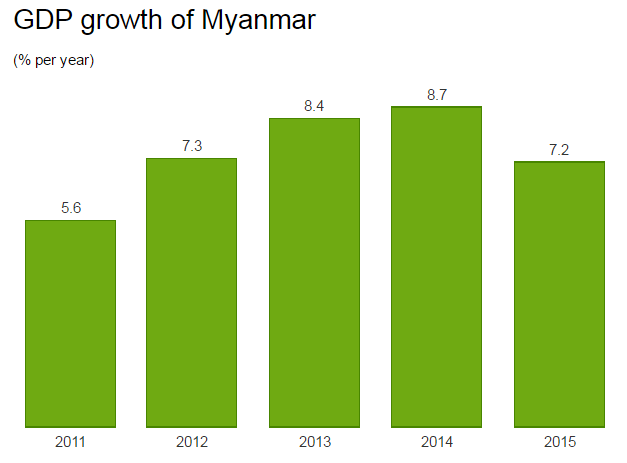

In light of Burma’s strengths, it is hardly surprising that it has grown at an average of around 8% per year since 2012, and is projected to grow by a further 8.6% in 2016 according to the Asian Development Bank. However, it would be misleading to say that the country is risk-free.

The military remains an important player socially and in domestic politics, where it retains control of a constitutionally-mandated 25% of the legislature. Given its position, the possibility of another coup and a return to direct military rule is an ever-present possibility. This chance is only exacerbated by the NDL’s antipathy towards the military and its talk of discarding the 2008 constitution for one that would better constrain the armed forces.

At the same time, while Burma has made tremendous strides in promoting human rights over the past several years, significant problems remain. Ethnic tensions exist between the government and minority groups, many of which have led to guerrilla insurgencies against the state. While the plight of the Rohingya Muslims — who are officially viewed as foreigners and denied citizenship — may be well known in the West, most of Burma’s peripheral minority groups are poorly integrated and discriminated against.

Along with the country’s endemic use of child labor, this discrimination creates risk for investors by increasing the possibility of renewed punitive sanctions by the West and general instability. While the West has demonstrated a willingness to overlook oppression of minorities in countries that are already integrated into the international system, Burma’s lack of strong systemic ties make it easier for domestic interest groups to pressure Western governments to act against it.

Burma thus faces enduring risks, but has immense potential. While the country may need to deepen its reforms in order to reassure foreign investors of its long-term viability, it has made tremendous strides since the end of military rule in 2010 and there is good reason to believe this progress will continue.