US shale oil transformed global energy markets over the past decade. But as the first wave of excitement over energy windfalls has passed, the grim reality has kicked in with the price slump.

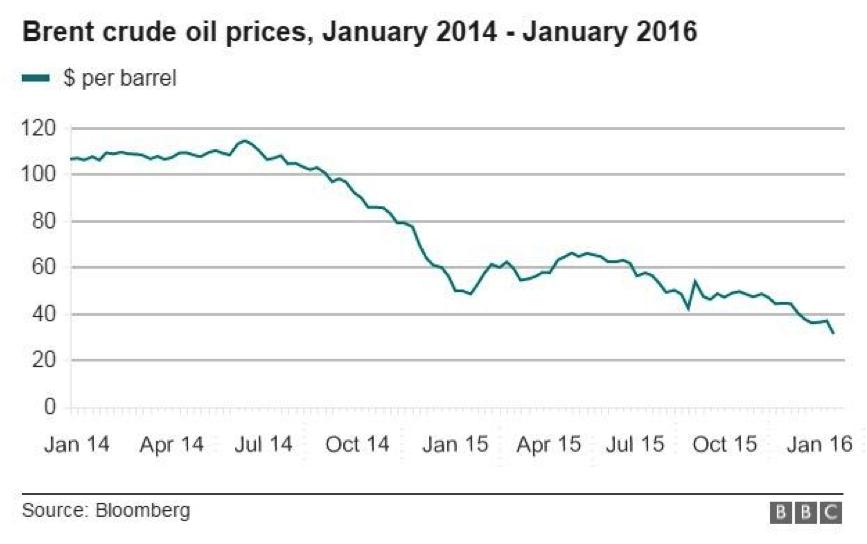

The US oil industry is experiencing its worst period since the 1980s, and the end is nowhere in sight. Since June 2014, oil prices have collapsed from more than $100 to $30 per barrel, and the most recent forecasts predict a further slide to $20 per barrel.

In 2007, oil production was hovering around 5 million barrels per day (mb/d), but by 2010, it increased by 500 000 b/d, and by early 2015 it shot up to 9.5 mb/d. Almost all of this increase came from unconventional shale fields.

Source: Federation of American Scientists

Such tremendous success had implications for both the US and global markets. By 2012 it was already clear that the US energy infrastructure was not ready to absorb large quantities of crude oil, which in effect created an oil glut and depressed US domestic prices bellow the global Brent benchmark.

US refineries quickly took advantage, and started to refine larger quantities of domestic sweet crude, instead of importing from traditional markets such as Nigeria, Algeria, Angola, Brazil and Russia.

In June 2014, the glut spillover effect finally started to affect global markets and prices began to fall. OPRC’s refusal to act as a swing producer and cut production in order to support prices in October 2014 further aggravated the situation. The world found itself awash with 2 million barrels of excess oil.

Over the past year and a half, the US oil sector has struggled to survive. Although producers managed to significantly cut capital costs, the breakeven point for the majority of shale producers is still considerably higher than the current price of oil.

In addition to low oil prices, the Federal Reserve’s decision to raise interest rates will reduce the ability of oil companies to find fresh capital in the financial markets. For many producers this means bankruptcy. According to the most recent analysis, as much as half of all shale producers could go bust if oil prices do not recover soon.

In terms of output, production is falling as well, but not as quickly as Saudi Arabia and other OPEC producers would like it to. According to the US Energy Information Agency (EIA), US production is expected to fall from 9.2 mb/d in November 2015, to 8.5 mb/d by September 2016.

The long-awaited decision to lift the ban on exports of crude oil in December 2015 was a welcome move, but in the current low price environment, it will not help much. There is so much discounted oil in global markets that American shale will still struggle to find new markets in the short-term.

However, there remains some optimism in the medium to long-term. The oil glut is expected to ease by late 2016 and in 2017. In such a scenario, the realistic forecast for oil prices is between $60-80 by 2020. Although this will not completely reverse the impact of the price slump, it will help the US oil industry to restructure and survive. Analysts should still be weary of sluggish global demand and Chinese economic troubles which may easily postpone this recovery.

However, despite current woes, shale will continue to be the game changer in the long term. Its greatest strength, in comparison to other global players, lies in the stable American political and economic environment, and the ability to quickly adapt to market realities. This will not only benefit the US economy, but also contribute to the overall stability of global energy markets.