Eurobonds have become popular financial solutions to Africa’s economic woes. However, their increased popularity may in fact result in increased risks for both lenders and borrowers.

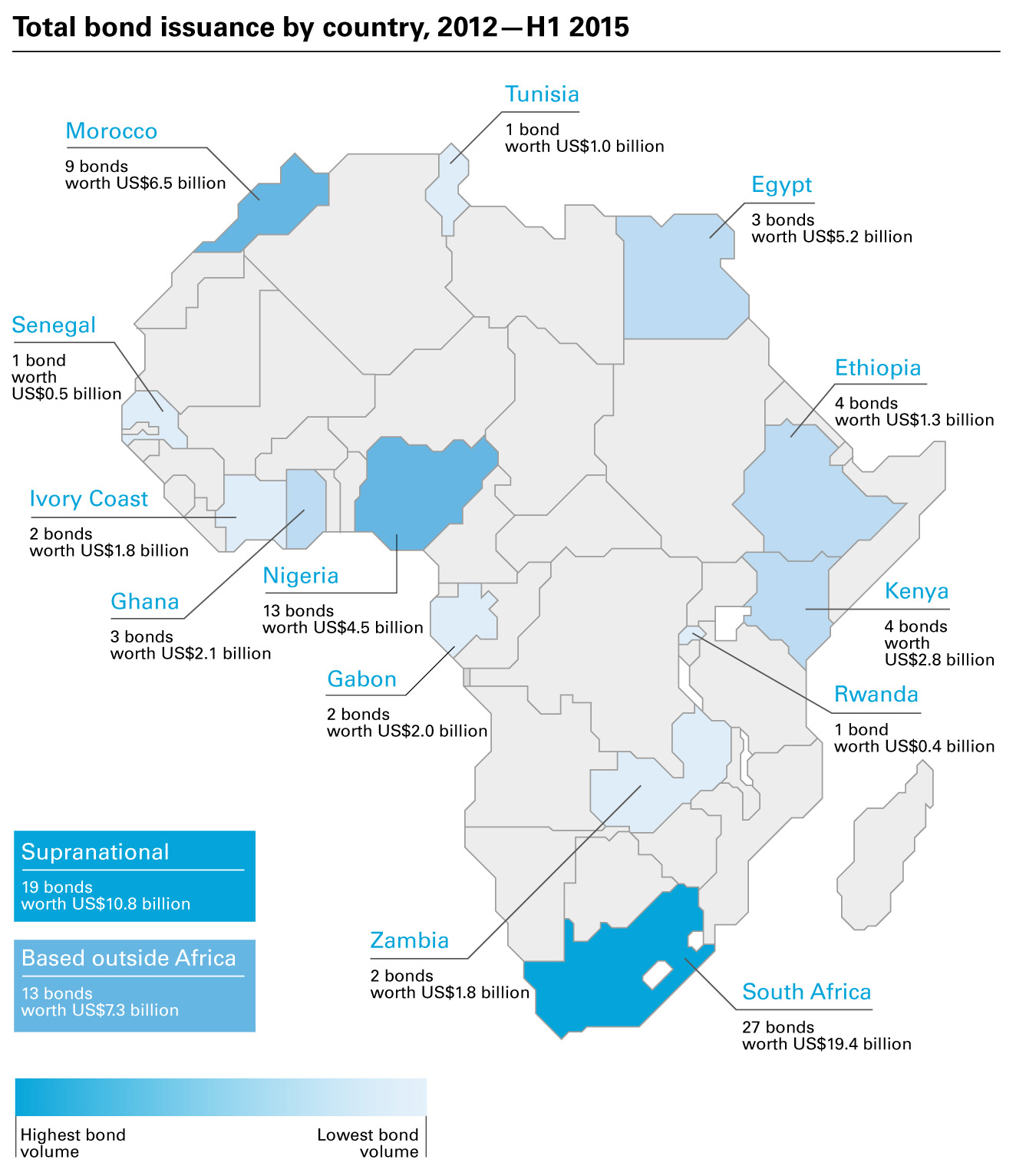

Eurobonds remain increasingly popular in Africa. Early November alone saw six sovereign issues from Angola, Gabon, Ghana, Ivory Coast, Namibia and Zambia, worth around $6 billion.

For investors, high yields have generated strong interest. By example, Angola’s recent ten year $1.5 billion debut Eurobond, with a yield of 9.5% was heavily oversubscribed. For African governments, Eurobonds are attractive in the face of commodity price drops and a need to finance continued economic growth.

One of the primary issues associated with Eurobonds is currency risk. An ODI report earlier in the year argued that if currency depreciation (relative to the dollar) were to reach 30%, this could result in losses of $10 billion for Africa. The likelihood of this scenario is increased in light of the anticipated Fed rates hike (expected on Wednesday 16th December).

In an effort to navigate this problem both Nigeria and Angola (oil dependent economies) have sought to tighten currency controls but volatile commodity markets continue to accentuate the problem. Currencies particularly at risk include: Zambian kwacha, Angolan kwanza, Namibian dollar, Ugandan shilling and Tanzanian shilling.

Patronage Machine

However, one of the primary risks is not economic, but political. One of the reasons that Eurobonds have become a favoured financing mechanism is their unregulated nature. African governments can use funds unaccountably while investors are shielded from liability. This could in part explain why African governments are looking to debt markets rather than the IMF for loans.

Where before, revenues from oil and gas and other commodities had financed extensive patronage networks, Eurobonds could now be replacing these patronage machines as political leaders’ primary means by which to enhance their political control and fortunes.

Governments such as Angola’s or Kenya’s, which face increased political divisions, in part, as a result of economic problems from oil price drops and China’s waning economic growth, could be prone to look to Eurobonds as a means to maintain patronage networks which consolidate their power.

Source: whitecase.com

Alternatively, for countries facing competitive elections in 2016, Eurobonds could be used for election spending and short-term improvements in the economy to improve chances of obtaining office. Eurobond issuances are expected to continue in 2016, which is also a big year for elections in Zambia, Ghana, DRC, Gabon, Uganda, Equatorial Guinea and many other African countries.

Given the long period (sometimes around 25 years) before Eurobonds reach redemption, investors tend not to factor political risks into their equation, or certainly do not worry about it until payment is nearly due. It is likely that servicing debts for African governments will already be a challenge given local currency volatility and Fed rates hikes, but the risk of default is heightened far more by the potential misuse of Eurobonds.

If Eurobonds are used as a strategic source of finance to diversify economies and fund infrastructure projects which will help catalyse economic growth then risks are not high. But in many instances in Africa, political interests can trump economic ones and patronage is a continuing feature in a number of countries. It is hard to assess political risk, as evidence of corrupt patronage networks can be hard to substantiate, but this does not discount the reality of its presence or at least its potential, given the unregulated nature of Eurobond funds.

Eurobondage

In the long-term, the real losers could end up being African countries. Increasing debt rates are not in and of themselves problematic, but in the context of macroeconomic instability and political uncertainty, debt can be a huge problem.

Last year, the IMF warned African countries of these risks, a warning that has become of an increasingly serious nature in light of continued commodity price drops which are taking a toll on many countries GDPs. On 8th December, oil prices slid below $37 per barrel, the lowest since 2009.

If African countries borrow more than they can pay back, then they could face problems similar to those of Portugal, Italy, Greece and Ireland. There is a risk that Africa may stop “rising,” but debt levels will not.

Risk Outlook

Eurobonds issuances are likely to continue, but African governments risk falling into Eurobondage, financing debt with debt, extending redemption periods and dropping credit ratings, and may even default if the political interests of elites take precedent over economic problems. This happened all too recently in 2010/11 when the Ivory Coast defaulted.

For investors, political risks remain at an arm’s length and seemingly distant. But reputation risks could accompany them if widespread Eurobonds are used for corruption and impropriety. For example, in Kenya there are allegations that $1.4 billion of a Eurobond fund cannot be accounted for. This type of potential financial mismanagement is not a sustainable trend and could end up being costly to both lenders and borrowers in the long-term.

{kind=link}